Exam 15: Investments and International Operations

Bond sinking funds are examples of short-term investments.

False

Comprehensive income refers to all changes in equity during a period except those from owners' investments and dividends.

True

Identify the classifications for investments in securities. Briefly comment on the differences among the features of equities that are classified as held-for-trading, available-for-sale, those with significant influence, and those with control.

Accounting for investments in securities depends on some or all of the following:

1. purpose, e.g. trading or long-term investment, the company's intent to hold the security either short-term or long-term,

2. its contractual characteristics, e.g. debt or equity,

3. whether it is listed on an exchange,

4. the industry in which the reporting entity operates, and

5. the accounting policy choice of the reporting entity.

Held-for-trading securities are acquired principally for the purpose of selling or repurchasing them in the near term, with a pattern of short-term profit-taking.

Available-for-sale securities are purchased to yield dividends or increases in fair value. They are not actively managed like held-for-trading securities.

A long-term investment classified as equity with significant influence implies that the investor can exert significant influence over the investee. An investor that owns 20% or more (but not more than 50%) of a company's voting shares is usually presumed to have a significant influence over the investee.

A long-term investment classified as equity with control implies that the investor can exert a controlling influence over the investee. An investor who owns more than 50% of a company's voting shares has control over the investee.

Explain how investors report investments in equity securities when the investor has control over an investee.

When an investor company owns more than 25% of the voting shares of an investee company, it has a controlling influence.

Define the return on total assets and explain how it is used to measure a company's financial performance.

An investor purchased bonds and holds them to maturity. The investor's journal entry to record the interest accrued at the end of the period should include a debit to Interest Receivable and a credit to Interest Revenue.

The consolidation method is used in accounting for long-term investments in equity securities with controlling influence.

Accounting for investments in securities depends on, among ther things, the contractual characteristics, e.g. debt or equity.

Explain the difference between short-term and long-term investments. Cite examples of each.

Any cash dividends received from equity securities are recorded as Dividend Expense.

Cash equivalents are investments that are readily converted to known amounts of cash and mature within three months.

___________________________ are investments in securities that management intends to convert to cash within the longer of one year or the operating cycle, and are readily convertible to cash.

Investments in held-for-trading securities are always classified as ______________ and are reported as _______________ on the balance sheet.

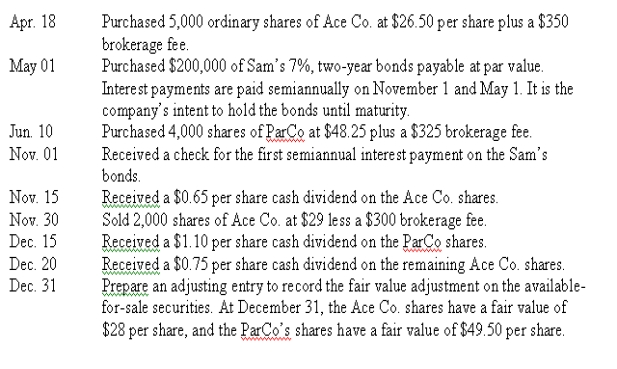

Acadia had no investments prior to the current year. It had the following transactions involving available-for-sale and held-to-maturity securities during the year. The share purchases are considered short-term available-for-sale securities. Prepare journal entries to record the transactions and events associated with the investment purchases.

Equity securities giving an investor significant influence over an investee are always considered short-term investments.

Any unrealized gain or loss for the portfolio of available-for-sale securities is reported as profit or loss on the income statement.

When using the equity method for investments in equity securities, the investor records the receipt of cash dividends as revenue.

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)