Exam 21: Non-Current Assets: Revaluation, Disposal and Other Aspects

Exam 1: Decision Making and the Role of Accounting44 Questions

Exam 2: Financial Statements for Decision Making67 Questions

Exam 3: Recording Transactions64 Questions

Exam 4: Adjusting the Accounts and Preparing Financial Statements65 Questions

Exam 5: Completing the Accounting Cycle Closing and Reversing Entries65 Questions

Exam 6: Accounting for Retailing65 Questions

Exam 7: Accounting for Systems63 Questions

Exam 8: Accounting for Manufacturing65 Questions

Exam 9: Cost Accounting Systems66 Questions

Exam 10: Cash Management and Control65 Questions

Exam 11: Cost-Volume-Profit Analysis for Decision Making65 Questions

Exam 12: Budgeting for Planning and Control65 Questions

Exam 13: Performance Evaluation for Managers65 Questions

Exam 14: Differential Analysis, Profitability Analysis and Capital Budgeting65 Questions

Exam 15: Partnerships: Formation, Operation and Reporting65 Questions

Exam 16: Companies: Formation and Operations65 Questions

Exam 17: Regulation and the Conceptual Framework64 Questions

Exam 18: Receivables65 Questions

Exam 19: Inventories60 Questions

Exam 20: Non-Current Assets: Acquisition and Depreciation65 Questions

Exam 21: Non-Current Assets: Revaluation, Disposal and Other Aspects65 Questions

Exam 22: Liabilities63 Questions

Exam 23: Presentation of Financial Statements65 Questions

Exam 24: Statement of Cash Flows65 Questions

Exam 25: Analysis and Interpretation of Financial Statements64 Questions

Select questions type

Billy's Computer Shop purchased some new equipment trading in old equipment with a carrying amount of $10 000. Cash of $9000 was paid to the supplier and a trade-in allowance of $7000 was granted. The new equipment should be recorded at:

(Multiple Choice)

4.8/5  (38)

(38)

Which of these does not contribute to the value of purchased goodwill?

(Multiple Choice)

4.9/5 (29)

According to IAS 38/AASB 138 intangible assets that have been established to have finite useful lives:

(Multiple Choice)

4.8/5 (38)

How many of these statements are true of the composite rate depreciation approach?

The general asset mix of a functional group of assets is assumed to be the same through new assets are added and old assets are sold.

Additions and retirements are assumed to occur uniformly throughout the year.

The method is often used by business entities with many similar assets in one class.

Profits and losses on disposal of assets are debited/credited to the accumulated depreciation account so no losses or profits on disposal are recorded.

(Multiple Choice)

4.9/5 (35)

Which statement relating to the composite-rate depreciation approach is not true?

(Multiple Choice)

4.7/5 (29)

FK Ltd's fleet of delivery trucks (original cost $850 000) had a carrying amount on 1 July 2012 of $470 000. On that date their value was revised to $500 000. Future depreciation charges will be based on which amount?

(Multiple Choice)

4.8/5 (34)

On 31 December 2014 an aeroplane with a cost of $200 000 has had accumulated depreciation written off of $170 000. If it was sold for a profit of $30 000 on 1 January 2015 how much was recorded as income from the proceeds of the sale?

(Multiple Choice)

4.7/5 (41)

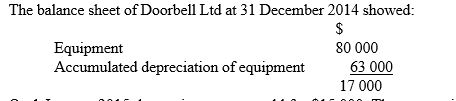

On 1 January 2015 the equipment was sold for $15 000. The accounting entry to record the closing of the equipment and the accumulated depreciation of equipment accounts is which of the following?

On 1 January 2015 the equipment was sold for $15 000. The accounting entry to record the closing of the equipment and the accumulated depreciation of equipment accounts is which of the following?

(Multiple Choice)

4.8/5 (36)

When a non-current asset is sold the gain or loss on disposal is the difference between:

(Multiple Choice)

4.8/5 (35)

Under IAS 38/AASB 138, which statement concerning internally generated intangible assets is not true?

(Multiple Choice)

4.7/5 (38)

Under the accounting standard dealing with revaluations, IAS 16/AASB 116, an entity is required to:

(Multiple Choice)

4.9/5 (37)

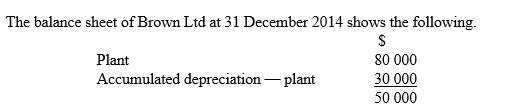

On 1 January 2015, based on a valuer's estimate of fair value, it was decided to revalue the plant to $65 000. The plant was then assessed to have a further useful life of 5 years and an expected residual amount of $5000. What is the journal entry in the books of Brown Ltd to record depreciation on plant on a straight-line basis for the half-year ending 30 June 2015 (balance date)?

On 1 January 2015, based on a valuer's estimate of fair value, it was decided to revalue the plant to $65 000. The plant was then assessed to have a further useful life of 5 years and an expected residual amount of $5000. What is the journal entry in the books of Brown Ltd to record depreciation on plant on a straight-line basis for the half-year ending 30 June 2015 (balance date)?

(Multiple Choice)

4.8/5 (34)

On 31 December 2013 a printing machine with a cost of $380 000 has accumulated depreciation written off of $140 000. If it is sold for $220 000 on 1 January 2014 what will be the net effect of the sale on the income statement?

(Multiple Choice)

4.8/5 (35)

Under IAS 41/AASB 141 the basis for measuring biological assets is:

(Multiple Choice)

4.8/5 (39)

How many of these are requirements of IAS 16/AASB 116?

An entire class of non-current assets must be revalued together.

If the revaluation model is adopted non-current assets should be revalued to either fair value or the value in use.

Before a depreciable asset is revalued accumulated depreciation should be written back to the asset account.

(Multiple Choice)

4.9/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)