Exam 21: Non-Current Assets: Revaluation, Disposal and Other Aspects

Exam 1: Decision Making and the Role of Accounting44 Questions

Exam 2: Financial Statements for Decision Making67 Questions

Exam 3: Recording Transactions64 Questions

Exam 4: Adjusting the Accounts and Preparing Financial Statements65 Questions

Exam 5: Completing the Accounting Cycle Closing and Reversing Entries65 Questions

Exam 6: Accounting for Retailing65 Questions

Exam 7: Accounting for Systems63 Questions

Exam 8: Accounting for Manufacturing65 Questions

Exam 9: Cost Accounting Systems66 Questions

Exam 10: Cash Management and Control65 Questions

Exam 11: Cost-Volume-Profit Analysis for Decision Making65 Questions

Exam 12: Budgeting for Planning and Control65 Questions

Exam 13: Performance Evaluation for Managers65 Questions

Exam 14: Differential Analysis, Profitability Analysis and Capital Budgeting65 Questions

Exam 15: Partnerships: Formation, Operation and Reporting65 Questions

Exam 16: Companies: Formation and Operations65 Questions

Exam 17: Regulation and the Conceptual Framework64 Questions

Exam 18: Receivables65 Questions

Exam 19: Inventories60 Questions

Exam 20: Non-Current Assets: Acquisition and Depreciation65 Questions

Exam 21: Non-Current Assets: Revaluation, Disposal and Other Aspects65 Questions

Exam 22: Liabilities63 Questions

Exam 23: Presentation of Financial Statements65 Questions

Exam 24: Statement of Cash Flows65 Questions

Exam 25: Analysis and Interpretation of Financial Statements64 Questions

Select questions type

Which statement concerning revaluations that reverse prior adjustments in value is untrue?

(Multiple Choice)

4.9/5  (46)

(46)

King Ltd acquired the business of Prince Ltd for a cash payment of $480 000. The carrying amount of Prince Ltd's assets at the time of purchase was $490 000 while the independent fair value was $460 000. There were no liabilities. What is the value of the purchased goodwill recorded by King Ltd?

(Multiple Choice)

4.9/5 (36)

On 31 December 2014 an aeroplane with a cost of $200 000 has accumulated depreciation written off of $90 000. If it was sold for $130 000 on 1 January 2015 how much will be recorded as the expense carrying-value on the disposal of the plane?

(Multiple Choice)

4.8/5 (42)

A motor vehicle, which had a carrying amount at the end of the financial year 2011/12 of $18 000, was disposed of on 1 November 2012. Depreciation was calculated on the vehicle at 20% per annum using the diminishing-balance method. What was the depreciation expense charged for the first 4 months of the financial year 2012/13, before the asset was sold?

(Multiple Choice)

4.9/5 (43)

The pair of terms that match is:

i. Non-current fixed assets and depreciation

ii. Natural resources and amortisation

iii. Intangible assets and depletion

iv. Land and depreciation

(Multiple Choice)

4.7/5 (35)

The carrying amount of a depreciable, non-current asset is its:

(Multiple Choice)

4.9/5 (41)

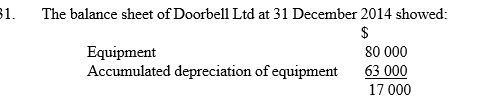

On 1 January 2015 the equipment was sold for $15 000. What is the accounting entry to record the receipt of the proceeds from the sale of the equipment?

On 1 January 2015 the equipment was sold for $15 000. What is the accounting entry to record the receipt of the proceeds from the sale of the equipment?

(Multiple Choice)

4.7/5 (31)

IFRS 3/AASB 3 requires that if the amount paid for a business is less than the sum of the fair value of the net identifiable assets acquired, and this is a genuine bargain purchase, then the difference is to be:

(Multiple Choice)

4.8/5 (30)

Accounting standard IAS 16/AASB 116 requires what basis of valuation to be used if assets are valued at other than cost?

(Multiple Choice)

4.9/5 (34)

Which of these terms have the same meaning in accounting?

i. Carrying amount

ii. Book value

iii. Written down value

(Multiple Choice)

4.9/5 (32)

What is the accounting entry to amortise an intangible asset over its useful life?

(Multiple Choice)

4.8/5 (36)

In accounting standard IAS 16/AASB 116 a downward revaluation is now known as a:

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)