Exam 4: Elasticity and Its Applications

Exam 1: What Is Economics59 Questions

Exam 2: Thinking Like an Economist54 Questions

Exam 3: The Market Forces of Supply and Demand56 Questions

Exam 4: Elasticity and Its Applications58 Questions

Exam 5: Background to Demand: Consumer Choices61 Questions

Exam 6: Background to Supply: Firms in Competitive Markets54 Questions

Exam 7: Consumers, Producers and the Efficiency of Markets56 Questions

Exam 8: Supply, Demand and Government Policies51 Questions

Exam 9: The Tax System48 Questions

Exam 10: Public Goods, Common Resources and Merit Goods58 Questions

Exam 11: Market Failure and Externalities61 Questions

Exam 12: Information and Behavioural Economics60 Questions

Exam 13: Firms Production Decisions47 Questions

Exam 14: Market Structures I: Monopoly57 Questions

Exam 15: Market Structures Ii: Monopolistic Competition59 Questions

Exam 16: Market Structures Iii: Oligopoly55 Questions

Exam 17: The Economics of Factor Markets60 Questions

Exam 18: Income Inequality and Poverty60 Questions

Exam 19: Interdependence and the Gains From Trade56 Questions

Exam 20: Measuring a Nations Well-Being60 Questions

Exam 21: Measuring the Cost of Living59 Questions

Exam 22: Production and Growth60 Questions

Exam 23: Unemployment60 Questions

Exam 24: Saving, Investment and the Financial System60 Questions

Exam 25: The Basic Tools of Finance57 Questions

Exam 26: Issues in Financial Markets59 Questions

Exam 27: The Monetary System60 Questions

Exam 28: Money Growth and Inflation59 Questions

Exam 29: Open-Economy Macroeconomics: Basic Concepts60 Questions

Exam 30: A Macroeconomic Theory of the Open Economy61 Questions

Exam 31: Business Cycles55 Questions

Exam 32: Keynesian Economics and the Is-Lm Analysis60 Questions

Exam 33: Aggregate Demand and Aggregate Supply60 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand41 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment52 Questions

Exam 36: Supply-Side Policies57 Questions

Exam 37: Common Currency Areas and European Monetary Union55 Questions

Exam 38: The Financial Crisis and Sovereign Debt60 Questions

Select questions type

If consumers always spend 15 percent of their income on food, then the income elasticity of demand for food is

(Multiple Choice)

4.8/5  (37)

(37)

If the price elasticity of supply equals zero, this implies that

(Multiple Choice)

4.7/5 (28)

Suppose that the price elasticity of supply of lawn mowers is 1.5. If the price of lawn mowers rises 5 per cent, the quantity supplied of lawn mowers would

(Multiple Choice)

4.9/5 (25)

If there is excess capacity in a production facility, it is likely that the firm's supply curve is

(Multiple Choice)

4.9/5 (29)

If Euro T-Shirt Co. lowers its price from €6 to €5 and finds that students increase their quantity demanded from 400 to 600 T-shirts per month, then the demand for EuroT-shirts within this price range is

(Multiple Choice)

4.7/5 (30)

In general, demand curves for luxuries tend to be price elastic.

(True/False)

4.9/5 (37)

If consumers think that there are very few substitutes for a good, then

(Multiple Choice)

4.8/5 (35)

The midpoint method is used to compute elasticity because it

(Multiple Choice)

4.9/5 (42)

The price elasticity of supply tends to be more inelastic as the firm's production facility reaches maximum capacity.

(True/False)

4.9/5 (32)

The price elasticity of demand is defined as the percentage change in quantity demanded divided by the percentage change in price.

(True/False)

4.8/5 (32)

Suppose that when the price rises by 10% for a particular good, the quantity demanded of that good falls by 20%. The price elasticity of demand for this good is equal to 2.0.

(True/False)

4.9/5 (32)

If demand is linear (a straight line), then price elasticity of demand is

(Multiple Choice)

4.9/5 (35)

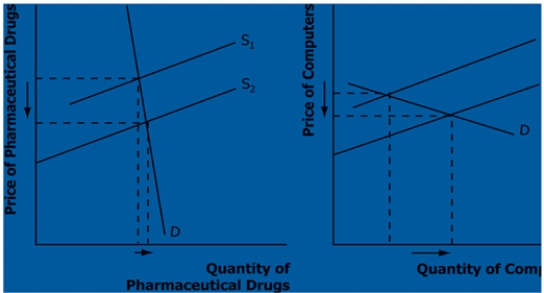

Pharmaceutical drug have an inelastic demand, and computers have an elastic demand. Assume technological advances lead to the doubling of supply of both products.

a. What happens to the equilibrium price and quantity in each market?

b. Which product experiences a larger change in price?

c. Which product experiences a larger change in quantity?

d. What happens to total consumer spending on each product?

(Essay)

4.9/5 (44)

Economists have observed that spending on restaurant meals declines more during economic downturns than does spending on food to be eaten at home. How might the concept of elasticities help explain this?

(Essay)

4.8/5 (28)

A decrease in supply will cause the smallest increase in price when

(Multiple Choice)

4.8/5 (33)

Technological improvements in agriculture that shift the supply of agricultural commodities to the right tend to

(Multiple Choice)

4.8/5 (34)

Suppose that at a price of €30 per month, there are 30,000 subscribers to cable television in Small Town. If Small Town Cablevision raises its price to €40 per month, the number of subscribers will fall to 20,000. Using the midpoint method for calculating the elasticity, what is the price elasticity of demand for cable TV in Small Town?

(Multiple Choice)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)