Exam 7: An Introduction to Portfolio Management

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

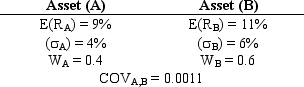

Exhibit 7.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.3. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.3. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.9/5  (44)

(44)

What is the expected return of the three stock portfolio described below?

(Multiple Choice)

4.9/5 (38)

When assessing the risk impact of adding a new security to a portfolio, it is necessary to consider the

(Multiple Choice)

4.8/5 (30)

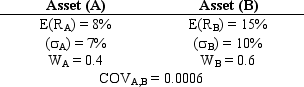

Exhibit 7.2

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.2. What is the standard deviation of this portfolio?

-Refer to Exhibit 7.2. What is the standard deviation of this portfolio?

(Multiple Choice)

4.8/5 (37)

Exhibit 7.3

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.3. What is the standard deviation of this portfolio?

(Multiple Choice)

4.8/5 (40)

What is the expected return of the three stock portfolio described below?

(Multiple Choice)

4.8/5 (48)

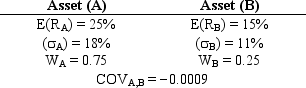

Exhibit 7.5

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.5. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.5. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.7/5 (39)

The correlation coefficient and the covariance are measures of the extent to which two random variables move together.

(True/False)

4.8/5 (44)

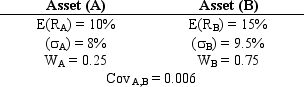

Exhibit 7.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.1. What is the standard deviation of this portfolio?

-Refer to Exhibit 7.1. What is the standard deviation of this portfolio?

(Multiple Choice)

4.8/5 (35)

A portfolio of two securities that are perfectly positively correlated has

(Multiple Choice)

4.9/5 (35)

What is the expected return of the three stock portfolio described below?

(Multiple Choice)

4.8/5 (40)

An investor is risk neutral if she chooses the asset with lower risk given a choice of several assets with equal returns.

(True/False)

4.8/5 (38)

Given a portfolio of stocks, the envelope curve containing the set of best possible combinations is known as the

(Multiple Choice)

4.8/5 (39)

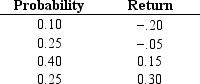

Exhibit 7.13

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

A financial analyst covering Magnum Oil has determined the following four possible returns given four different states of the economy over the next period.

-Refer to Exhibit 7.13. Calculate the expected return for Magnum Oil.

-Refer to Exhibit 7.13. Calculate the expected return for Magnum Oil.

(Multiple Choice)

4.9/5 (30)

The set of portfolios with the maximum rate of return for every given risk level is known as the optimal frontier.

(True/False)

4.7/5 (33)

Exhibit 7B.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 1)2 - r1.2 E( 1) E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2 E( 1) E( 2)]

-Refer to Exhibit 7B.1. What is the value of W1 when r1.2 = -1 and E( 1) = .10 and E( 2) = .12?

(Multiple Choice)

4.9/5 (39)

Exhibit 7.14

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Stocks A and B have a correlation coefficient of -0.8. The stocks' expected returns and standard deviations are in the table below. A portfolio consisting of 40% of stock A and 60% of stock B is constructed.

-Refer to Exhibit 7.14. What percentage of stock A should be invested to obtain the minimum risk portfolio that contains stock A and B?

-Refer to Exhibit 7.14. What percentage of stock A should be invested to obtain the minimum risk portfolio that contains stock A and B?

(Multiple Choice)

4.9/5 (39)

You are given a two asset portfolio with a fixed correlation coefficient. If the weights of the two assets are varied the expected portfolio return would be ____ and the expected portfolio standard deviation would be ____.

(Multiple Choice)

4.9/5 (31)

The most important criteria when adding new investments to a portfolio is the

(Multiple Choice)

4.9/5 (28)

Exhibit 7.13

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

A financial analyst covering Magnum Oil has determined the following four possible returns given four different states of the economy over the next period.

-Refer to Exhibit 7.13. Calculate the standard deviation for Magnum Oil.

(Multiple Choice)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)