Exam 7: An Introduction to Portfolio Management

Exam 1: The Investment Setting78 Questions

Exam 2: The Asset Allocation Decision80 Questions

Exam 3: Selecting Investments in a Global Market80 Questions

Exam 4: Organization and Functioning of Securities Markets91 Questions

Exam 5: Security-Market Indexes84 Questions

Exam 6: Efficient Capital Markets90 Questions

Exam 7: An Introduction to Portfolio Management97 Questions

Exam 8: An Introduction to Asset Pricing Models119 Questions

Exam 9: Multifactor Models of Risk and Return59 Questions

Exam 10: Analysis of Financial Statements89 Questions

Exam 11: Introduction to Security Valuation86 Questions

Exam 12: Macroanalysis and Microvaluation of the Stock Market119 Questions

Exam 13: Industry Analysis90 Questions

Exam 14: Company Analysis and Stock Valuation133 Questions

Exam 15: Technical Analysis83 Questions

Exam 16: Equity Portfolio Management Strategies58 Questions

Exam 17: Bond Fundamentals89 Questions

Exam 18: The Analysis and Valuation of Bonds108 Questions

Exam 19: Bond Portfolio Management Strategies87 Questions

Exam 20: An Introduction to Derivative Markets and Securities108 Questions

Exam 21: Forward and Futures Contracts99 Questions

Exam 22: Option Contracts106 Questions

Exam 23: Swap Contracts, Convertible Securities, and Other Embedded Derivatives87 Questions

Exam 24: Professional Money Management, Alternative Assets, and Industry Ethics102 Questions

Exam 25: Evaluation of Portfolio Performance96 Questions

Select questions type

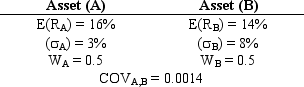

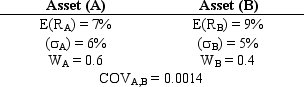

Exhibit 7.10

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.10. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.10. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.8/5  (41)

(41)

The slope of the utility curves for a strongly risk-averse investor, relative to the slope of the utility curves for a less risk-averse investor, will

(Multiple Choice)

4.8/5 (39)

Exhibit 7A.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The general equation for the weight of the first security to achieve the minimum variance (in a two stock portfolio) is given by:

W1 = [E( 2)2 - r1.2 E( 1)E( 2)] /[E( 1)2 + E( 2)2 - 2 r1.2E( 1)E( 2)]

-A good portfolio is a collection of individually good assets.

(True/False)

4.9/5 (36)

As the number of risky assets in a portfolio increases, the total risk of the portfolio decreases.

(True/False)

4.8/5 (33)

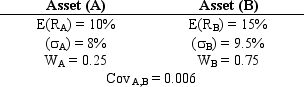

Exhibit 7.1

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.1. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.1. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.8/5 (38)

Between 1980 and 2000, the standard deviation of the returns for the NIKKEI and the DJIA indexes were 0.08 and 0.10, respectively, and the covariance of these index returns was 0.0007. What was the correlation coefficient between the two market indicators?

(Multiple Choice)

5.0/5 (33)

Investors choose a portfolio on the efficient frontier based on their utility functions that reflect their attitudes towards risk.

(True/False)

4.8/5 (41)

A basic assumption of the Markowitz model is that investors base decisions solely on expected return and risk.

(True/False)

4.7/5 (38)

A positive relationship between expected return and expected risk is consistent with

(Multiple Choice)

5.0/5 (26)

The combination of two assets that are completely negatively correlated provides maximum returns.

(True/False)

4.8/5 (40)

Exhibit 7.11

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.11. Calculate the expected standard deviation of the two stock portfolio.

-Refer to Exhibit 7.11. Calculate the expected standard deviation of the two stock portfolio.

(Multiple Choice)

4.7/5 (37)

In a two stock portfolio, if the correlation coefficient between two stocks were to decrease over time, everything else remaining constant, the portfolio's risk would

(Multiple Choice)

4.9/5 (34)

Between 1986 and 1996, the standard deviation of the returns for the NYSE and the DJIA indexes were 0.10 and 0.09, respectively, and the covariance of these index returns was 0.0009. What was the correlation coefficient between the two market indicators?

(Multiple Choice)

4.7/5 (39)

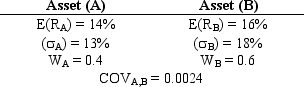

Exhibit 7.15

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.15. What is the standard deviation of this portfolio?

-Refer to Exhibit 7.15. What is the standard deviation of this portfolio?

(Multiple Choice)

4.7/5 (34)

Exhibit 7.15

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.15. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.8/5 (31)

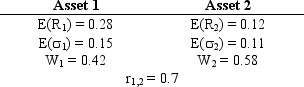

Exhibit 7.12

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Consider two securities, A and B. Security A and B have a correlation coefficient of 0.65. Security A has standard deviation of 12, and security B has standard deviation of 25. Calculate the covariance between these two securities.

-Consider two securities, A and B. Security A and B have a correlation coefficient of 0.65. Security A has standard deviation of 12, and security B has standard deviation of 25. Calculate the covariance between these two securities.

(Multiple Choice)

4.9/5 (41)

A portfolio manager is considering adding another security to his portfolio. The correlations of the 5 alternatives available are listed below. Which security would enable the highest level of risk diversification?

(Multiple Choice)

4.8/5 (44)

Exhibit 7.12

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.12. Calculate the expected returns and expected standard deviations of a two stock portfolio when r1,2 = .80 and w1 = .60.

(Multiple Choice)

4.9/5 (39)

Exhibit 7.7

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

-Refer to Exhibit 7.7. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

-Refer to Exhibit 7.7. What is the expected return of a portfolio of two risky assets if the expected return E(Ri), standard deviation ( i), covariance (COVi,j), and asset weight (Wi) are as shown above?

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)