Exam 1: Introduction to Operations and Supply Chain Management

Exam 1: Introduction to Operations and Supply Chain Management102 Questions

Exam 2: Quality Management88 Questions

Exam 3: Statistical Process Control157 Questions

Exam 4: Product Design95 Questions

Exam 5: Service Design91 Questions

Exam 6: Processes and Technology81 Questions

Exam 7: Capacity and Facilities Design128 Questions

Exam 8: Human Resources131 Questions

Exam 9: Project Management106 Questions

Exam 10: Supply Chain Management Strategy and Design72 Questions

Exam 11: Global Supply Chain Procurement and Distribution122 Questions

Exam 12: Forecasting92 Questions

Exam 13: Inventory Management127 Questions

Exam 14: Sales and Operations Planning123 Questions

Exam 15: Resource Planning97 Questions

Exam 16: Lean Systems88 Questions

Exam 17: Scheduling96 Questions

Select questions type

Canadian companies can become globally competitive by emphasizing the strategic importance of operations.

(True/False)

4.9/5  (27)

(27)

A manager of a global supply chain is concerned with all the following except

(Multiple Choice)

4.8/5 (36)

Single factor productivity compares output to an individual input.

(True/False)

4.7/5 (29)

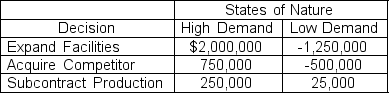

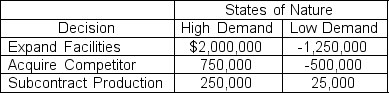

A small parts manufacturer has just engineered a new product for the automotive industry. In order to produce the part the company can expand existing facilities, acquire a competitor, or subcontract production. The company believes the product will either experience high market demand or low market demand. The following payoff table describes the company's decision situation:  The best decision for the manufacturer using the equal likelihood criterion is to

The best decision for the manufacturer using the equal likelihood criterion is to

(Multiple Choice)

4.9/5 (37)

Quantitative methods are tools available to operations managers to help make a decision but not a recommendation.

(True/False)

4.9/5 (44)

A small parts manufacturer has just engineered a new product for the automotive industry. In order to produce the part the company can expand existing facilities, acquire a competitor, or subcontract production. The company believes the product will either experience high market demand or low market demand. The following payoff table describes the company's decision situation:  The best decision for the manufacturer using the maximax decision criterion is to

The best decision for the manufacturer using the maximax decision criterion is to

(Multiple Choice)

4.9/5 (35)

Order qualifiers are the characteristics of a product that have to be satisfied just to be considered for purchase by a customer.

(True/False)

4.9/5 (33)

Quantitative methods are tools available to operations managers to help make a decision or recommendation.

(True/False)

4.8/5 (35)

Human resources management provides demand estimates that are used in production decisions.

(True/False)

4.9/5 (25)

The four primary functional areas of a firm are marketing, finance, operations, and human resources.

(True/False)

4.9/5 (32)

A firm who is adept at recognizing global windows of opportunity, acting on those very quickly, with tight linkages can be said to be competing on

(Multiple Choice)

4.7/5 (30)

Which of the following is not one of the four primary functional areas of a firm?

(Multiple Choice)

4.9/5 (31)

Linear programming, simulation, and waiting line theory are most closely associated with which era in the historical development of operations management?

(Multiple Choice)

4.8/5 (35)

To be effective an operations manager needs an integrated view of business organizations.

(True/False)

4.9/5 (38)

Mass production refers to high-volume production of a standardized product.

(True/False)

4.9/5 (38)

Firms compete in the marketplace based on cost, speed, quality, and flexibility.

(True/False)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)