Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis

Exam 1: What Is Economics232 Questions

Exam 2: The Economy: Myth and Reality155 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice255 Questions

Exam 4: Supply and Demand: an Initial Look313 Questions

Exam 5: Consumer Choice: Individual and Market Demand206 Questions

Exam 6: Demand and Elasticity214 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis221 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis194 Questions

Exam 9: Securities: Business Finance and the Economy: the Tail That Wags the Dog203 Questions

Exam 10: The Firm and the Industry Under Perfect Competition212 Questions

Exam 11: Monopoly208 Questions

Exam 12: Between Competition and Monopoly230 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust155 Questions

Exam 14: The Case for Free Markets: the Price System225 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination172 Questions

Exam 21: Is Useconomic Leadership Threatened75 Questions

Exam 22: An Introduction to Macroeconomics216 Questions

Exam 23: The Goals of Macroeconomic Policy212 Questions

Exam 24: Economic Growth: Theory and Policy228 Questions

Exam 25: Aggregate Demand and the Powerful Consumer219 Questions

Exam 26: Demand-Side Equilibrium: Unemployment or Inflation216 Questions

Exam 27: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 28: Managing Aggregate Demand: Fiscal Policy210 Questions

Exam 29: Money and the Banking System224 Questions

Exam 30: Monetary Policy: Conventional and Unconventional210 Questions

Exam 31: He Financial Crisis and the Great Recession66 Questions

Exam 32: The Debate Over Monetary and Fiscal Policy219 Questions

Exam 33: Budget Deficits in the Short and Long Run215 Questions

Exam 34: The Trade-Off Between Inflation and Unemployment219 Questions

Exam 35: International Trade and Comparative Advantage223 Questions

Exam 36: The International Monetary System: Order or Disorder218 Questions

Exam 37: Exchange Rates and the Macroeconomy219 Questions

Select questions type

Suppose that on a Saturday night at 10pm a large hotel has 300 vacant rooms, with little expectation of renting them at such a late hour on a weekend.A traveler comes in the door, looking a bit down on his luck, and asks how much a room will cost.Since he can't afford the normal rate of $150, the night manager decides to let him stay in the room for only $40.Is it likely that this decision reduced, or increased, the hotel's profits?

Explain your answer.

(Essay)

4.8/5  (40)

(40)

The state is considering adding a satellite campus to its major university.How can marginal analysis assist, even though the university does not attempt to maximize profits?

(Essay)

4.8/5 (36)

Decision making that seeks only solutions that are acceptable is called

(Multiple Choice)

4.7/5 (28)

Profits will be maximized when the slope of the total revenue curve and the slope of the total cost curve equal zero.

(True/False)

5.0/5 (37)

Total revenue is equal to quantity multiplied by average revenue.

(True/False)

4.9/5 (36)

A firm has positive fixed cost and positive variable cost.At its current level of output, marginal cost equals average cost.The firm must

(Multiple Choice)

4.9/5 (34)

Total profit is represented by the vertical distance between a total revenue curve and a total cost curve.

(True/False)

4.9/5 (41)

Some companies follow a strategy of sales maximization.They say that this puts them in close touch with their customers and they can better track the market, responding to needs more quickly.However, this increases costs because of the need to stock a wider variety of parts and sizes and colors, etc.What would make this strategy a profit-maximizing one?

(Essay)

4.9/5 (38)

If marginal cost is less than average cost, average cost must fall when more units are produced.

(True/False)

5.0/5 (38)

It can be shown that average revenue and price are always equal.

(True/False)

4.7/5 (37)

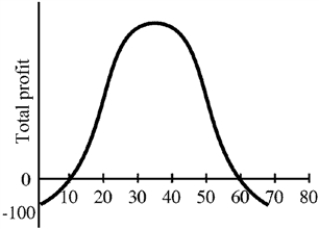

Figure 8-5

-In Figure 8-5, profits are maximized at output of

-In Figure 8-5, profits are maximized at output of

(Multiple Choice)

4.8/5 (36)

A graph of total profits is always likely to be positively sloped throughout its length.

(True/False)

4.8/5 (42)

A small business owner who is earning a positive economic profit, no matter how small, is doing better than if she sold her business and went to work for another firm.

(True/False)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)