Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis

Exam 1: What Is Economics232 Questions

Exam 2: The Economy: Myth and Reality155 Questions

Exam 3: The Fundamental Economic Problem: Scarcity and Choice255 Questions

Exam 4: Supply and Demand: an Initial Look313 Questions

Exam 5: Consumer Choice: Individual and Market Demand206 Questions

Exam 6: Demand and Elasticity214 Questions

Exam 7: Production, Inputs, and Cost: Building Blocks for Supply Analysis221 Questions

Exam 8: Output, Price, and Profit: the Importance of Marginal Analysis194 Questions

Exam 9: Securities: Business Finance and the Economy: the Tail That Wags the Dog203 Questions

Exam 10: The Firm and the Industry Under Perfect Competition212 Questions

Exam 11: Monopoly208 Questions

Exam 12: Between Competition and Monopoly230 Questions

Exam 13: Limiting Market Power: Regulation and Antitrust155 Questions

Exam 14: The Case for Free Markets: the Price System225 Questions

Exam 15: The Shortcomings of Free Markets219 Questions

Exam 16: Externalities, the Environment, and Natural Resources222 Questions

Exam 17: Taxation and Resource Allocation221 Questions

Exam 18: Pricing the Factors of Production233 Questions

Exam 19: Labor and Entrepreneurship: the Human Inputs271 Questions

Exam 20: Poverty, Inequality, and Discrimination172 Questions

Exam 21: Is Useconomic Leadership Threatened75 Questions

Exam 22: An Introduction to Macroeconomics216 Questions

Exam 23: The Goals of Macroeconomic Policy212 Questions

Exam 24: Economic Growth: Theory and Policy228 Questions

Exam 25: Aggregate Demand and the Powerful Consumer219 Questions

Exam 26: Demand-Side Equilibrium: Unemployment or Inflation216 Questions

Exam 27: Bringing in the Supply Side: Unemployment and Inflation228 Questions

Exam 28: Managing Aggregate Demand: Fiscal Policy210 Questions

Exam 29: Money and the Banking System224 Questions

Exam 30: Monetary Policy: Conventional and Unconventional210 Questions

Exam 31: He Financial Crisis and the Great Recession66 Questions

Exam 32: The Debate Over Monetary and Fiscal Policy219 Questions

Exam 33: Budget Deficits in the Short and Long Run215 Questions

Exam 34: The Trade-Off Between Inflation and Unemployment219 Questions

Exam 35: International Trade and Comparative Advantage223 Questions

Exam 36: The International Monetary System: Order or Disorder218 Questions

Exam 37: Exchange Rates and the Macroeconomy219 Questions

Select questions type

Is it a good thing to go to a point where marginal profit is zero?

Explain.

(Essay)

4.7/5  (39)

(39)

Maureen left her teaching job, which paid $30,000 per year, and invested $20,000 of her retirement fund (which was earning 10 percent interest) in a new real estate business.Her accountant predicted a $60,000 revenue the first year.Her husband, an economist, forecast her profit to be

(Multiple Choice)

4.9/5 (40)

A firm can always increase its output by one unit at a marginal cost of $10.Its marginal cost curve is

(Multiple Choice)

4.9/5 (41)

An airline is considering adding a flight from Chicago to Sioux Falls.Total cost of the flight is $5,500.Variable cost is $2,000.Revenue from the flight is expected to be $3,000.Should the flight be added?

(Multiple Choice)

4.9/5 (38)

Business people often use "hunches" and intuition to make decisions regarding what to produce.

(True/False)

4.7/5 (48)

Sally leaves her $24,000 secretarial position with a company and invests her savings of $15,000 (on which she was earning 6 percent interest) in her own Ready Sec agency.After expenses, her net income was $28,900.Her economic profit was

(Multiple Choice)

4.9/5 (31)

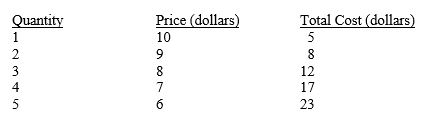

Table 8-3

-Explain how much the firm shown in Table 8-3 should produce, first using total profit and then using marginal analysis.

-Explain how much the firm shown in Table 8-3 should produce, first using total profit and then using marginal analysis.

(Essay)

4.9/5 (34)

"As long as total revenue slopes up, marginal revenue must slope up also." Explain whether this statement is true or false.

(Essay)

4.9/5 (35)

The assumption that firms attempt to maximize profits will yield good predictions even if firms sometimes pursue other goals.

(True/False)

4.8/5 (35)

The term "satisficing" for decision-making behavior by many firms was coined by

(Multiple Choice)

4.9/5 (45)

To find its profit-maximizing output level, a firm should operate where

(Multiple Choice)

4.8/5 (35)

If average cost is falling, then marginal cost must be falling.

(True/False)

4.9/5 (32)

Marginal profit is the addition to a firm's total profit from a

(Multiple Choice)

4.8/5 (36)

Total profit is maximized if the slope of the total profit curve is

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)