Exam 13: Foreign Exchange Risk

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

The use of an exchange rate forward contract assures the FI of the opportunity to buy (or sell) the foreign currency at a future time at a known price.

(True/False)

4.9/5  (33)

(33)

Off-balance-sheet hedging involves taking a position in FX forward or other derivative securities even though no FX assets or liabilities are on the balance sheet.

(True/False)

4.9/5 (35)

Directly matching foreign asset and liability books in the same FX currency will allow an FI to hedge or lock in a profit spread regardless of future changes in exchange rates.

(True/False)

4.7/5 (42)

An FI has purchased (borrowed) a one-year $10 million Eurodollar deposit at an annual interest rate of 6 percent. It has invested these proceeds in one-year Euro (€) bonds at an annual rate of 6.5 percent after converting them at the current spot rate of €1.75/$. Both interest and principal are paid at the end of the year. Assume that instead of investing in Euro bonds at a fixed rate of 6.5 percent, it invests them in variable rates of LIBOR + 1.5 percent, reset every six months. The current LIBOR rate is 5 percent. What is the annual spread earned by the bank if LIBOR at the end of six months is 5.5 percent? Assume both interest and principal will be reinvested in six months. Assume the exchange rate remains at €1.75/$at the end of the year.

(Multiple Choice)

4.8/5 (38)

The market in which foreign currency is traded for future delivery is the forward foreign exchange market.

(True/False)

4.8/5 (36)

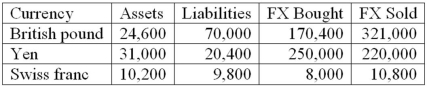

The following are the net currency positions of a Canadian FI (stated in Canadian dollars).  How would you characterize the FI's risk exposure to fluctuations in the British pound to dollar exchange rate?

How would you characterize the FI's risk exposure to fluctuations in the British pound to dollar exchange rate?

(Multiple Choice)

4.8/5 (40)

The decrease in European FX volatility during the last decade has occurred because of

(Multiple Choice)

4.8/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)