Exam 9: Interest Rate Risk II

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

Consider a five-year, 8 percent annual coupon bond selling at par of $1,000. What is the duration of this bond?

(Multiple Choice)

4.8/5  (33)

(33)

Investing in a zero-coupon asset with a maturity equal to the desired investment horizon is one method of immunizing against changes in interest rates.

(True/False)

4.8/5 (34)

Based on an 18-month, 8 percent (semiannual) coupon Treasury note selling at par. If interest rates increase by 20 basis points (i.e., ΔR = 20 basis points), use the duration approximation to determine the approximate price change for the Treasury note.

(Multiple Choice)

4.7/5 (23)

Duration normally is less than the maturity for a fixed income asset.

(True/False)

4.8/5 (30)

The smaller the leverage adjusted duration gap, the more exposed the FI is to interest rate shocks.

(True/False)

4.8/5 (25)

The use of duration to predict changes in bond prices for given changes in interest rate changes will always underestimate the amount of the true price change.

(True/False)

4.8/5 (42)

The economic meaning of duration is the interest elasticity of a financial assets price.

(True/False)

4.7/5 (39)

For given changes in interest rates, the change in the market value of net worth of an FI is equal to the difference between the changes in the market value of the assets and market value of the liabilities.

(True/False)

4.9/5 (32)

A key assumption of Macaulay duration is that the yield curve is flat so that all cash flows are discounted at the same discount rate.

(True/False)

4.8/5 (31)

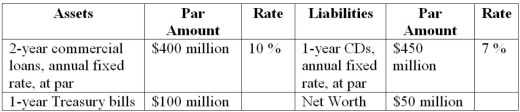

First Duration Bank has the following assets and liabilities on its balance sheet  What is the FI's leverage-adjusted duration gap?

What is the FI's leverage-adjusted duration gap?

(Multiple Choice)

5.0/5 (42)

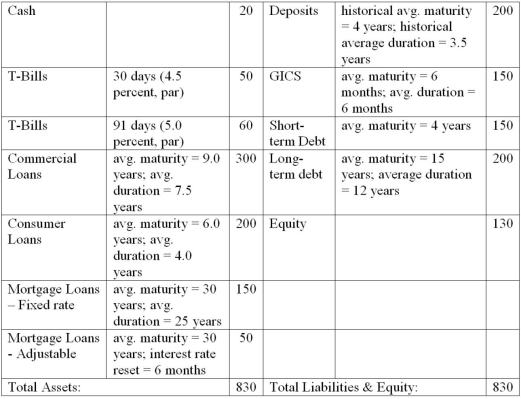

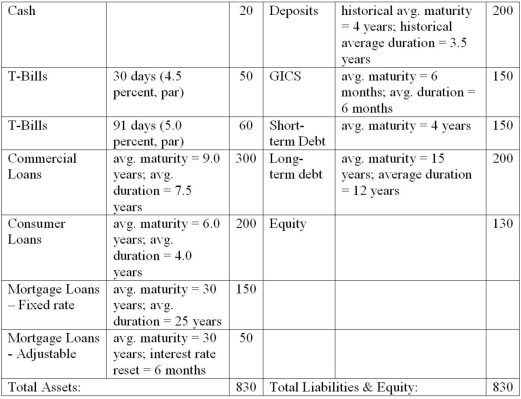

The numbers provided are in millions of dollars and reflect market values:  The short-term debt consists of 4-year bonds paying an annual coupon of 4 percent and selling at par. What is the duration of the short-term debt?

The short-term debt consists of 4-year bonds paying an annual coupon of 4 percent and selling at par. What is the duration of the short-term debt?

(Multiple Choice)

4.8/5 (38)

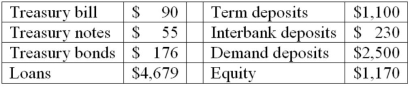

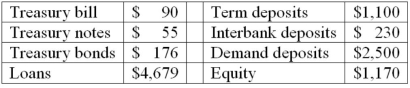

The numbers provided by Fourth Bank of Duration are in thousands of dollars.  Notes: All Treasury bills have six months until maturity. One-year Treasury notes are priced at par and have a coupon of 7 percent paid semiannually. Treasury bonds have an average duration of 4.5 years and the loan portfolio has a duration of 7 years. Term deposits have a 1-year duration and the Interbank deposits duration is 0.003 years. Fourth Bank of Duration assigns a duration of zero (0) to demand deposits. What is the bank's leverage adjusted duration gap?

Notes: All Treasury bills have six months until maturity. One-year Treasury notes are priced at par and have a coupon of 7 percent paid semiannually. Treasury bonds have an average duration of 4.5 years and the loan portfolio has a duration of 7 years. Term deposits have a 1-year duration and the Interbank deposits duration is 0.003 years. Fourth Bank of Duration assigns a duration of zero (0) to demand deposits. What is the bank's leverage adjusted duration gap?

(Multiple Choice)

4.8/5 (32)

The difference between the changes in the market value of the assets and market value of liabilities for a given change in interest rates is, by definition, the change in the FI's net worth.

(True/False)

4.8/5 (41)

The numbers provided by Fourth Bank of Duration are in thousands of dollars.  Notes: All Treasury bills have six months until maturity. One-year Treasury notes are priced at par and have a coupon of 7 percent paid semiannually. Treasury bonds have an average duration of 4.5 years and the loan portfolio has a duration of 7 years. Term deposits have a 1-year duration and the Interbank deposits duration is 0.003 years. Fourth Bank of Duration assigns a duration of zero (0) to demand deposits. If the relative change in interest rates is a decrease of 1 percent, calculate the impact on the bank's market value of equity using the duration approximation.

(That is, ΔR/(1 + R) = -1 percent)

Notes: All Treasury bills have six months until maturity. One-year Treasury notes are priced at par and have a coupon of 7 percent paid semiannually. Treasury bonds have an average duration of 4.5 years and the loan portfolio has a duration of 7 years. Term deposits have a 1-year duration and the Interbank deposits duration is 0.003 years. Fourth Bank of Duration assigns a duration of zero (0) to demand deposits. If the relative change in interest rates is a decrease of 1 percent, calculate the impact on the bank's market value of equity using the duration approximation.

(That is, ΔR/(1 + R) = -1 percent)

(Multiple Choice)

4.9/5 (36)

The numbers provided are in millions of dollars and reflect market values:  A risk manager could restructure assets and liabilities to reduce interest rate exposure for this example by

A risk manager could restructure assets and liabilities to reduce interest rate exposure for this example by

(Multiple Choice)

4.8/5 (26)

In most countries FIs report their balance sheet using market value accounting.

(True/False)

4.8/5 (34)

Attempts to satisfy the objectives of shareholders and regulators requires the bank to use the same duration match in the protection of net worth from interest rate risk.

(True/False)

4.9/5 (24)

Deep discount bonds are semi-annual fixed-rate coupon bonds that sell at a market price that is less than par value.

(True/False)

4.7/5 (38)

Using a fixed-rate bond to immunize a desired investment horizon means that the reinvested coupon payments are not affected by changes in market interest rates.

(True/False)

4.8/5 (36)

Third Duration Investments has the following assets and liabilities on its balance sheet. The two-year Treasury notes are zero coupon assets. Interest payments on all other assets and liabilities occur at maturity. Assume 360 days in a year.  What is the duration of the liabilities?

What is the duration of the liabilities?

(Multiple Choice)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)