Exam 8: Interest Rate Risk I

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

Which theory of term structure argues that individual investors have specific maturity preferences?

(Multiple Choice)

4.9/5  (32)

(32)

A bank with a negative repricing (or funding) gap faces reinvestment risk.

(True/False)

4.8/5 (31)

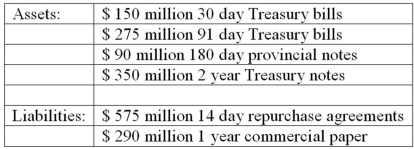

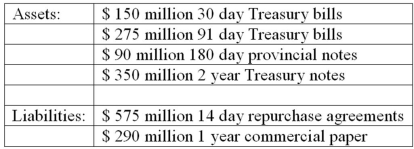

The following are the assets and liabilities of a government security dealer.  Use the repricing model to determine the funding gap for a maturity bucket of 91 days.

Use the repricing model to determine the funding gap for a maturity bucket of 91 days.

(Multiple Choice)

4.7/5 (36)

Because the repricing model ignores the market value effect of changing interest rates, the repricing gap is an incomplete measure of the true interest rate risk exposure of an FI.

(True/False)

4.7/5 (32)

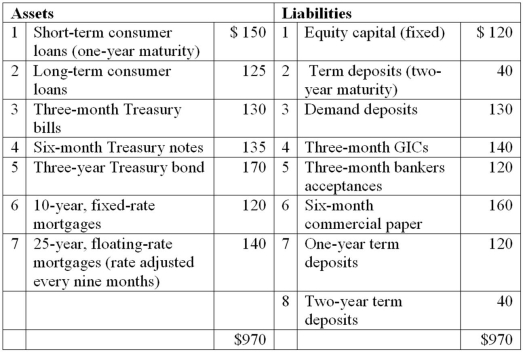

The following is the balance sheet of Victoria Bank. The average maturity of demand deposits is estimated at 2 years.  What is the impact on net interest income in year two if interest rates increase by 50 basis points at the end of year one? Ignore runoffs.

What is the impact on net interest income in year two if interest rates increase by 50 basis points at the end of year one? Ignore runoffs.

(Multiple Choice)

4.8/5 (24)

One reason to include demand deposits when estimating a bank's repricing gap is because rising interest rates could lead to high withdrawals.

(True/False)

4.8/5 (41)

Runoff in demand deposits in a repricing model is typically lower during periods of falling interest rates.

(True/False)

4.7/5 (23)

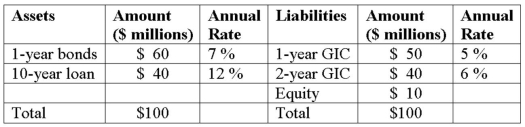

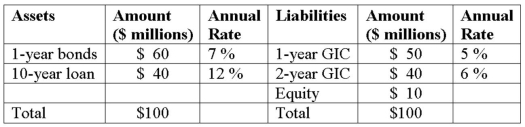

Hadbucks National Bank current balance sheet appears below. All assets and liabilities are currently priced at par and pay interest annually.  Which of the following statements is true?

Which of the following statements is true?

(Multiple Choice)

4.8/5 (31)

Hadbucks National Bank current balance sheet appears below. All assets and liabilities are currently priced at par and pay interest annually.  Can the FI immunize itself from interest rate risk exposure by setting the maturity gap equal to zero?

Can the FI immunize itself from interest rate risk exposure by setting the maturity gap equal to zero?

(Multiple Choice)

4.8/5 (38)

The balance sheet of XYZ Bank appears below. All figures in millions of Canadian dollars.  Suppose that interest rates rise by 2 percent on both RSAs and RSLs. The expected annual change in net interest income of the bank is

Suppose that interest rates rise by 2 percent on both RSAs and RSLs. The expected annual change in net interest income of the bank is

(Multiple Choice)

4.7/5 (30)

If interest rates decrease 50 basis points for an FI that has a gap of +$5 million, the expected change in net interest income is

(Multiple Choice)

4.8/5 (33)

If the interest rate spread between rate sensitive assets and rate sensitive liabilities increases for a bank, future increases in interest rates will lead to an increase in net interest income.

(True/False)

4.9/5 (41)

Which of the following is a weakness of the repricing model to measure interest rate risk?

(Multiple Choice)

4.9/5 (25)

The balance sheet of ARGH Insurance shows the following fixed and rate sensitive assets and liabilities.  What is the repricing gap for the FI?

What is the repricing gap for the FI?

(Multiple Choice)

4.9/5 (42)

The following are the assets and liabilities of a government security dealer.  Use the repricing model to determine the funding gap for a maturity bucket of 30 days.

Use the repricing model to determine the funding gap for a maturity bucket of 30 days.

(Multiple Choice)

4.8/5 (33)

If the chosen maturity buckets have a time period that is too long, the repricing model may produce inaccurate results because

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)