Exam 8: Interest Rate Risk I

Exam 1: Why Are Financial Institutions Special90 Questions

Exam 2: Deposit-Taking Institutions43 Questions

Exam 3: Finance Companies71 Questions

Exam 4: Securities, Brokerage, and Investment Banking91 Questions

Exam 5: Mutual Funds, Hedge Funds, and Pension Funds61 Questions

Exam 6: Insurance Companies80 Questions

Exam 7: Risks of Financial Institutions110 Questions

Exam 8: Interest Rate Risk I110 Questions

Exam 9: Interest Rate Risk II116 Questions

Exam 10: Credit Risk: Individual Loans112 Questions

Exam 11: Credit Risk: Loan Portfolio and Concentration Risk51 Questions

Exam 12: Liquidity Risk85 Questions

Exam 13: Foreign Exchange Risk87 Questions

Exam 14: Sovereign Risk89 Questions

Exam 15: Market Risk95 Questions

Exam 16: Off-Balance-Sheet Risk101 Questions

Exam 17: Technology and Other Operational Risks107 Questions

Exam 18: Liability and Liquidity Management38 Questions

Exam 19: Deposit Insurance and Other Liability Guarantees54 Questions

Exam 20: Capital Adequacy102 Questions

Exam 21: Product and Geographic Expansion114 Questions

Exam 22: Futures and Forwards234 Questions

Exam 23: Options, Caps, Floors, and Collars113 Questions

Exam 24: Swaps95 Questions

Exam 25: Loan Sales83 Questions

Exam 26: Securitization Index98 Questions

Select questions type

Which theory of term structure posits that long-term rates are a geometric average of current and expected short-term interest rates?

(Multiple Choice)

4.8/5  (32)

(32)

The maturity of a portfolio of assets or liabilities is a weighted average of the maturities of the assets or liabilities that comprise that portfolio.

(True/False)

4.8/5 (32)

The balance sheet of ARGH Insurance shows the following fixed and rate sensitive assets and liabilities.  What will be the FI's net interest income at year-end if interest rates do not change?

What will be the FI's net interest income at year-end if interest rates do not change?

(Multiple Choice)

4.7/5 (39)

When the Bank of Canada finds it necessary to slow economic activity, it allows interest rates to fall.

(True/False)

4.7/5 (29)

If interest rates decrease 40 basis points (0.40 percent) for an FI that has a cumulative gap of -$25 million, the expected change in net interest income is

(Multiple Choice)

4.7/5 (32)

The gap ratio is useful because it indicates the scale of the interest rate exposure by dividing the gap by the asset size of the institution.

(True/False)

5.0/5 (32)

The following is the balance sheet of Victoria Bank. The average maturity of demand deposits is estimated at 2 years.  What is the repricing gap if a 3-year maturity gap is used? Ignore runoffs.

What is the repricing gap if a 3-year maturity gap is used? Ignore runoffs.

(Multiple Choice)

4.7/5 (33)

For a given change in interest rates, fixed-rate assets with long-term maturities will have smaller changes in price than assets with shorter maturities.

(True/False)

4.9/5 (35)

Because of its complexity, small deposit-taking institutions rarely use the repricing, or funding gap, model.

(True/False)

4.9/5 (32)

Which theory of term structure states that long-term rates are equal to the geometric average of current and expected short-term rates plus a risk premium that increases with the maturity of the security?

(Multiple Choice)

4.8/5 (30)

The Bank for International Settlements (BIS) requires deposit-taking institutions to have interest rate risk management systems.

(True/False)

4.8/5 (37)

The following information is from First Yaupon Savings Association.  What is the repricing gap over the 1-year maturity bucket?

What is the repricing gap over the 1-year maturity bucket?

(Multiple Choice)

4.8/5 (33)

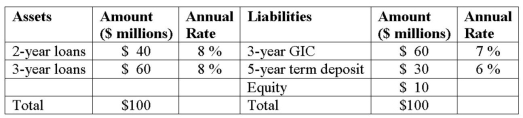

Duration Bank has the following assets and liabilities as of year-end. All assets and liabilities are currently priced at par and pay interest annually.  Is the bank exposed to interest rate increases or decreases and why?

Is the bank exposed to interest rate increases or decreases and why?

(Multiple Choice)

4.9/5 (24)

The market segmentation theory of the term structure of interest rates

(Multiple Choice)

4.8/5 (22)

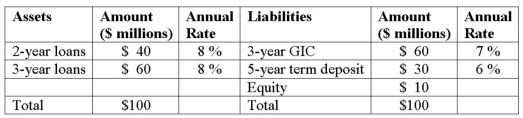

Duration Bank has the following assets and liabilities as of year-end. All assets and liabilities are currently priced at par and pay interest annually.  What is the weighted average maturity of the liabilities of the FI?

What is the weighted average maturity of the liabilities of the FI?

(Multiple Choice)

4.9/5 (27)

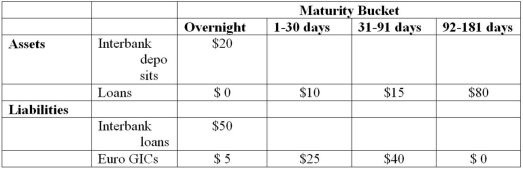

The following information details the current rate sensitivity report for Gotbucks Bank, Inc. ($million).  What does Gotbucks Bank's 91-day gap positions reveal about the bank management's interest rate forecasts and the bank's interest rate risk exposure?

What does Gotbucks Bank's 91-day gap positions reveal about the bank management's interest rate forecasts and the bank's interest rate risk exposure?

(Multiple Choice)

4.7/5 (34)

In general, the interest rate spread (spread effect) between rate sensitive assets and rate sensitive liabilities is positively related to the change in net interest income.

(True/False)

4.8/5 (29)

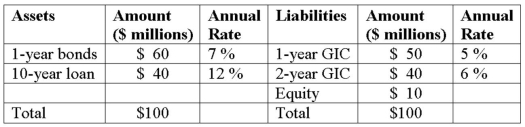

Hadbucks National Bank current balance sheet appears below. All assets and liabilities are currently priced at par and pay interest annually.  What is this FI's maturity gap?

What is this FI's maturity gap?

(Multiple Choice)

4.8/5 (37)

Which of the following describes the condition known as runoff in the repricing model approach to measuring interest rate risk of an FI?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)