Exam 9: Competitive Markets

Exam 1: Economic Issues and Concepts130 Questions

Exam 2: Economic Theories,Data,and Graphs140 Questions

Exam 3: Demand, Supply, and Price161 Questions

Exam 4: Elasticity160 Questions

Exam 5: Price Controls and Market Efficiency125 Questions

Exam 6: Consumer Behaviour140 Questions

Exam 7: Producers in the Short Run144 Questions

Exam 8: Producers in the Long Run141 Questions

Exam 9: Competitive Markets154 Questions

Exam 10: Monopoly, cartels, and Price Discrimination126 Questions

Exam 11: Imperfect Competition and Strategic Behaviour126 Questions

Exam 12: Economic Efficiency and Public Policy123 Questions

Exam 13: How Factor Markets Work123 Questions

Exam 14: Labour Markets and Income Inequality119 Questions

Exam 15: Interest Rates and the Capital Market107 Questions

Exam 16: Market Failures and Government Intervention123 Questions

Exam 17: The Economics of Environmental Protection133 Questions

Exam 18: Taxation and Public Expenditure121 Questions

Exam 19: What Macroeconomics Is All About116 Questions

Exam 20: The Measurement of National Income117 Questions

Exam 21: The Simplest Short-Run Macro Model156 Questions

Exam 22: Adding Government and Trade to the Simple Macro Model132 Questions

Exam 23: Output and Prices in the Short Run142 Questions

Exam 24: From the Short Run to the Long Run: The Adjustment of Factor Prices149 Questions

Exam 25: Long-Run Economic Growth129 Questions

Exam 26: Money and Banking129 Questions

Exam 27: Money, Interest Rates, and Economic Activity135 Questions

Exam 28: Monetary Policy in Canada119 Questions

Exam 29: Inflation and Disinflation122 Questions

Exam 30: Unemployment Fluctuations and the Nairu120 Questions

Exam 31: Government Debt and Deficits129 Questions

Exam 32: The Gains From International Trade127 Questions

Exam 33: Trade Policy126 Questions

Exam 34: Exchange Rates and the Balance of Payments161 Questions

Select questions type

Which of the following conditions is true of a perfectly competitive industry when it is in long-run equilibrium?

Free

(Multiple Choice)

5.0/5  (40)

(40)

Correct Answer: Verified

Verified

C

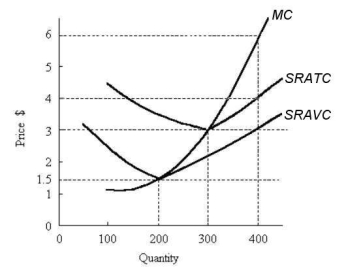

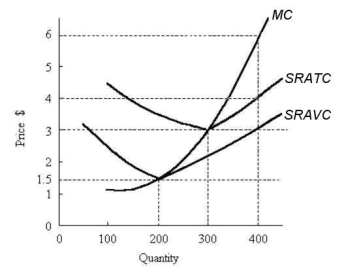

Consider the following short-run cost curves for a profit-maximizing firm in a perfectly competitive industry.  FIGURE 9-2

-Refer to Figure 9-2.The short-run supply curve for the industry in which this firm operates is

FIGURE 9-2

-Refer to Figure 9-2.The short-run supply curve for the industry in which this firm operates is

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

E

Comparing the short-run and long-run profit-maximizing positions of a perfectly competitive firm,which statement is true?

Free

(Multiple Choice)

4.8/5 (28)

Correct Answer:Verified

D

Consider the following cost curves for Firm X,a perfectly competitive firm.  FIGURE 9-5

-Refer to Figure 9-5.In this industry,which one of the following is FALSE?

FIGURE 9-5

-Refer to Figure 9-5.In this industry,which one of the following is FALSE?

(Multiple Choice)

5.0/5 (31)

Suppose ABC Corp.is a firm producing newsprint in a perfectly competitive industry.Its output is 1500 tonnes per month,the marginal cost of the last tonne produced is $710,and the average revenue per tonne is $620.In the short run,this firm should

(Multiple Choice)

5.0/5 (41)

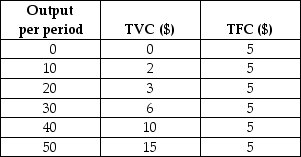

Consider the following total cost schedule for a perfectly competitive firm producing ball-point pens.

TABLE 9-3

-Refer to Table 9-3.What is the marginal cost of producing the 35th unit of output?

TABLE 9-3

-Refer to Table 9-3.What is the marginal cost of producing the 35th unit of output?

(Multiple Choice)

4.8/5 (42)

In the short run,a profit-maximizing firm will expand output

(Multiple Choice)

4.8/5 (26)

Consider the following short-run cost curves for a profit-maximizing firm in a perfectly competitive industry.  FIGURE 9-2

-Refer to Figure 9-2.If the current market price is $6,the profit-maximizing output for this firm is

FIGURE 9-2

-Refer to Figure 9-2.If the current market price is $6,the profit-maximizing output for this firm is

(Multiple Choice)

4.8/5 (30)

Consider a perfectly competitive firm when its industry is in long-run equilibrium.Which of the following statements is correct?

(Multiple Choice)

4.8/5 (32)

Suppose a typical firm in a competitive industry has the following data in the short run: price = $5000; output = 1 million units; ATC = $5300; AVC = $4750.What will likely happen in the long run?

(Multiple Choice)

4.9/5 (37)

Which of the following statements is one of the assumptions of the theory of perfect competition?

(Multiple Choice)

4.9/5 (37)

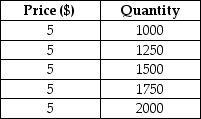

Consider the price and quantity data below for a perfectly competitive firm producing mousetraps.

TABLE 9-1

-Refer to Table 9-1.Suppose this firm is currently selling 1750 mousetraps at the market price of $5.If the firm raises its price to $6,it's average revenue will be

TABLE 9-1

-Refer to Table 9-1.Suppose this firm is currently selling 1750 mousetraps at the market price of $5.If the firm raises its price to $6,it's average revenue will be

(Multiple Choice)

4.8/5 (37)

9.3 Short-Run Decisions

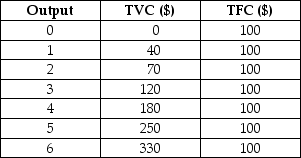

Assume the following total cost schedule for a perfectly competitive firm.

TABLE 9-2

-Refer to Table 9-2.This profit-maximizing firm would produce no output in the short run if the market price of its output dropped below

TABLE 9-2

-Refer to Table 9-2.This profit-maximizing firm would produce no output in the short run if the market price of its output dropped below

(Multiple Choice)

4.9/5 (33)

For any firm operating in any market structure,marginal revenue is defined as

(Multiple Choice)

4.7/5 (37)

Average revenue (AR)for an individual firm in a perfectly competitive market equals

(Multiple Choice)

4.7/5 (34)

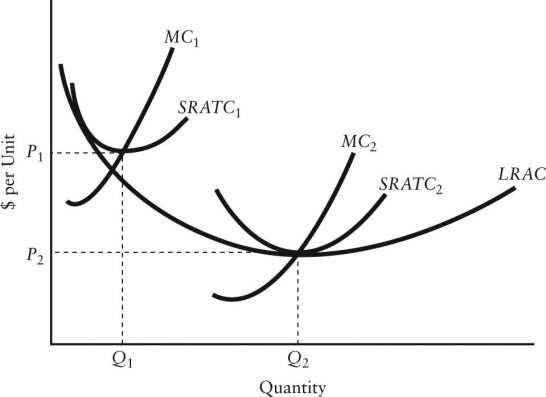

Consider the following statement of equalities: P = MC = minimum SRATC = minimum LRAC.This statement of equalities best applies to which of the following?

(Multiple Choice)

4.8/5 (36)

9.3 Short-Run Decisions

Assume the following total cost schedule for a perfectly competitive firm.

TABLE 9-2

-Refer to Table 9-2.What is the marginal cost of producing the 5th unit of output?

(Multiple Choice)

4.8/5 (33)

Suppose that in a perfectly competitive industry,the market price of the product is $12.Firm A is producing the output level at which average total cost equals marginal cost,both of which are $10.To maximize its profits,Firm A should

(Multiple Choice)

4.9/5 (28)

Which of the following assumptions about perfectly competitive markets is primarily responsible for firms having zero economic profit in long run equilibrium?

(Multiple Choice)

4.9/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)