Exam 18: Accounting for Share-Based Payments

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

AASB 2 requires some share-based payments to be recognised in an entity's financial statements.

(True/False)

4.8/5  (40)

(40)

AASB 2 requires the re-measurement of cash-settled transactions at fair value at reporting date.

(True/False)

4.8/5 (41)

What is the journal entry to recognise salary expense for Southport Ltd.related to the share appreciation rights issued 1 July 2009 for the year ended 30 June 2011?

(Multiple Choice)

4.7/5 (37)

What would be the appropriate journal entry to account for the share-based payment transaction for the year ending 30 June 2012?

(Multiple Choice)

4.8/5 (30)

What is the Employee benefits expense of Liverpool Ltd related to this share option for the year ended 30 June 2011?

(Multiple Choice)

4.8/5 (47)

Which of the following items are considered share-based payment transactions within the scope of AASB 2?

(Multiple Choice)

4.7/5 (42)

AASB 2 does not require expensing of cash-settled share- based payment transactions until settlement date.

(True/False)

4.8/5 (31)

If an entity alters the conditions of the options after issue,AASB 2 requires the effects of such modifications to be recognised.

(True/False)

4.9/5 (34)

AASB 2 requires all equity-settled share-based payment transactions be measured at fair value of goods and services received.

(True/False)

4.9/5 (43)

On 30 June 2010,based on probability estimates how many employees are expected to be employed by Windermere Ltd when the share vests?

(Multiple Choice)

4.9/5 (34)

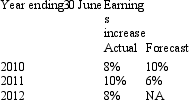

On 1 July 2009,Manchester Ltd granted 50,000 share options to its Chief Executive Officer with an exercise price of $40 per share,conditional upon the entity achieving the following non-market vesting conditions:  Earnings information available follows:

Earnings information available follows:

In accordance with AASB 2,when will this share option vest?

In accordance with AASB 2,when will this share option vest?

(Multiple Choice)

4.9/5 (42)

What is the journal entry to recognise salary expense for Southport Ltd.related to the share appreciation rights issued 1 July 2009 for the year ended 30 June 2014?

(Multiple Choice)

4.9/5 (36)

A share-based payment is a transaction which entitles another party to receive a cash payment with the amount paid dependent on the price of the entity's shares or other equity instruments.

(True/False)

4.7/5 (35)

What action must Wigan Ltd take that is in compliance with AASB 2,if the option does not vest on 30 June 2012?

(Multiple Choice)

4.7/5 (39)

Penneshaw Ltd grants 100 options to each of its 50 employees on 1 July 2009.Each grant is conditional on the employee working for the company for 3 years.The fair value of each option at grant date is $15. The following information is available:

What is the employee benefits expense of Penneshaw Ltd related to this share option for the year ended 30 June 2012?

What is the employee benefits expense of Penneshaw Ltd related to this share option for the year ended 30 June 2012?

(Multiple Choice)

4.7/5 (34)

In a cash-settled share-based payment transaction,the entity shall remeasure the fair value of the liability at each reporting date and at the date of settlement,with any changes in fair value recognised in profit or loss for the period.

(True/False)

4.8/5 (36)

What would be the appropriate journal entry to account for the share-based payment transaction for the year ending 30 June 2011?

(Multiple Choice)

4.9/5 (32)

What is/are the journal entry/ies to recognise salary expense for Southport Ltd.related to the share appreciation rights issued 1 July 2009 for the year ended 30 June 2012?

(Multiple Choice)

4.7/5 (36)

On 30 June 2012,based on probability estimates how many employees are expected to be employed by Windermere Ltd when the share vests?

(Multiple Choice)

4.9/5 (44)

In share-based payment transactions with cash alternatives,the entity shall measure the equity component of the compound financial instrument as the difference between the fair value of the goods or services received and the fair value of the debt component,measured at vesting date.

(True/False)

4.9/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)