Exam 6: Revaluation and Impairment Testing of Non-Current Assets

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

Revaluations increments are often a source of discussion because:

(Multiple Choice)

4.8/5  (40)

(40)

AASB 116 requires that revaluation increments and decrements must be offset recorded directly to equity and not be recorded as a gain or loss:

(True/False)

4.7/5 (38)

Palm Beach Ltd has elected to adopt the allowed alternative treatment to account for some of its property,plant and equipment.The information available for the class of assets the entity wishes to covert to revaluation model follows:  Which of the following statements are correct if Palm Beach Ltd is to comply with AASB 116?

Which of the following statements are correct if Palm Beach Ltd is to comply with AASB 116?

(Multiple Choice)

4.8/5 (32)

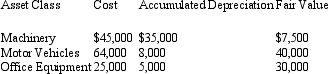

Hendersons Ltd has just begun to revalue its plant and equipment.The following information about the items included in this class of non-current assets shows their carrying value,and most recent revaluation.  What is/are the appropriate journal entry(ies)to record the revaluations?

What is/are the appropriate journal entry(ies)to record the revaluations?

(Multiple Choice)

5.0/5 (39)

Positive accounting theory suggests that the revalution model is income increasing because the credit is asset revaluation reserve:

(True/False)

4.8/5 (32)

Which of the following statements is a valid reason to select cost model over the revaluation model?

(Multiple Choice)

4.8/5 (33)

Purple Co Ltd purchased an item of land 3 years ago at a cost of $700 000.Two years ago the recoverable value of the land was considered to be $550 000.In the current period the land is revalued and the fair value is now $750 000.What is the treatment of the change in value in each of the periods?

(Multiple Choice)

4.8/5 (39)

Australia is the only country that allows upward revaluations of non-current assets:

(True/False)

4.8/5 (38)

Brahms Ltd acquired a property of land and building for $1.5 million.Management estimates the value of land to be 40% of cost.The building is estimated to have a useful life of 50 years.After 25 years,the property was revalued at 1.2 million.It is expected that the life of building will remain the same and salvage value is expected to be $100,000.What is the revaluation gain(loss)for building and the depreciation expense one year after revaluation?

(Multiple Choice)

4.8/5 (31)

Once a class of non-current assets has been revalued,AASB 116 requires that:

(Multiple Choice)

4.9/5 (38)

Depreciation method used and depreciation rates are required to be disclosed for taxation purposes.

(True/False)

4.7/5 (35)

AASB 116 prescribes that,if assets within the same class are revalued and some assets increased in value while others decreased in value:

(Multiple Choice)

4.9/5 (27)

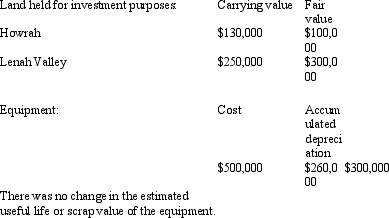

Stairway Ltd is undertaking its regular review of the fair value of its assets.It has discovered the following material changes:  What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

What are the journal entries required to record the revaluations in accordance with relevant accounting standards?

(Multiple Choice)

4.8/5 (37)

Seagull Marinas Ltd owns land that was purchased for $300,000 to be used as the future site of a boat shed.Due to the development of a resort in the vicinity,the land's fair market value had risen to $480,000 on 30 June 2002.A revaluation undertaken on 30 June 2005 of $150,000 reflects the effect of the failure of resort development and local concerns about the protection of the nesting sites of endangered sea birds located near the land.What are the journal entries required to record the revaluations on 30 June 2002 and 30 June 2005?

(Multiple Choice)

4.8/5 (34)

Pigeon Ltd purchased land for $750,000 6 years ago.It was revalued on 31 December 2002 to $600,000.A subsequent revaluation on 31 December 2004 found the market value to be $900,000 due to a change in council zoning for the area.What are the journal entries required to record the revaluations on 31 December 2002 and 31 December 2004?

(Multiple Choice)

4.9/5 (41)

Chopin Ltd has a debt contract and is close to violating the return on equity ratio as stipulated in the debt agreement.What is the most appropriate action to take?

(Multiple Choice)

4.8/5 (39)

Smith & Jones Ltd owns equipment that was purchased for $56,000 and has accumulated depreciation of $14,000.The following market value information was gathered about the equipment:  The equipment has a remaining useful life to the entity of 10 years.What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

The equipment has a remaining useful life to the entity of 10 years.What are the appropriate journal entries to record the revaluation under the gross method and the net-amount method?

(Multiple Choice)

4.9/5 (37)

A class of non-current assets as defined by AASB 116 is a category of non-current assets that:

(Multiple Choice)

4.9/5 (40)

Recoverable amount is the amount expected to be recovered through the ongoing use and subsequent disposal of an asset:

(True/False)

4.7/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)