Exam 15: Alternative Minimum Tax

Exam 1: An Introduction to Taxation and Understanding the Federal Tax Law159 Questions

Exam 2: Working With the Tax Law85 Questions

Exam 3: Computing the Tax150 Questions

Exam 4: Gross Income: Concepts and Inclusions125 Questions

Exam 5: Gross Income: Exclusions116 Questions

Exam 6: Deductions and Losses: in General153 Questions

Exam 7: Deductions and Losses: Certain Business Expenses and Losses97 Questions

Exam 8: Depreciation, Cost Recovery, Amortization, and Depletion116 Questions

Exam 9: Deductions: Employee and Self-Employed-Related Expenses166 Questions

Exam 10: Deductions and Losses: Certain Itemized Deductions106 Questions

Exam 11: Investor Losses103 Questions

Exam 12: Tax Credits and Payments109 Questions

Exam 13: Property Transactions: Determination of Gain or Loss, Basis Considerations, and Nontaxable Exchanges-Part 1200 Questions

Exam 13: Property Transactions: Determination of Gain or Loss, Basis Considerations, and Nontaxable Exchanges-Part 292 Questions

Exam 14: Property Transactions: Capital Gains and Losses, 1231, Recapture Provisions144 Questions

Exam 15: Alternative Minimum Tax125 Questions

Exam 16: Accounting Periods and Methods87 Questions

Exam 17: Corporations: Introduction and Operating Rules109 Questions

Exam 18: Corporations: Organization and Capital Structure93 Questions

Exam 19: Corporations: Distributions Not in Complete Liquidation145 Questions

Exam 20: Corporations: Distributions in Complete Liquidation and an Overview of Reorganizations70 Questions

Exam 21: Partnerships159 Questions

Exam 22: S: Corporations159 Questions

Exam 23: Exempt Entities151 Questions

Exam 24: Multistate Corporate Taxation145 Questions

Exam 25: Taxation of International Transactions148 Questions

Exam 26: Tax Practice and Ethics147 Questions

Exam 28: Income Taxation of Trusts and Estates145 Questions

Select questions type

C corporations are subject to a positive AMT adjustment equal to 75% of the excess of ACE over AMTI before the ACE adjustment.

(True/False)

4.9/5  (39)

(39)

Marvin, the vice president of Lavender, Inc., exercises stock options for 100 shares of stock in March 2012. The stock options are incentive stock options (ISOs). Their exercise price is $20 and the fair market value on the date of exercise is $28. The options were granted in March 2009 and all restrictions on the free transferability had lapsed by the exercise date.

(Multiple Choice)

4.9/5 (31)

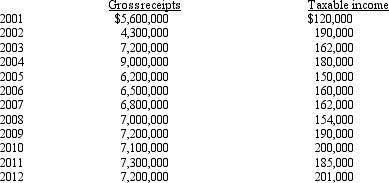

Sage, Inc., has the following gross receipts and taxable income:

Is Sage, Inc., subject to the AMT in 2012?

Is Sage, Inc., subject to the AMT in 2012?

(Essay)

4.9/5 (40)

The AMT exemption for a C corporation is $40,000 reduced by 35% of the amount by which AMTI exceeds $150,000.

(True/False)

4.8/5 (27)

The C corporation AMT rate can be higher than the individual AMT rates.

(True/False)

4.8/5 (34)

Miriam, who is a head of household and age 36, provides you with the following information from her financial records for 2012.  Calculate her AMTI for 2012.

Calculate her AMTI for 2012.

(Multiple Choice)

4.8/5 (39)

If the regular income tax deduction for medical expenses is $0, under certain circumstances the AMT deduction for medical expenses can be greater than $0.

(True/False)

4.7/5 (40)

What is the relationship between the regular income tax liability and the tentative AMT?

(Essay)

4.8/5 (36)

Durell owns a construction company that builds residential housing.The company is eligible to use the completed contract method for regular income tax purposes.What can Durell do to minimize his AMT?

(Essay)

4.8/5 (39)

In 2012, Ben exercised an incentive stock option (ISO), acquiring stock with a fair market value of $190,000 for $170,000.His AMT basis for the stock is $170,000, his regular income tax basis for the stock is $170,000, and his AMT adjustment is $0 ($170,000 - $170,000).

(True/False)

4.8/5 (34)

Kay, who is single, had taxable income of $0 in 2012.She has positive timing adjustments of $206,300 and exclusion items of $100,000 for the year.What is the amount of her alternative minimum tax credit for carryover to 2013?

(Multiple Choice)

4.8/5 (35)

Akeem, who does not itemize, incurred a net operating loss (NOL) of $50,000 in 2012.His deductions in 2012 included AMT tax preference items of $20,000, and he had no AMT adjustments.Assuming the NOL is not carried back, what is Akeem's ATNOLD carryover to 2013?

(Multiple Choice)

4.8/5 (34)

For individual taxpayers, the AMT credit is applicable for the AMT that results from timing differences, but it is not available for the AMT that results from the adjustment for itemized deductions or exclusion preferences.

(True/False)

4.9/5 (30)

Danica owned a car that she used exclusively for business.The car was purchased in 2010 and sold in 2012 for a recognized gain of $9,000.However, the sale resulted in no AMT.Why?

(Essay)

4.8/5 (39)

Kerri, who had AGI of $120,000, itemized her deductions in the current year.She incurred unreimbursed employee business expenses of $8,500.Kerri must make a positive AMT adjustment of $2,400 in computing AMT.

(True/False)

4.9/5 (39)

Why is there a need for a second tax system called the alternative minimum tax?

(Essay)

4.8/5 (36)

The sale of business property might result in an AMT adjustment.

(True/False)

4.8/5 (34)

AGI is used as the base for application of percentage limitations (i.e., 20%, 30%, 50%) that apply to the charitable contribution deduction for regular income tax purposes. Modified AGI is used as the base for application of percentage limitations that apply to the charitable contribution deduction for AMT purposes.

(True/False)

5.0/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)