Exam 15: Alternative Minimum Tax

Exam 1: An Introduction to Taxation and Understanding the Federal Tax Law159 Questions

Exam 2: Working With the Tax Law85 Questions

Exam 3: Computing the Tax150 Questions

Exam 4: Gross Income: Concepts and Inclusions125 Questions

Exam 5: Gross Income: Exclusions116 Questions

Exam 6: Deductions and Losses: in General153 Questions

Exam 7: Deductions and Losses: Certain Business Expenses and Losses97 Questions

Exam 8: Depreciation, Cost Recovery, Amortization, and Depletion116 Questions

Exam 9: Deductions: Employee and Self-Employed-Related Expenses166 Questions

Exam 10: Deductions and Losses: Certain Itemized Deductions106 Questions

Exam 11: Investor Losses103 Questions

Exam 12: Tax Credits and Payments109 Questions

Exam 13: Property Transactions: Determination of Gain or Loss, Basis Considerations, and Nontaxable Exchanges-Part 1200 Questions

Exam 13: Property Transactions: Determination of Gain or Loss, Basis Considerations, and Nontaxable Exchanges-Part 292 Questions

Exam 14: Property Transactions: Capital Gains and Losses, 1231, Recapture Provisions144 Questions

Exam 15: Alternative Minimum Tax125 Questions

Exam 16: Accounting Periods and Methods87 Questions

Exam 17: Corporations: Introduction and Operating Rules109 Questions

Exam 18: Corporations: Organization and Capital Structure93 Questions

Exam 19: Corporations: Distributions Not in Complete Liquidation145 Questions

Exam 20: Corporations: Distributions in Complete Liquidation and an Overview of Reorganizations70 Questions

Exam 21: Partnerships159 Questions

Exam 22: S: Corporations159 Questions

Exam 23: Exempt Entities151 Questions

Exam 24: Multistate Corporate Taxation145 Questions

Exam 25: Taxation of International Transactions148 Questions

Exam 26: Tax Practice and Ethics147 Questions

Exam 28: Income Taxation of Trusts and Estates145 Questions

Select questions type

Vicki owns and operates a news agency (as a sole proprietorship). During 2012, she incurred expenses of $24,000 to increase circulation of newspapers and magazines that her agency distributes. For regular income tax purposes, she elected to expense the $24,000 in 2012. In addition, Vicki incurred $15,000 in circulation expenditures in 2013 and again elected expense treatment.What AMT adjustments will be required in 2012 and 2013 as a result of the circulation expenditures?

(Multiple Choice)

4.8/5  (40)

(40)

Vinny's AGI is $220,000.He contributed $130,000 in cash to the Boy Scouts, a public charity.What is Vinny's charitable contribution deduction for AMT purposes?

(Multiple Choice)

4.7/5 (42)

The phaseout of the AMT exemption amount for a taxpayer filing as a head of household both begins and ends at a higher income level than it does for a single taxpayer.

(True/False)

4.8/5 (33)

If a gambling loss itemized deduction is permitted for regular income tax purposes, there will be no AMT adjustment associated with the gambling loss.

(True/False)

4.8/5 (30)

Lavender, Inc., incurs research and experimental expenditures of $210,000 in 2012.Determine the amount of the AMT adjustment for 2012 and for 2013 if for regular income tax purposes:

(Essay)

4.9/5 (37)

If circulation expenditures are amortized over a ten-year period for regular income tax purposes, there will be no AMT adjustment.

(True/False)

4.8/5 (46)

All of a C corporation's AMT is available for carryover as a minimum tax credit regardless of whether the adjustments and preferences originate from timing differences or AMT exclusions.

(True/False)

4.9/5 (38)

If the taxpayer elects to capitalize intangible drilling costs and to amortize them over a 10-year period for regular income tax purposes, there is no adjustment or preference for AMT purposes.

(True/False)

4.8/5 (40)

If a taxpayer deducts the standard deduction in calculating regular taxable income, what effect does this have in calculating AMTI?

(Essay)

4.8/5 (32)

Keosha acquires 10-year personal property to use in her business in 2012 and takes the maximum cost recovery deduction for regular income tax purposes. As a result of this, Keosha will have a positive AMT adjustment in 2012.

(True/False)

4.7/5 (36)

If Jessica exercises an ISO and disposes of the option in the same tax year, are any AMT adjustments required?

(Essay)

4.9/5 (38)

Discuss the tax year in which an AMT adjustment is first required for an ISO.

(Essay)

4.8/5 (40)

Prior to the effect of tax credits, Wayne's regular income tax liability is $175,000 and his tentative AMT is $150,000.Wayne has nonrefundable business tax credits of $40,000.Wayne's tax liability is $135,000.

(True/False)

5.0/5 (43)

Ted, who is single, owns a personal residence in the city.He also owns a condo near the ocean.He uses the condo as a vacation home.In March 2012, he borrowed $50,000 on a home equity loan and used the proceeds to acquire a luxury automobile.During 2012, he paid the following amounts of interest:  What amount, if any, must Ted recognize as an AMT adjustment in 2012?

What amount, if any, must Ted recognize as an AMT adjustment in 2012?

(Multiple Choice)

4.8/5 (38)

Andrea, who is single, has a personal exemption deduction in calculating her 2012 taxable income.She has no dependency deductions.What is the amount of the AMT adjustment in calculating AMTI?

(Essay)

4.9/5 (35)

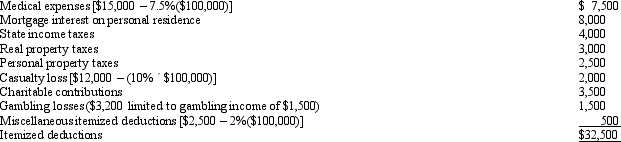

Luke's itemized deductions in calculating taxable income are as follows:

(Essay)

4.9/5 (37)

Tricia sold land that originally cost $105,000 for $112,000.There is a positive AMT adjustment of $7,000 associated with the sale of the land.

(True/False)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)