Exam 3: Computing the Tax

Exam 1: An Introduction to Taxation and Understanding the Federal Tax Law195 Questions

Exam 2: Working With the Tax Law86 Questions

Exam 3: Computing the Tax187 Questions

Exam 4: Gross Income: Concepts and Inclusions124 Questions

Exam 5: Gross Income: Exclusions113 Questions

Exam 6: Deductions and Losses: in General146 Questions

Exam 7: Deductions and Losses: Certain Business Expenses and Losses95 Questions

Exam 8: Depreciation, cost Recovery, amortization, and Depletion103 Questions

Exam 9: Deductions: Employee and Self-Employed-Related Expenses181 Questions

Exam 10: Deductions and Losses: Certain Itemized Deductions105 Questions

Exam 11: Investor Losses111 Questions

Exam 12: Tax Credits and Payments118 Questions

Exam 13: Property Transactions: Determination of Gain or Loss, basis Considerations, and Nontaxable Exchanges280 Questions

Exam 14: Property Transactions, capital Gains and Losses, sec1231, and Recapture Provisions145 Questions

Exam 15: Alternative Minimum Tax132 Questions

Exam 16: Accounting Periods and Methods91 Questions

Exam 17: Corporations: Introduction and Operating Rules112 Questions

Exam 18: Corporations: Organization and Capital Structure93 Questions

Exam 19: Corporations: Distributions Not in Complete Liquidation192 Questions

Exam 20: Corporations: Distributions in Complete Liquidation and an Overview of Reorganization72 Questions

Exam 21: Partnerships163 Questions

Exam 22: S Corporations145 Questions

Exam 23: Exempt Entities141 Questions

Exam 24: Multistate Corporate Taxation196 Questions

Exam 25: Taxation of International Transactions164 Questions

Exam 26: Tax Practice and Ethics183 Questions

Exam 27: The Federal Gift and Estate Taxes167 Questions

Exam 28: Income Taxation of Trusts and Estates167 Questions

Select questions type

Regarding dependency exemptions, classify each statement in one of the four categories:

a.Could be a qualifying child.

b.Could be a qualifying relative.

c.Could be either a qualifying child or a qualifying relative.

d.Could be neither a qualifying child nor a qualifying relative.

-A niece who lives with taxpayer,is 20 years old,earns $5,000,and is a full-time student.

(Short Answer)

4.8/5  (40)

(40)

Because they appear on page 1 of Form 1040,itemized deductions are also referred to as "page 1 deductions."

(True/False)

4.7/5 (38)

For 2017,Tom has taxable income of $48,005.When he uses the Tax Tables,Tom finds that his tax liability is higher than under the Tax Rate Schedules.

a.Why is there a difference?

b.Can Tom use the Tax Rate Schedules?

(Essay)

4.7/5 (40)

The basic and additional standard deductions both are subject to an annual adjustment for inflation.

(True/False)

4.8/5 (36)

In early 2017,Ben sold a yacht,held for 9 months and for pleasure,for a $5,000 gain.Concerned about offsetting the gain before year-end,Ben is considering selling one of the following-each of which would yield a $5,000 loss:

∙ Houseboat used for recreation.

∙ Truck used in business.

∙ Stock investment held for 13 months.

Evaluate each choice.

(Essay)

4.9/5 (36)

Kirby is in the 15% tax bracket and had the following capital asset transactions during 2017:

Kirby's tax consequences from these gains are as follows:

(Multiple Choice)

4.8/5 (41)

Kyle and Liza are married and under 65 years of age.During 2017,they furnish more than half of the support of their 19-year old daughter,May,who lives with them.She graduated from high school in May 2016.May earns $15,000 from a part-time job,most of which she sets aside for future college expenses.Kyle and Liza also provide more than half of the support of Kyle's cousin who lives with them.Liza's father,who died on January 3,2017,at age 90,has for many years qualified as their dependent.How many personal and dependency exemptions should Kyle and Liza claim?

(Multiple Choice)

4.8/5 (37)

Regarding dependency exemptions, classify each statement in one of the four categories:

a.Could be a qualifying child.

b.Could be a qualifying relative.

c.Could be either a qualifying child or a qualifying relative.

d.Could be neither a qualifying child nor a qualifying relative.

-An ex-husband (divorce occurred last year) who lives with taxpayer.

(Short Answer)

4.8/5 (37)

Match the statements that relate to each other. Note: Some choices may be used more than once.

a.Not available to 65-year old taxpayer who itemizes.

b.Exception for U.S. citizenship or residency test (for dependency exemption purposes).

c.Largest basic standard deduction available to a dependent who has no earned income.

d.Considered for dependency exemption purposes.

e.Qualifies for head of household filing status.

f.A child (age 15) who is a dependent and has only earned income.

g.Considered in applying gross income test (for dependency exemption purposes).

h.Not considered in applying the gross income test (for dependency exemption purposes).

i.Unmarried taxpayer who can use the same tax rates as married persons filing jointly.

j.Exception to the support test (for dependency exemption purposes).

k.A child (age 16) who is a dependent and has only unearned income of $4,500.

l.No correct match provided.

-Multiple support agreement

(Short Answer)

4.9/5 (35)

In resolving qualified child status for dependency exemption purposes,why are tiebreaker rules necessary? Can these rules be waived?

(Essay)

4.8/5 (41)

When the kiddie tax applies,the child need not file an income tax return because the child's income will be reported on the parents' return.

(True/False)

4.9/5 (45)

Match the statements that relate to each other. Note: Some choices may be used more than once.

a.Not available to 65-year old taxpayer who itemizes.

b.Exception for U.S. citizenship or residency test (for dependency exemption purposes).

c.Largest basic standard deduction available to a dependent who has no earned income.

d.Considered for dependency exemption purposes.

e.Qualifies for head of household filing status.

f.A child (age 15) who is a dependent and has only earned income.

g.Considered in applying gross income test (for dependency exemption purposes).

h.Not considered in applying the gross income test (for dependency exemption purposes).

i.Unmarried taxpayer who can use the same tax rates as married persons filing jointly.

j.Exception to the support test (for dependency exemption purposes).

k.A child (age 16) who is a dependent and has only unearned income of $4,500.

l.No correct match provided.

-Kiddie tax does not apply

(Short Answer)

4.7/5 (47)

Married taxpayers who file a joint return cannot later (i.e.,after the filing due date) switch to separate returns for that year.

(True/False)

4.9/5 (44)

The Dargers have itemized deductions that exceed the standard deduction.However,when they file their joint return,they choose the standard deduction option.

a.Is this proper procedure?

b.Aside from a possible misunderstanding as to the tax law, what might be the reason for the Darger's choice?

(Essay)

4.9/5 (38)

Match the statements that relate to each other.

a.Available to a 70-year-old father claimed as a dependent by his son.

b.Equal to tax liability divided by taxable income.

c.The highest income tax rate applicable to a taxpayer.

d.Not eligible for the standard deduction.

e.No one qualified taxpayer meets the support test.

f.Taxpayer's ex-husband does not qualify.

g.A dependent child (age 18) who has only unearned income.

h.Highest applicable rate is 39.6%.

i.Applicable rate could be as low as 0%.

j.Maximum rate is 28%.

k.Income from foreign sources is not subject to tax.

l.No correct match provided.

-Average income tax rate

(Short Answer)

4.9/5 (29)

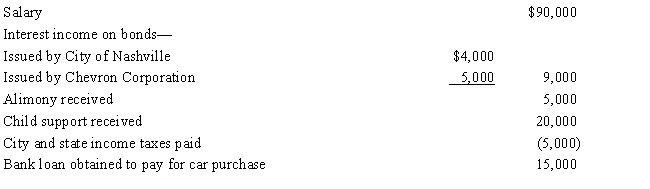

Emily had the following transactions during 2016:

What is Emily's AGI for 2017?

(Essay)

4.8/5 (28)

In determining whether the gross income test is met for dependency exemption purposes,only the taxable portion of a scholarship is considered.

(True/False)

4.9/5 (33)

Maude's parents live in another state and she cannot claim them as her dependents.If Maude pays their medical expenses,can she derive any tax benefit from doing so? Explain.

(Essay)

4.8/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)