Exam 6: Inventories and Cost of Sales

Exam 1: Accounting in Business245 Questions

Exam 2: Analyzing and Recording Transactions201 Questions

Exam 3: Adjusting Accounts and Preparing Financial Statements227 Questions

Exam 4: Completing the Accounting Cycle177 Questions

Exam 5: Accounting for Merchandising Operations189 Questions

Exam 6: Inventories and Cost of Sales194 Questions

Exam 7: Accounting Information Systems166 Questions

Exam 8: Cash and Internal Controls195 Questions

Exam 9: Accounting for Receivables162 Questions

Exam 10: Long-Term Assets208 Questions

Exam 11: Current Liabilities and Payroll Accounting178 Questions

Exam 12: Accounting for Partnerships141 Questions

Exam 13: Accounting for Corporations210 Questions

Exam 14: Long-Term Liabilities158 Questions

Exam 15: Investments and International Operations156 Questions

Exam 16: Statement of Cash Flows173 Questions

Exam 17: Analysis of Financial Statements182 Questions

Exam 18: Managerial Accounting Concepts and Principles199 Questions

Exam 19: Job Order Cost Accounting165 Questions

Exam 20: Process Cost Accounting172 Questions

Exam 21: Cost Allocation and Performance Measurement173 Questions

Exam 22: Cost-Volume-Profit Analysis190 Questions

Exam 23: Master Budgets and Planning166 Questions

Exam 24: Flexible Budgets and Standard Costs178 Questions

Exam 25: Capital Budgeting and Managerial Decisions153 Questions

Select questions type

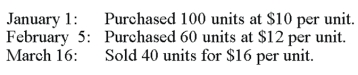

Using the information given below, prepare the general journal entry to record the March 16 sale assuming a cash sale and the LIFO method is used:

(Essay)

4.9/5  (38)

(38)

The matching principle is used by some companies to avoid allocating incidental inventory costs to cost of goods sold.

(True/False)

4.9/5 (39)

Louise Company reported the following income statement information for Year 1 and Year 2: The beginning inventory balance for Year 1 is correct. The ending inventory balance for Year 2 is also correct. However, the ending inventory figure for Year 1 was overstated by $20,000. Given this information, the correct gross profit figures for Year 1 and Year 2 would be:

(Multiple Choice)

4.9/5 (26)

Advances in technology have greatly reduced the cost of a perpetual inventory system. What advantages does a perpetual inventory system have over periodic?

(Essay)

5.0/5 (39)

Incidental costs often added to the costs of inventory include import duties, freight, storage, and insurance.

(True/False)

4.8/5 (39)

Using the information given below, prepare the general journal entry to record the March 16 sale assuming a cash sale and the weighted average method is used.

(Essay)

4.8/5 (36)

A company can change its inventory costing method without mentioning this change in its financial statements because it is an internal management decision.

(True/False)

4.8/5 (31)

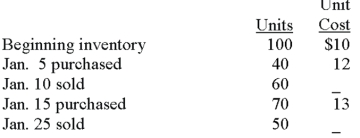

A company sells a climbing kit and uses the perpetual inventory system to account for its merchandise. The beginning balance of the inventory and its transactions during January were as follows: If the ending inventory is reported at $276, what inventory method was used?

(Multiple Choice)

4.7/5 (39)

The retail inventory method estimates the cost of ending inventory by applying the gross profit ratio to net sales.

(True/False)

4.9/5 (36)

Use the following information for Razor Company to compute inventory turnover for 2011.

(Multiple Choice)

4.9/5 (37)

A company has the following per unit original costs and net realizable values for its inventory: Part A: 50 units with a cost of $5, and net realizable value of $4.50

Part B: 75 units with a cost of $6, and net realizable value of $6.50

Part C: 160 units with a cost of $3, and net realizable value of $2.50

Under the lower of cost and net realizable value, the total value of this company's ending inventory is:

(Multiple Choice)

4.9/5 (32)

The ____________________ ratio reflects how much inventory is available in terms of days' sales.

(Essay)

4.8/5 (36)

When applying the lower of cost and net realizable value (NRV) of inventory valuation, NRV is defined as the estimated _____________________ in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale.

(Essay)

4.9/5 (35)

An understatement of the ending inventory balance will understate cost of goods sold and overstate net income.

(True/False)

4.9/5 (35)

Using the information given below for a company that uses a perpetual inventory system, calculate the ending inventory using weighted average.

(Essay)

4.8/5 (38)

Goods on consignment are goods shipped by their owner, called the consignee, to another party called the consignor.

(True/False)

4.9/5 (40)

The costs of goods purchased will vary under the different inventory methods of specific identification, FIFO, LIFO, and weighted average.

(True/False)

4.9/5 (29)

Management decisions in accounting for inventory cost include all of the following except:

(Multiple Choice)

5.0/5 (32)

The consistency concept prescribes that a company use the same accounting methods period after period, so that financial statements are comparable across periods.

(True/False)

4.9/5 (29)

On December 31 of the current year, Hewett Company reported an ending inventory balance of $215,000. The following additional information is also available: Hewett sold goods costing $38,000 to Trump Enterprises on December 28 and shipped the goods on that date with shipping terms of FOB shipping point. The goods were not included in the ending inventory amount of $215,000 because they were not in Hewett's warehouse.

Hewett purchased goods costing $44,000 on December 29. The goods were shipped FOB destination and were received by Hewett on January 2 of the following year. The shipment was a rush order that was supposed to arrive by December 31. These goods were included in the ending inventory balance of $215,000.

Hewett's ending inventory balance of $215,000 included $15,000 of goods being held on consignment from Rumsfeld Company. (Hewett Company is the consignee.)

Hewett's ending inventory balance of $215,000 did not include goods costing $95,000 that were shipped to Hewett on December 27 with shipping terms of FOB destination and were still in transit at year-end.

Based on the above information, the correct balance for ending inventory on December 31 is:

(Multiple Choice)

4.9/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)