Exam 18: Time Series and Forecasting

Exam 1: Statistics and Data100 Questions

Exam 2: Tabular and Graphical Methods123 Questions

Exam 3: Numerical Descriptive Measures151 Questions

Exam 4: Basic Probability Concepts116 Questions

Exam 5: Discrete Probability Distributions139 Questions

Exam 6: Continuous Probability Distributions128 Questions

Exam 7: Sampling and Sampling Distributions124 Questions

Exam 8: Interval Estimation123 Questions

Exam 9: Hypothesis Testing135 Questions

Exam 10: Statistical Inference Concerning Two Populations124 Questions

Exam 11: Statistical Inference Concerning Variance111 Questions

Exam 12: Chi-Square Tests120 Questions

Exam 13: Analysis of Variance58 Questions

Exam 14: Regression Analysis140 Questions

Exam 15: Inference With Regression Models124 Questions

Exam 16: Regression Models for Nonlinear Relationships115 Questions

Exam 17: Regression Models With Dummy Variables114 Questions

Exam 18: Time Series and Forecasting124 Questions

Exam 19: Returns, Index Numbers and Inflation120 Questions

Exam 20: Nonparametric Tests108 Questions

Select questions type

Under which of the following conditions is qualitative forecasting considered attractive?

(Multiple Choice)

4.8/5  (38)

(38)

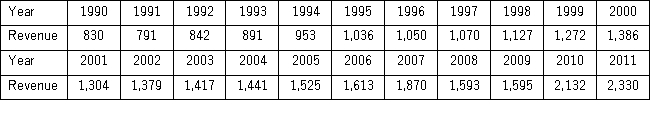

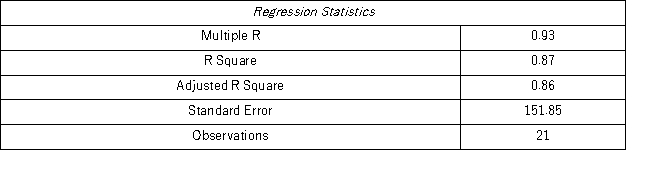

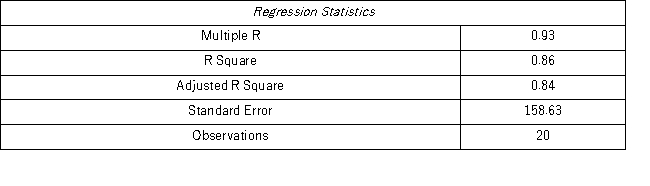

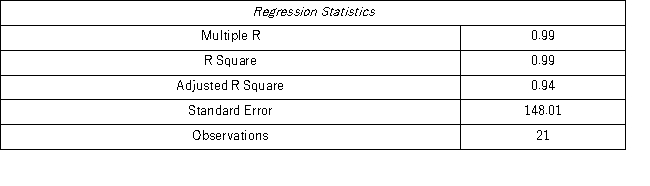

The following table shows the annual revenues (in millions of dollars)of a pharmaceutical company over the period 1990-2011.  The autoregressive models of order 1 and 2,yt = β0 + β1yt - 1 + εt,and yt = β0 + β1yt - 1 + β2yt - 2 + εt,were applied on the time series to make revenue forecasts.The relevant parts of Excel regression outputs are given below.

Model AR(1):

The autoregressive models of order 1 and 2,yt = β0 + β1yt - 1 + εt,and yt = β0 + β1yt - 1 + β2yt - 2 + εt,were applied on the time series to make revenue forecasts.The relevant parts of Excel regression outputs are given below.

Model AR(1):

Model AR(2):

Model AR(2):

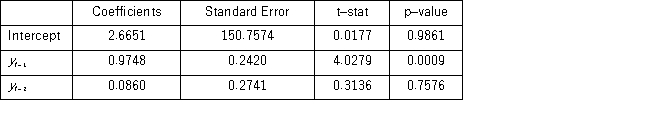

When for AR(1),H0: β0 = 0 is tested against HA: β0 ≠ 0,the p-value of this t test shown by Excel output is 0.9590.This could suggest that the model yt = β1yt-1 + εt might be an alternative to the AR(1)model yt = β0 + β1yt-1 + εt.Excel partial output for this simplified model is as follows:

When for AR(1),H0: β0 = 0 is tested against HA: β0 ≠ 0,the p-value of this t test shown by Excel output is 0.9590.This could suggest that the model yt = β1yt-1 + εt might be an alternative to the AR(1)model yt = β0 + β1yt-1 + εt.Excel partial output for this simplified model is as follows:

Find the revenue forecast for 2012 through the use of yt = β1yt-1 + εt.

Find the revenue forecast for 2012 through the use of yt = β1yt-1 + εt.

(Essay)

4.9/5 (36)

When the decomposition model,yt = Tt × St × It,is applied,forecasts are made as  ,where

,where  represents the estimated trend for seasonally adjusted time series for period t,and

represents the estimated trend for seasonally adjusted time series for period t,and  is the seasonal index for period t.

is the seasonal index for period t.

(True/False)

4.7/5 (40)

When comparing which of the following trend models is the adjusted R2 not used?

(Multiple Choice)

5.0/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)