Exam 7: Allocating Costs of Support Departments and Joint Products

Exam 1: Introduction to Cost Management151 Questions

Exam 2: Basic Cost Management Concepts199 Questions

Exam 3: Cost Behavior193 Questions

Exam 4: Activity-Based Costing198 Questions

Exam 5: Product and Service Costing: Job-Order System149 Questions

Exam 6: Process Costing181 Questions

Exam 7: Allocating Costs of Support Departments and Joint Products171 Questions

Exam 8: Budgeting for Planning and Control202 Questions

Exam 9: Standard Costing: a Functional-Based Control Approach125 Questions

Exam 10: Decentralization: Responsibility, Accounting, Performance Evaluation, and Transfer Pricing134 Questions

Exam 11: Strategic Cost Management148 Questions

Exam 12: Activity-Based Management146 Questions

Exam 13: The Balanced Scorecard: Strategic-Based Control124 Questions

Exam 14: Quality and Environmental Cost Management199 Questions

Exam 15: Lean Accounting and Productivity Measurement161 Questions

Exam 16: Cost-Volume-Profit Analysis128 Questions

Exam 17: Activity Resource Usage Model and Tactical Decision Making121 Questions

Exam 18: Pricing and Profitability Analysis159 Questions

Exam 19: Capital Investment125 Questions

Exam 20: Inventory Management: Economic Order Quantity, Jit, and the Theory of Constraints127 Questions

Select questions type

Mainstream Corporation manufactures two products, I and II, from a joint process. A production run costs $20,000 and results in 500 units of I and 2,000 units of II.

Both products must be processed past the split-off point, incurring separable costs of $5 per unit for I and $10 per unit for II. The market price is $25 for I and $20 for II.

Required:

a. Allocate joint production costs to each product using the physical units method.

b. Allocate joint production costs to each product using the net realizable value method.

c. Allocate joint production costs to each product using the constant gross margin percentage method.

(Essay)

4.8/5  (33)

(33)

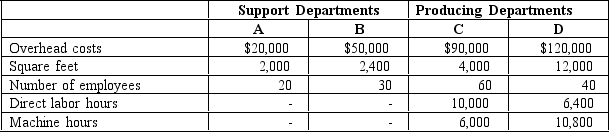

Santiago Manufacturing prices its products at full cost plus 40 percent. The company operates two support departments and two producing departments. Budgeted costs and normal activity levels are as follows:  Support Department A's costs are allocated based on square feet, and Support Department B's costs are allocated based on number of employees. Department C uses direct labor hours to assign overhead costs to products, while Department D uses machine hours.

One of the products the company produces requires 4 direct labor hours per unit in Department C and no time in Department D. Direct materials for the product cost $45 per unit, and direct labor is $20 per unit.

If the direct method of allocation is used and the company follows its usual pricing policy, the selling price of the product would be

Support Department A's costs are allocated based on square feet, and Support Department B's costs are allocated based on number of employees. Department C uses direct labor hours to assign overhead costs to products, while Department D uses machine hours.

One of the products the company produces requires 4 direct labor hours per unit in Department C and no time in Department D. Direct materials for the product cost $45 per unit, and direct labor is $20 per unit.

If the direct method of allocation is used and the company follows its usual pricing policy, the selling price of the product would be

(Multiple Choice)

4.9/5 (30)

The activities or variables within a producing department that provoke the incurrence of support costs are called:

(Multiple Choice)

4.9/5 (42)

Tec-Pro Company has two support departments (S1 and S2) and two producing departments (P1 and P2). Department S1 costs are allocated on the basis of number of employees, and Department S2 costs are allocated on the basis of space occupied expressed in square feet.

Data on direct department costs, number of employees, and space occupied are as follows:

When Tec-Pro uses the sequential method, the support department allocated first is the one with the highest percentage of interdepartmental service. The choice of the department allocated first is determined by the comparison of the following ratio for S1 and S2, respectively:

When Tec-Pro uses the sequential method, the support department allocated first is the one with the highest percentage of interdepartmental service. The choice of the department allocated first is determined by the comparison of the following ratio for S1 and S2, respectively:

(Multiple Choice)

4.8/5 (34)

Vladimir, Inc. began the current period with no inventories. During the period, it processed 50,000 pounds of materials costing $450,000. Conversion costs incurred during the period amounted to $660,000. The firm ended the period with no work-in-process. During the period, the firm produced 16,000, 24,000, and 10,000 units of X, Y, and Z, respectively. All costs are considered joint costs. The firm sold 12,000 units of X, 16,000 units of Y, and 9,000 units of Z. X sells for $30 per unit, Y for $44 per unit, and Z for $4 per unit. The firm uses the net realizable value method for cost allocation. Z is considered a by-product.

Required:

a. Discuss the following methods to account for by-products:

• other income

• replacement cost

• joint cost proration

b. Give three examples of by-products.

(Essay)

4.8/5 (43)

Which joint cost allocation method is described by the following statement? Overall sales revenue minus overall costs (joint plus further processing costs) is calculated to yield gross profit and the gross profit percentage. Each product is then assigned the same cost of goods sold percentage.

(Multiple Choice)

4.8/5 (28)

Joint production processes result in the output of two or more products produced simultaneously.

(True/False)

4.7/5 (41)

Restaurant Products produces two products, X and Y, in a single process. In 2011, the joint costs of this process were $25,000. In addition, 4,000 units of X and 6,000 units of Y were produced. Separable processing costs beyond the split-off point were X - $10,000; Y - $20,000. X sells for $10.00 per unit; Y sells for $7.50 per unit. What amount of joint costs will be allocated to Product X using the physical units method?

(Multiple Choice)

4.8/5 (39)

Arctic Tundra Company has two support departments (S1 and S2) and two producing departments (P1 and P2).

Estimated direct costs and percentages of services used by these departments are as follows:

a. Prepare a schedule allocating the support department costs to the producing departments using the direct allocation method.

b. Prepare a schedule allocating the support department costs to the producing departments using the sequential allocation method.

a. Prepare a schedule allocating the support department costs to the producing departments using the direct allocation method.

b. Prepare a schedule allocating the support department costs to the producing departments using the sequential allocation method.

(Essay)

4.9/5 (40)

Products produced simultaneously by the same process up to a point are called products.

(Short Answer)

4.7/5 (39)

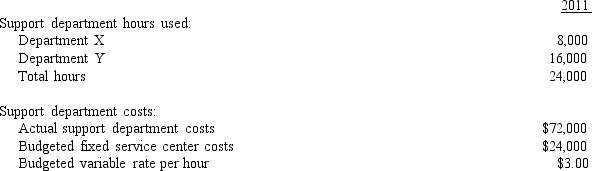

Andover,, Inc., has two producing departments. Each producing department is held responsible for a share of the costs of a support department. Actual and budgeted data are as follows:

Support department hours used:

Support department costs:

Support department costs:

Normal support department usage is 8,000 hours each for Department L and Department M. Assuming the direct method is used and the purpose is product costing, support department costs allocated to Department L are

Normal support department usage is 8,000 hours each for Department L and Department M. Assuming the direct method is used and the purpose is product costing, support department costs allocated to Department L are

(Multiple Choice)

4.9/5 (49)

Alliance Manufacturing Company has two support departments, Maintenance Department and Personnel Department, and two producing departments, X and Y. The Maintenance Department costs of $90,000 are allocated on the basis of standard service hours used. The Personnel Department costs of $13,500 are allocated on the basis of number of employees. The direct costs of Departments X and Y are $27,000 and $45,000, respectively.

Data on standard service hours and number of employees are as follows:

Predetermined overhead rates for Departments X and Y, respectively, are based on direct labor hours.

What is the overhead rate for Department Y assuming the direct method is used?

a. $90.00

b. $163.50

c. $187.50

d. $81.75

Predetermined overhead rates for Departments X and Y, respectively, are based on direct labor hours.

What is the overhead rate for Department Y assuming the direct method is used?

a. $90.00

b. $163.50

c. $187.50

d. $81.75

(Essay)

4.8/5 (43)

Figure 7-7

Garden of Eden Company manufactures two products, Brights and Dulls, from a joint process. A production run costs $50,000 and results in 250 units of Brights and 1,000 units of Dulls. Both products must be processed past the split-off point, incurring separable costs for Brights of $60 per unit and $40 per unit for Dulls. The market price is

$250 for Brights and $200 for Dulls.

-Refer to Figure 7-7. What is the gross profit for Brights assuming the net realizable value method is used?

(Multiple Choice)

4.7/5 (36)

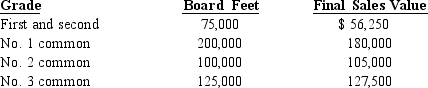

Carson Wood Products processes logs into four grades of lumber totaling 500,000 board feet as follows at a joint cost of $300,000:  What amount of joint costs will be allocated to No. 2 common using the constant gross margin percentage method?

What amount of joint costs will be allocated to No. 2 common using the constant gross margin percentage method?

(Multiple Choice)

4.9/5 (48)

Carson Wood Products processes logs into four grades of lumber totaling 500,000 board feet as follows at a joint cost of $300,000:  What is the gross profit of No. 3 common if the constant gross margin percentage method is used?

What is the gross profit of No. 3 common if the constant gross margin percentage method is used?

(Multiple Choice)

4.7/5 (45)

Compare and contrast the various methods of accounting for joint product costs.

(Essay)

4.8/5 (35)

Albemarle, Inc., has two producing departments. Each producing department is held responsible for a share of the costs of a support department.

Actual and budgeted data are as follows:

Normal support department usage is 12,000 hours each for Department X and Department Y.

Required:

a. Assuming the purpose is product costing, allocate the costs of the support department using the direct method.

b. Assuming the purpose is to evaluate performance, allocate the costs of the support department.

Normal support department usage is 12,000 hours each for Department X and Department Y.

Required:

a. Assuming the purpose is product costing, allocate the costs of the support department using the direct method.

b. Assuming the purpose is to evaluate performance, allocate the costs of the support department.

(Essay)

4.9/5 (30)

Consequence Printing operates a Graphics business at two different locations. Consequence Printing has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each Graphics Center on the basis of total prints made.

During the first month, the costs of the support department were expected to be $100,000. Of this amount, $30,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $64,000 and actual fixed costs of $36,000.

Normal and actual activity (prints made) are as follows:

a. For purposes of performance evaluation, calculate the fixed costs allocated to Graphics Center 1.

b. For purposes of performance evaluation, calculate the fixed costs allocated to Graphics Center 2.

c. Calculate the support department costs not allocated to the two Graphics Centers.

a. For purposes of performance evaluation, calculate the fixed costs allocated to Graphics Center 1.

b. For purposes of performance evaluation, calculate the fixed costs allocated to Graphics Center 2.

c. Calculate the support department costs not allocated to the two Graphics Centers.

(Essay)

4.7/5 (33)

Causal factors are variables or activities within a producing department that stimulate the incurrence of support costs.

(True/False)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)