Exam 7: Allocating Costs of Support Departments and Joint Products

Exam 1: Introduction to Cost Management151 Questions

Exam 2: Basic Cost Management Concepts199 Questions

Exam 3: Cost Behavior193 Questions

Exam 4: Activity-Based Costing198 Questions

Exam 5: Product and Service Costing: Job-Order System149 Questions

Exam 6: Process Costing181 Questions

Exam 7: Allocating Costs of Support Departments and Joint Products171 Questions

Exam 8: Budgeting for Planning and Control202 Questions

Exam 9: Standard Costing: a Functional-Based Control Approach125 Questions

Exam 10: Decentralization: Responsibility, Accounting, Performance Evaluation, and Transfer Pricing134 Questions

Exam 11: Strategic Cost Management148 Questions

Exam 12: Activity-Based Management146 Questions

Exam 13: The Balanced Scorecard: Strategic-Based Control124 Questions

Exam 14: Quality and Environmental Cost Management199 Questions

Exam 15: Lean Accounting and Productivity Measurement161 Questions

Exam 16: Cost-Volume-Profit Analysis128 Questions

Exam 17: Activity Resource Usage Model and Tactical Decision Making121 Questions

Exam 18: Pricing and Profitability Analysis159 Questions

Exam 19: Capital Investment125 Questions

Exam 20: Inventory Management: Economic Order Quantity, Jit, and the Theory of Constraints127 Questions

Select questions type

FIGURE 7-5

Stronghold, Inc., operates a brochure business at two different locations. Stronghold, Inc., has one support department that is responsible for cleaning, service, and maintenance of its printing equipment. The costs of the support department are allocated to each brochure center on the basis of total brochures made.

During the first month, the costs of the support department were expected to be $400,000. Of this amount, $120,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $256,000 and actual fixed costs of $144,000.

Normal and actual activity (brochures made) are as follows:

-Refer to Figure 7-5. Support department costs NOT allocated to the two brochure centers are

-Refer to Figure 7-5. Support department costs NOT allocated to the two brochure centers are

(Multiple Choice)

4.8/5  (33)

(33)

Figure 7-6

Golden Leaves Company has two support departments, Maintenance Department (MD) and Personnel Department (PD), and two producing departments, P1 and P2. The Maintenance Department costs of $30,000 are allocated on the basis of standard service used. The Personnel Department costs of $4,500 are allocated on the basis of number of employees. The direct costs of Departments P1 and P2 are $9,000 and $15,000, respectively.

Data on standard service hours and number of employees are as follows:

-Refer to Figure 7-6. What is the combined total department costs for the producing departments after allocation of the support departments?

-Refer to Figure 7-6. What is the combined total department costs for the producing departments after allocation of the support departments?

(Multiple Choice)

4.9/5 (28)

The choice of allocation method depends on an evaluation of costs and benefits, and circumstances.

(True/False)

4.7/5 (38)

After allocation, total overhead in producing department is divided by the budgeted measure of activity to get the

__________ overhead rate.

(Short Answer)

4.8/5 (36)

Figure 7-6

Golden Leaves Company has two support departments, Maintenance Department (MD) and Personnel Department (PD), and two producing departments, P1 and P2. The Maintenance Department costs of $30,000 are allocated on the basis of standard service used. The Personnel Department costs of $4,500 are allocated on the basis of number of employees. The direct costs of Departments P1 and P2 are $9,000 and $15,000, respectively.

Data on standard service hours and number of employees are as follows:

-Refer to Figure 7-6. Using the sequential method, if the support department with the highest percentage of interdepartmental service is allocated first, the cost of the Maintenance Department allocated to Department P1 is

(Multiple Choice)

4.7/5 (46)

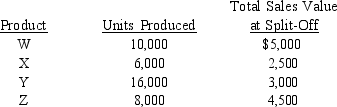

Laredo Corporation, which manufactures products W, X, Y, and Z through a joint process costing $24,000, has the following data for 2016:  What is the amount of joint costs assigned to product W using the physical units method?

What is the amount of joint costs assigned to product W using the physical units method?

(Multiple Choice)

4.9/5 (33)

A company incurred $80,000 of common fixed costs and $120,000 of common variable costs. These costs are to be allocated to Departments A and B. Data on capacity provided and capacity used are as follows: Capacity Provided Capacity Used

Department in Hours in Hours

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

Assume that both fixed and variable costs are allocated on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

(Multiple Choice)

4.8/5 (39)

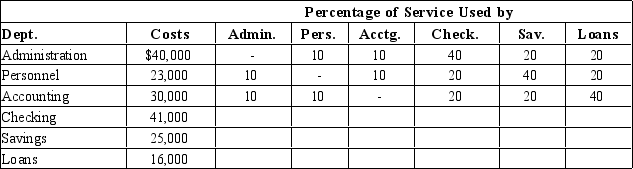

The Savings Bank of Sarasota has three revenue-generating departments: checking accounts, savings accounts, and loans. The bank also has three service areas: administration, personnel, and accounting. The direct costs per month and the interdepartmental service structure are shown below:  The Savings Bank of Sarasota uses the sequential (step) method and the service departments are allocated in the following order: administration, personnel, and accounting. How much cost would be allocated to the loan area from the personnel department using the sequential/step method? (Round to two decimal places.)

The Savings Bank of Sarasota uses the sequential (step) method and the service departments are allocated in the following order: administration, personnel, and accounting. How much cost would be allocated to the loan area from the personnel department using the sequential/step method? (Round to two decimal places.)

(Multiple Choice)

4.8/5 (38)

Fixed support department costs should be allocated based on

(Multiple Choice)

4.9/5 (38)

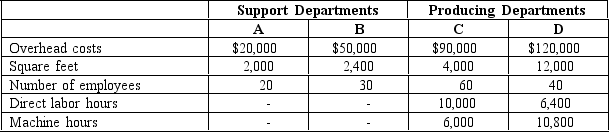

Rodriguez Manufacturing prices its products at full cost plus 40 percent. The company operates two support departments and two producing departments. Budgeted costs and normal activity levels are as follows:  Support Department A's costs are allocated based on square feet, and Support Department B's costs are allocated based on number of employees. Department C uses direct labor hours to assign overhead costs to products, while Department D uses machine hours.

One of the products the company produces requires 4 direct labor hours per unit in Department C and no time in Department D. Direct materials for the product cost $45 per unit, and direct labor is $20 per unit.

If the sequential method of allocation is used and the company follows its usual pricing policy, the selling price of the product would be (round service allocations to the nearest whole dollar and the costs per unit to two decimal places)

Support Department A's costs are allocated based on square feet, and Support Department B's costs are allocated based on number of employees. Department C uses direct labor hours to assign overhead costs to products, while Department D uses machine hours.

One of the products the company produces requires 4 direct labor hours per unit in Department C and no time in Department D. Direct materials for the product cost $45 per unit, and direct labor is $20 per unit.

If the sequential method of allocation is used and the company follows its usual pricing policy, the selling price of the product would be (round service allocations to the nearest whole dollar and the costs per unit to two decimal places)

(Multiple Choice)

4.9/5 (39)

A company incurred $120,000 of common fixed costs and $180,000 of common variable costs. These costs are to be allocated to Departments XX and YY. Data on capacity provided and capacity used are as follows:  Assume that common fixed costs are to be allocated to Departments XX and YY on the basis of capacity provided

And that common variable costs are to be allocated to Departments XX and YY on the basis of capacity used. The fixed and variable costs allocated to Department XX are

Fixed Variable

Assume that common fixed costs are to be allocated to Departments XX and YY on the basis of capacity provided

And that common variable costs are to be allocated to Departments XX and YY on the basis of capacity used. The fixed and variable costs allocated to Department XX are

Fixed Variable

(Multiple Choice)

4.8/5 (36)

A company incurred $40,000 of common fixed costs and $60,000 of common variable costs. These costs are to be allocated to Departments A and B. Data on capacity provided and capacity used are as follows: Capacity Provided Capacity Used

Department in Hours in Hours

Assume that common fixed costs are to be allocated to Departments A and B on the basis of capacity provided and that common variable costs are to be allocated to Departments A and B on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

Assume that common fixed costs are to be allocated to Departments A and B on the basis of capacity provided and that common variable costs are to be allocated to Departments A and B on the basis of capacity used. The fixed and variable costs allocated to Department A are

Fixed Variable

(Not Answered)

This question doesn't have any answer yet

Activities or variables within a producing department that provoke the incurrence of support costs are called

__________ .

(Short Answer)

4.7/5 (34)

FIGURE 7-4

Copies Plus Print operates a copy business at two different locations. Copies Plus Print has one support department that is responsible for cleaning, service, and maintenance of its copying equipment. The costs of the support department are allocated to each copy center on the basis of total copies made.

During the first month, the costs of the support department were expected to be $200,000. Of this amount, $60,000 is considered a fixed cost. During the month, the support department incurred actual variable costs of $128,000 and actual fixed costs of $72,000.

Normal and actual activity (copies made) are as follows:

-Refer to Figure 7-4. Support department costs NOT allocated to the two copy centers are

-Refer to Figure 7-4. Support department costs NOT allocated to the two copy centers are

(Multiple Choice)

4.8/5 (27)

Support department fixed costs are allocated on the basis of original capacity.

(True/False)

4.8/5 (39)

The charging rate combines variable and fixed costs of support departments.

(Short Answer)

5.0/5 (38)

What is one of the potential disadvantages of NOT allocating support department costs to production departments?

(Multiple Choice)

4.9/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)