Exam 14: Introduction to Time Series Regression and Forecasting

Exam 1: Economic Questions and Data11 Questions

Exam 2: Review of Probability61 Questions

Exam 3: Review of Statistics56 Questions

Exam 4: Linear Regression With One Regressor54 Questions

Exam 5: Regression With a Single Regressor: Hypothesis Tests and Confidence Intervals53 Questions

Exam 6: Linear Regression With Multiple Regressors54 Questions

Exam 7: Hypothesis Tests and Confidence Intervals in Multiple Regression50 Questions

Exam 8: Nonlinear Regression Functions53 Questions

Exam 9: Assessing Studies Based on Multiple Regression55 Questions

Exam 10: Regression With Panel Data40 Questions

Exam 11: Regression With a Binary Dependent Variable40 Questions

Exam 12: Instrumental Variables Regression40 Questions

Exam 13: Experiments and Quasi-Experiments40 Questions

Exam 14: Introduction to Time Series Regression and Forecasting36 Questions

Exam 15: Estimation of Dynamic Causal Effects40 Questions

Exam 16: Additional Topics in Time Series Regression40 Questions

Exam 17: The Theory of Linear Regression With One Regressor39 Questions

Exam 18: The Theory of Multiple Regression38 Questions

Select questions type

The Granger Causality Test c. uses the -statistic to test the hypothesis that certain regressors have no predictive content for the dependent variable beyond that contained in the other regressors.

d. establishes the direction of causality (as used in common parlance) between and in addition to correlation.

e. is a rather complicated test for statistical independence.

f. is a special case of the Augmented Dickey-Fuller test.

(Short Answer)

4.7/5  (48)

(48)

You should use the QLR test for breaks in the regression coefficients, when

(Multiple Choice)

4.8/5 (35)

The Times Series Regression with Multiple Predictors a. is the same as the with additional predictors and their lags present.

b. gives you more than one prediction.

c. cannot be estimated by OLS due to the presence of multiple lags.

d. requires that the regressors and the dependent variable have nonzero, finite eighth moments.

(Short Answer)

4.9/5 (37)

You want to determine whether or not the unemployment rate for the United States has a

stochastic trend using the Augmented Dickey Fuller Test (ADF).The BIC suggests using

3 lags, while the AIC suggests 4 lags.

(a)Which of the two will you use for your choice of the optimal lag length?

(Essay)

4.9/5 (40)

One of the sources of error in the RMSFE in the AR(1) model is

(Multiple Choice)

4.8/5 (37)

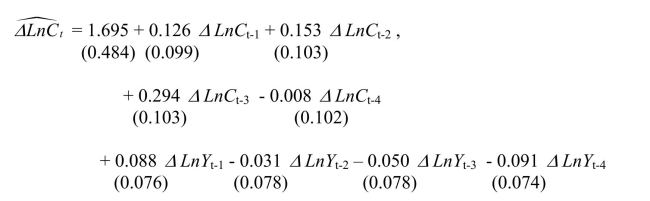

Having learned in macroeconomics that consumption depends on disposable income, you

want to determine whether or not disposable income helps predict future consumption.

You collect data for the sample period 1962:I to 1995:IV and plot the two variables.

(a)To determine whether or not past values of personal disposable income growth rates help

to predict consumption growth rates, you estimate the following relationship.  The Granger causality test for the exclusion on all four lags of the GDP growth rate is

0.98.Find the critical value for the 1%, the 5%, and the 10% level from the relevant table

and make a decision on whether or not these additional variables Granger cause the

change in the growth rate of consumption.

The Granger causality test for the exclusion on all four lags of the GDP growth rate is

0.98.Find the critical value for the 1%, the 5%, and the 10% level from the relevant table

and make a decision on whether or not these additional variables Granger cause the

change in the growth rate of consumption.

(Essay)

4.7/5 (41)

If a "break" occurs in the population regression function, then

(Multiple Choice)

4.9/5 (30)

In order to make reliable forecasts with time series data, all of the following conditions are needed with the exception of

(Multiple Choice)

4.9/5 (33)

One reason for computing the logarithms (ln), or changes in logarithms, of economic time series is that

(Multiple Choice)

4.9/5 (42)

The root mean squared forecast error (RMSFE)is defined as a. .

b. .

c. .

d. .

(Short Answer)

4.8/5 (29)

Negative autocorrelation in the change of a variable implies that

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)