Exam 16: Translating Foreign Currency Statements: The Temporal Method and the Functional Currency Concept

Exam 1: Wholly Owned Subsidiaries: at Date of Creation87 Questions

Exam 2: Wholly Owned Subsidiaries: Postcreation Periods110 Questions

Exam 3: Partially Owned Created Subsidiaries & Variable Interest Entities138 Questions

Exam 4: Introduction to Business Combinations105 Questions

Exam 5: The Purchase Method: at Date of Acquisition-100 Ownership135 Questions

Exam 6: The Purchase Method: Postacquisition Periods and Partial Ownerships74 Questions

Exam 7: New Basis of Accounting52 Questions

Exam 8: Introduction to Intercompany Transactions42 Questions

Exam 9: Intercompany Inventory Transfers66 Questions

Exam 10: Intercompany Fixed Asset Transfers & Bond Holdings31 Questions

Exam 11: Changes in a Parents Ownership Interest, Statement of Cash Flows, & Earnings Per Share86 Questions

Exam 12: Reporting Segment and Related Information90 Questions

Exam 13: International Accounting Standards & Translating Foreign Currency Transactions103 Questions

Exam 14: Using Derivatives to Manage Foreign Currency Exposures256 Questions

Exam 15: Translating Foreign Currency Statements: The Current Rate Method99 Questions

Exam 16: Translating Foreign Currency Statements: The Temporal Method and the Functional Currency Concept231 Questions

Exam 17: Interim Period Reporting49 Questions

Exam 18: Securities and Exchange Commission Reporting55 Questions

Exam 19: Bankruptcy Reorganizations and Liquidations51 Questions

Exam 20: Partnerships: Formation and Operation45 Questions

Exam 21: Partnerships: Changes in Ownership37 Questions

Exam 22: Partnerships: Liquidations35 Questions

Exam 23: Estates and Trusts40 Questions

Exam 24: Governmental Accounting: Basic Principles and the General Fund138 Questions

Exam 25: Governmental Accounting: The Special-Purpose Funds and Special General Ledger232 Questions

Exam 26: Not-For-Profit Organizations: Introduction and Private Npos218 Questions

Select questions type

A decrease in the direct exchange rate as a result of foreign inflation results in an unrealized inflationary holding gain to the extent that foreign fixed assets are financed with nonindexed debt.

(True/False)

4.9/5  (28)

(28)

The functional currency concept is based on whether decision making at the foreign unit has been decentralized.

(True/False)

4.8/5 (34)

The risk of investing in foreign countries can be virtually eliminated by having the foreign units invest their assets in nonmonetary assets.

(True/False)

4.8/5 (36)

Under FAS 52, the effect of an exchange rate change is always reported currently in earnings if the foreign currency is the functional currency.

(True/False)

4.8/5 (32)

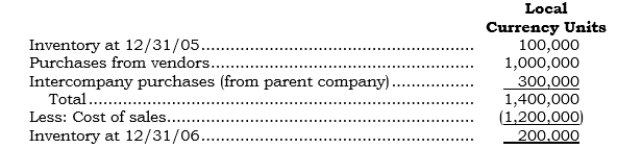

A foreign subsidiary has provided the following information with respect to its year-end inventories and cost of sales for 2006:

Additional information:

a. The subsidiary's sales occurred evenly throughout the year.

b. The average exchange rate during the year was 1 LCU = $.40.

c. Purchases from vendors occurred during the first nine months, when the average rate was 1 LCU = $.42.

d. The intercompany purchases from the parent all occurred in the last three months, when the average exchange rate was 1 LCU = $.33. (The parent recorded these intercompany sales in its general ledger at $96,000.)

e. The current rate at 12/31/06 was 1 LCU = $.30.

f. The beginning inventory was reported at $50,000 in the 12/31/05 balance sheet (as expressed in U.S. dollars).

g. Assume that no lower-of-cost-or-market test in U.S. dollars need be performed at 12/31/06.

h.

Additional information:

a. The subsidiary's sales occurred evenly throughout the year.

b. The average exchange rate during the year was 1 LCU = $.40.

c. Purchases from vendors occurred during the first nine months, when the average rate was 1 LCU = $.42.

d. The intercompany purchases from the parent all occurred in the last three months, when the average exchange rate was 1 LCU = $.33. (The parent recorded these intercompany sales in its general ledger at $96,000.)

e. The current rate at 12/31/06 was 1 LCU = $.30.

f. The beginning inventory was reported at $50,000 in the 12/31/05 balance sheet (as expressed in U.S. dollars).

g. Assume that no lower-of-cost-or-market test in U.S. dollars need be performed at 12/31/06.

h.  Required:

a. Assuming that the foreign currency is the functional currency, determine the amounts at which the cost of sales for 2006 and inventory at 12/31/06 would be reported in U.S. dollars.

b. Same as Requirement a, but assume that the U.S. dollar is the functional currency.

Required:

a. Assuming that the foreign currency is the functional currency, determine the amounts at which the cost of sales for 2006 and inventory at 12/31/06 would be reported in U.S. dollars.

b. Same as Requirement a, but assume that the U.S. dollar is the functional currency.

(Essay)

4.8/5 (37)

_____ During 2006, a foreign subsidiary had fixed assets of 100,000 local currency units that were financed with nonindexed local currency debt. Assume that the direct exchange rate decreased by $.07 during 2006, which was the result of foreign inflation. How much would the consolidated stockholders' equity change in U.S. dollars under the current rate method?

(Multiple Choice)

4.8/5 (38)

Under FAS 52, the effect of an exchange rate change is always reported in Other Comprehensive Income if the foreign currency is the functional currency.

(True/False)

4.8/5 (41)

_____ Under FAS 52, how is the effect of an exchange rate change for the current year reported under the temporal method of translation?

(Multiple Choice)

4.9/5 (47)

Under FAS 52, the U.S. dollar is deemed the functional currency for foreign units operating in ________________________________________.

(Short Answer)

4.8/5 (36)

_____ Which of the following items is a factor pointing toward the use of the U.S. dollar as the functional currency?

(Multiple Choice)

4.9/5 (42)

_____ Which of the following statements is true concerning the U.S. income tax rules?

(Multiple Choice)

4.8/5 (27)

The PPP current-value approach results in mixing different valuation bases (for domestic fixed assets and foreign fixed assets).

(True/False)

4.7/5 (38)

A gain in name only is called a(n) ___________________________________ gain.

(Short Answer)

4.9/5 (34)

_____ Unrealized inflationary holding gains resulting from the exchange rate change effect of foreign inflation are reported

(Multiple Choice)

4.9/5 (36)

_____ Paltex's foreign subsidiary reported depreciation expense for 2007 of 250,000 LCUs (100,000 LCUs pertain to equipment acquired in 2007, when the exchange rate was $1 = 8 LCUs, and 150,000 LCUs pertain to equipment acquired in 2007, when the exchange rate was $1 = 6 LCUs). For 2007, the average exchange rate was $1 = 5 LCUs, and the year-end exchange rate was $1 = 4 LCUs. If the LCU is the functional currency, what amount should be reported for depreciation expense in dollars?

(Multiple Choice)

4.9/5 (35)

A domestic company's 100%-owned foreign subsidiary located in Switzerland submitted the following income statement for 2006:

Additional information:

a. Inventory decreased 100,000 francs during 2006.

b. Sales, purchases, and operating expenses occurred or were incurred evenly throughout the year. (Operating expenses include depreciation expense of 100,000 francs.)

c. The subsidiary, whose functional currency is the U.S. dollar, had at the beginning of 2006 monetary assets of 1,000,000 francs, monetary liabilities of 700,000 Swiss francs, and stockholders' equity of 1,500,000 Swiss francs.

d. On 10/19/06, the subsidiary declared and paid a cash dividend of 200,000 Swiss francs.

e. Cash disbursements for 2006 were 2,500,000 francs.

f. Direct exchange rate information follows:

Additional information:

a. Inventory decreased 100,000 francs during 2006.

b. Sales, purchases, and operating expenses occurred or were incurred evenly throughout the year. (Operating expenses include depreciation expense of 100,000 francs.)

c. The subsidiary, whose functional currency is the U.S. dollar, had at the beginning of 2006 monetary assets of 1,000,000 francs, monetary liabilities of 700,000 Swiss francs, and stockholders' equity of 1,500,000 Swiss francs.

d. On 10/19/06, the subsidiary declared and paid a cash dividend of 200,000 Swiss francs.

e. Cash disbursements for 2006 were 2,500,000 francs.

f. Direct exchange rate information follows:

Required:

Calculate the 2006 foreign currency transaction gain or loss arising from the change in the exchange rate.

Required:

Calculate the 2006 foreign currency transaction gain or loss arising from the change in the exchange rate.

(Essay)

4.9/5 (34)

_____ The U.S. dollar is the functional currency of a British subsidiary. During 2006, the British pound strengthened. An unfavorable reporting result occurred as a result of this 2006 exchange rate change. What was the subsidiary's average financial position during 2006?

(Multiple Choice)

4.8/5 (42)

_____ Parrex has a foreign subsidiary, Sarrex. The direct exchange rate decreased from $.70 at 1/1/06 to $.60 at 12/31/06. During 2006, Sarrex had (a) an average net asset position of 400,000 LCUs and (b) an average net monetary liability position of 600,000 LCUs. Under the temporal method, what is the effect of the change in the exchange rate for 2006?

(Multiple Choice)

4.9/5 (39)

Under APB Opinion No. 23, parent-level income taxes are recorded on a foreign subsidiary's earnings regardless of whether the income taxes are expected to eventually be paid.

(True/False)

4.7/5 (34)

_____ Pindax owns 100% of the outstanding common stock of Sindax, a foreign subsidiary located in a country having a 25% income tax rate and a 5% dividend withholding tax. For 2006, Sindax reported net income of $300,000 and paid dividends of $300,000. Pindax's income tax rate is 40%. What amount should Pindax report for deferred income taxes payable in its balance sheet at 12/31/06?

(Multiple Choice)

4.8/5 (30)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)