Exam 36: Translation of the Accounts of Foreign Operations

Exam 1: An Overview of the Australian External Reporting Environment50 Questions

Exam 2: The Conceptual Framework of Accounting and Its Relevance to Financ62 Questions

Exam 3: Theories of Financial Accounting61 Questions

Exam 4: An Overview of Accounting for Assets62 Questions

Exam 5: Depreciation of Property, plant and Equipment62 Questions

Exam 6: Revaluation and Impairment Testing of Non-Current Assets59 Questions

Exam 7: Inventory61 Questions

Exam 8: Accounting for Intangibles61 Questions

Exam 9: Accounting for Heritage Assets and Biological Assets61 Questions

Exam 10: An Overview of Accounting for Liabilities58 Questions

Exam 11: Accounting for Lease78 Questions

Exam 12: Set-Off and Extinguishment of Debt47 Questions

Exam 13: Accounting for Employee Benefits67 Questions

Exam 14: Share Capital and Reserves66 Questions

Exam 15: Accounting for Financial Instruments72 Questions

Exam 16: Revenue Recognition Issues64 Questions

Exam 17: The Statement of Comprehensive Income and Statement of Changes in E62 Questions

Exam 18: Accounting for Share-Based Payments62 Questions

Exam 19: Accounting for Income Taxes56 Questions

Exam 20: Cash-Flow Statements60 Questions

Exam 21: Accounting for the Extractive Industries60 Questions

Exam 22: Accounting for General Insurance Contracts58 Questions

Exam 23: Accounting for Superannuation Plans62 Questions

Exam 24: Events Occurring After Balance Sheet Date62 Questions

Exam 25: Segment Reporting61 Questions

Exam 26: Related-Party Disclosures59 Questions

Exam 27: Earnings Per Share43 Questions

Exam 28: Accounting for Group Structures69 Questions

Exam 29: Further Consolidation Issues I: Accounting for Intragroup Transact46 Questions

Exam 30: Further Consolidation Issues II: Accounting for Minority Interests34 Questions

Exam 31: Further Consolidation Issues III: Accounting for Indirect Ownershi38 Questions

Exam 32: Further Consolidation Issues Iv: Accounting for Changes in the Deg39 Questions

Exam 33: Accounting for Equity Investments67 Questions

Exam 33: Accounting for Equity Investments59 Questions

Exam 35: Accounting for Foreign Currency Transactions58 Questions

Exam 36: Translation of the Accounts of Foreign Operations41 Questions

Exam 37: Accounting for Corporate Social Responsibility59 Questions

Select questions type

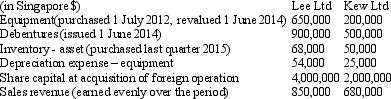

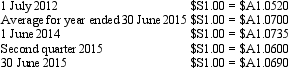

Rudd Ltd,an Australian entity purchased Lee Ltd and Kew Ltd on 1 July 2012.Both entities are considered foreign operations of Rudd Ltd based in Singapore.The following information was extracted from the foreign operation's accounts for the period ended 30 June 2015:  Exchange rate information is:

Exchange rate information is:

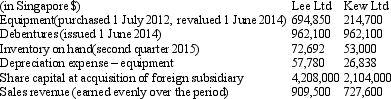

The translation from Singapore dollars to Australian dollars resulted to the following balances:

The translation from Singapore dollars to Australian dollars resulted to the following balances:

Which of the following translation processes were applied to Lee Ltd and Kew Ltd,respectively,for the year ended 30 June 2015?

Which of the following translation processes were applied to Lee Ltd and Kew Ltd,respectively,for the year ended 30 June 2015?

(Multiple Choice)

4.8/5  (40)

(40)

Lennon Ltd has two foreign operations based in Japan.The following information was extracted from the foreign operation's accounts for the period ended 30 June 2015:  Exchange rate information is:

Exchange rate information is:

The translation from Japanese Yen to Australian dollars resulted to the following balances (rounded to the nearest ¥000):

The translation from Japanese Yen to Australian dollars resulted to the following balances (rounded to the nearest ¥000):

Which of the following translation processes were applied to Yoko Ltd and Ono Ltd,respectively,for the year ended 30 June 2015?

Which of the following translation processes were applied to Yoko Ltd and Ono Ltd,respectively,for the year ended 30 June 2015?

(Multiple Choice)

4.9/5 (32)

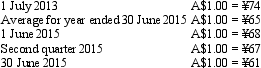

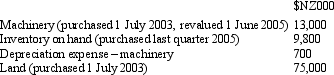

Aus Co Ltd has a foreign operation based in Japan.The following information was extracted from the foreign operation's accounts for the period ended 30 June 2005:  Exchange rate information is:

Exchange rate information is:

What is the amount at which each item would be translated (rounded to the nearest $A)?

What is the amount at which each item would be translated (rounded to the nearest $A)?

(Multiple Choice)

4.9/5 (28)

Exchange differences resulting from the translation of foreign operations to presentation currency are shown:

(Multiple Choice)

4.8/5 (33)

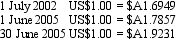

The net assets of a foreign operation at 30 June 2005 are constituted as assets of US$400,000 and liabilities of US$250,000.The parent entity purchased the foreign subsidiary on 1 July 2002.Exchange rate information is as follows:  The foreign operation has not traded during the year ended 30 June 2005,so the net assets remained unchanged during the period.What is the parent entity's foreign currency exposure for the year ended 30 June 2005?

The foreign operation has not traded during the year ended 30 June 2005,so the net assets remained unchanged during the period.What is the parent entity's foreign currency exposure for the year ended 30 June 2005?

(Multiple Choice)

4.8/5 (39)

In translating the accounts of a foreign operation from functional to presentation currency,resulting exchange differences is recognised in other comprehensive income.

(True/False)

4.8/5 (47)

Under the translation method required by AASB 121,the approach to translating a foreign operation's accounts includes:

(Multiple Choice)

4.8/5 (34)

The exchange rate used for the translation of the payment of dividends is the spot rate at the date when the retained earnings or reserves,from which the dividends were drawn,were createD.

(True/False)

5.0/5 (29)

In the process of consolidating the translated financial accounts of a foreign operation,the calculation of minority interests will be affected by the translation process in what way?

(Multiple Choice)

4.8/5 (33)

The translation approach required by AASB 121 in translating to presentation currency is similar to the "current rate" method required under the former AASB 1012:

(True/False)

4.7/5 (40)

The amount of a foreign operation's post-acquisition retained earnings as translated into Australian dollars will depend on the amount translated from the income statement:

(True/False)

4.9/5 (35)

AASB 121 requires foreign currency transactions to be recorded on initial recognition in the functional currency,by applying to the foreign currency amount the spot exchange rate between the functional currency and the foreign currency at the reporting date.

(True/False)

4.9/5 (29)

If the assets of a foreign operation exceed its liabilities,and the value of the Australian dollar falls relative to the currency of the foreign operations,there will be:

(Multiple Choice)

4.7/5 (26)

As prescribed in AASB 121,translation of the accounts of foreign operations to the presentation currency requires any gains or losses on translation be taken directly to reserves:

(True/False)

4.8/5 (32)

Under the former AASB 1012 there were two methods of translation of the accounts of foreign operations; the method being used being dependent upon the whether these operations are integrated or self-sustaining:

(True/False)

4.9/5 (33)

If the exchange rate for US dollars relative to Australian dollars goes from US$1 = $A2.10 to US$1 = $A2.20,the Australian dollar has strengthened.

(True/False)

4.9/5 (41)

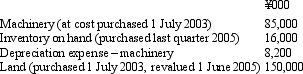

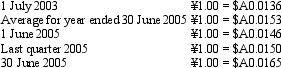

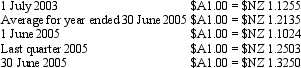

Aus Co Ltd has a foreign operation based in New Zealand.The following information was extracted from the foreign operation's accounts for the period ended 30 June 2005:  Exchange rate information is:

Exchange rate information is:

What is the amount at which each item will be translated (rounded to the nearest $A)?

What is the amount at which each item will be translated (rounded to the nearest $A)?

(Multiple Choice)

4.8/5 (29)

As prescribed in AASB 121,in translating the accounts of a foreign operation from local currency to functional currency,the exchange rate to use for land is the exchange rate at the date of the transaction.

(True/False)

4.9/5 (35)

The foreign exchange exposure of the parent entity in relation to its foreign operation relates to the net cash flows of the investment in the operation:

(True/False)

4.8/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)