Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

Article Summary

As a part of its 2013 marketing campaign, the Greater Fort Lauderdale Convention & Visitors Bureau (CVB) set its sights on increasing travel to the region by with promotions to the lesbian, gay, bisexual and transgender community (LGBT). From August through November, the CVB has events scheduled across the United States and globally in an effort to attract a larger share of this travel segment. According to the CVB, Fort Lauderdale is the state's largest and most popular diverse gay capital, and their marketing efforts helped attract 1.2 million LGBT tourists who spent $1.4 billion in 2012.

Source: Arlene Satchell, "Lauderdale CVB ramps up LGBT summer marketing," Sun Sentinel, June 29, 2013.

-Refer to the Article Summary. By marketing to the LGBT community, Fort Lauderdale and the CVB are trying to set the city apart from competing travel destinations. This is an example of

(Multiple Choice)

4.9/5  (39)

(39)

Juicy Couture has been successful in selling women's clothing using an unusual strategy. According to an article in the Wall Street Journal, the key to the firm's strategy is to "limit distribution to maintain the brand's exclusive cachet, even if that means sacrificing sales, a brand-management technique once used only for high-end luxury brands." In 2006, Juicy clothes were sold in only four department stores: Neiman Marcus, Saks, Bloomingdale's, and Nordstrom. In 2006, its sales have more than quadrupled since 2002.

Source: Rachel Dodes, "From Track Suits to Fast Track," Wall Street Journal, September 13, 2006.

How does limiting the number of stores in which Juicy's products are sold contribute to its success?

(Multiple Choice)

4.9/5 (33)

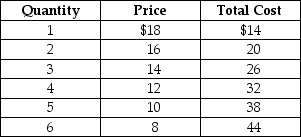

Table 13-1

-Refer to Table 13-1. What portion of the marginal revenue of the 5th unit is due to the output effect and what portion is due to the price effect?

-Refer to Table 13-1. What portion of the marginal revenue of the 5th unit is due to the output effect and what portion is due to the price effect?

(Multiple Choice)

4.9/5 (36)

Starbucks started out small in 1971, but by 1993 Starbucks was a national chain and had coffeehouses in 38 countries. A key to the company's success was the realization by executives that

(Multiple Choice)

4.7/5 (32)

In a monopolistically competitive market, a successful new restaurant

(Multiple Choice)

4.7/5 (34)

Suppose that if a local McDonald's restaurant reduces the price of a Big Mac from $4.00 to $3.25, the number of Big Macs it sells per day will increase from 4 to 5. Explain the output effect and the price effect resulting from this change. Using a graph, illustrate both the loss in revenue from selling each of the first 4 Big Macs for $0.75 less and the additional revenue from selling 1 more Big Mac. What is the total change in revenue received which results from this price decrease?

(Essay)

4.8/5 (35)

Table 13-5

Table 13-5 shows the demand and cost data facing a monopolistically competitive producer of canvas bags.

-Refer to Table 13-5. At the profit-maximizing or loss-minimizing output level,

Table 13-5 shows the demand and cost data facing a monopolistically competitive producer of canvas bags.

-Refer to Table 13-5. At the profit-maximizing or loss-minimizing output level,

(Multiple Choice)

4.9/5 (30)

For a profit-maximizing monopolistically competitive firm, for the last unit sold, the marginal cost of production is less than the marginal benefit received by a customer from the purchase of that unit.

(True/False)

4.7/5 (31)

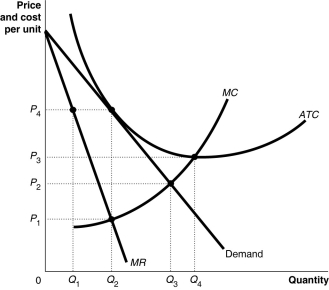

Figure 13-3  -Refer to Figure 13-3. The marginal revenue from one additional unit sold is the sum of the gain in revenue from selling the additional unit and the loss in revenue from having to charge a lower price to sell the additional unit. Based on the diagram in the figure,

-Refer to Figure 13-3. The marginal revenue from one additional unit sold is the sum of the gain in revenue from selling the additional unit and the loss in revenue from having to charge a lower price to sell the additional unit. Based on the diagram in the figure,

(Multiple Choice)

4.8/5 (32)

Which of the following is an example of a factor that a firm's owners and managers can control in making the firm successful?

(Multiple Choice)

4.8/5 (33)

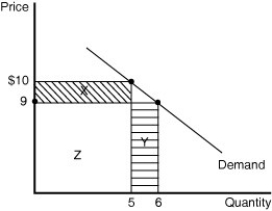

Figure 13-11  -Refer to Figure 13-11. What is the amount of excess capacity?

-Refer to Figure 13-11. What is the amount of excess capacity?

(Multiple Choice)

4.7/5 (35)

A successful trademark is one that becomes a generic name for a product, for example, "Kleenex" has become a generic term for tissues.

(True/False)

4.8/5 (26)

When new firms are encouraged to enter a monopolistically competitive market,

(Multiple Choice)

4.9/5 (28)

Firms such as Caribou Coffee and Diedrich Coffee operate hundreds of coffeehouses nationwide while firms such as Dunn Brothers Coffee operate only in four states. How would you characterize these stores?

(Multiple Choice)

4.9/5 (39)

What are the most important differences between perfectly competitive markets and monopolistically competitive markets?

(Essay)

4.7/5 (31)

If a monopolistically competitive firm lowers its price and, as a result, its total revenue decreases then

(Multiple Choice)

4.7/5 (26)

If firms in a monopolistically competitive industry are making profits in the short run,

(Multiple Choice)

4.7/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)