Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

Suppose a monopolistically competitive firm's output where marginal revenue equals marginal cost is 66 units and the price corresponding to this quantity is $18. If the average total cost at this output is $16.55, then its total profit is

(Multiple Choice)

4.9/5  (31)

(31)

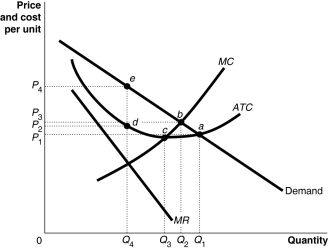

Figure 13-13  -Refer to Figure 13-13. What is the area that represents the firm's profit?

-Refer to Figure 13-13. What is the area that represents the firm's profit?

(Multiple Choice)

4.8/5 (42)

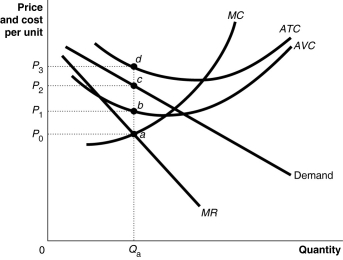

Figure 13-4  Figure 13-4 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-4. What is the area that represents the total variable cost of production?

Figure 13-4 shows short-run cost and demand curves for a monopolistically competitive firm in the market for designer watches.

-Refer to Figure 13-4. What is the area that represents the total variable cost of production?

(Multiple Choice)

4.9/5 (36)

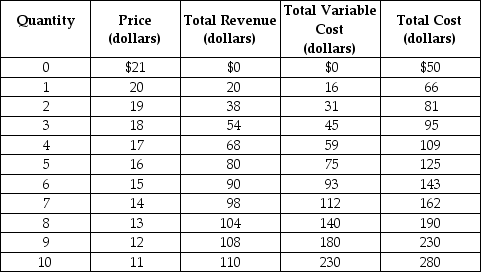

Table 13-3

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3. What are the profit-maximizing/loss-minimizing output level and price?

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3. What are the profit-maximizing/loss-minimizing output level and price?

(Multiple Choice)

4.9/5 (41)

For a monopolistically competitive firm, price equals average revenue.

(True/False)

4.8/5 (37)

The key characteristics of a monopolistically competitive market structure include

(Multiple Choice)

4.7/5 (36)

When a credit card company offers different services with its card, like travel insurance for air travel tickets purchased with the credit card or product insurance for items purchased with the card, the credit card company is trying to

(Multiple Choice)

5.0/5 (39)

The most important of the factors that make a firm successful and that can be controlled by the firm's owners and managers are

(Multiple Choice)

4.8/5 (42)

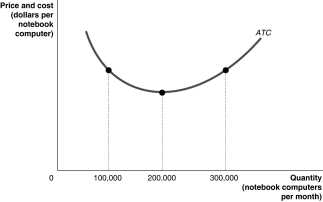

Figure 13-6  -Refer to Figure 13-6. Suppose Dell finds the relationship between the average total cost of producing notebook computers and the quantity of notebook computers produced is as shown by Figure 13-2. Dell will maximize profits if it produces ________ notebook computers per month.

-Refer to Figure 13-6. Suppose Dell finds the relationship between the average total cost of producing notebook computers and the quantity of notebook computers produced is as shown by Figure 13-2. Dell will maximize profits if it produces ________ notebook computers per month.

(Multiple Choice)

4.9/5 (30)

Table 13-3

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3. If this firm continues to produce, what is likely to happen to the product's price in the long run?

(Multiple Choice)

4.9/5 (41)

The ability to engage in product differentiation is one of the factors a manager or owner of a firm can control in order to create value for consumers.

(True/False)

4.9/5 (35)

Excess capacity is a characteristic of monopolistically competitive firms. What does excess capacity mean?

(Multiple Choice)

4.8/5 (41)

If a significant number of smokers switch from smoking tobacco cigarettes to e-cigarettes, a company like NJOY will likely find its demand curve shifting to the ________ and its marginal revenue curve shifting to the ________ as more competitors enter the market.

(Multiple Choice)

4.9/5 (31)

One way by which firms differentiate their products is to find a market niche.

(True/False)

4.9/5 (34)

In long-run equilibrium, compared to a perfectly competitive market, a monopolistically competitive industry produces a ________ level of output and charges a ________ price.

(Multiple Choice)

4.9/5 (40)

One goal a firm tries to achieve when it advertises a product is to

(Multiple Choice)

4.9/5 (37)

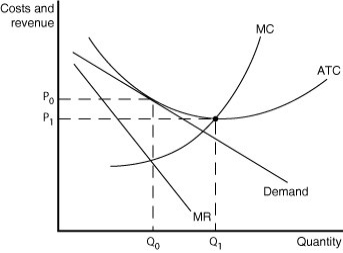

Figure 13-14  Figure 13-14 illustrates a monopolistically competitive firm.

-Refer to Figure 13-14. Which of the following statements describes the firm depicted in the diagram?

Figure 13-14 illustrates a monopolistically competitive firm.

-Refer to Figure 13-14. Which of the following statements describes the firm depicted in the diagram?

(Multiple Choice)

4.8/5 (46)

Consumers in a monopolistically competitive market do not receive any consumer surplus because the price paid for the product exceeds the marginal cost of production.

(True/False)

4.7/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)