Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

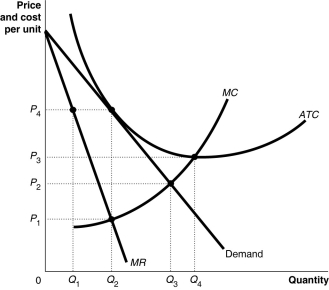

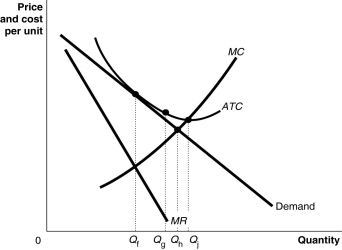

Figure 13-11  -Refer to Figure 13-11. What is the productively efficient output for the firm represented in the diagram?

-Refer to Figure 13-11. What is the productively efficient output for the firm represented in the diagram?

(Multiple Choice)

4.9/5  (30)

(30)

When a monopolistically competitive firm cuts its price to increase its sales, it experiences a gain in revenue due to the

(Multiple Choice)

4.9/5 (38)

According to a Wall Street Journal article, hhgregg has differentiated itself from its competition, particularly from large chain stores such as Best Buy,

(Multiple Choice)

4.8/5 (35)

A monopolistically competitive industry that earns economic profits in the short run will be able to expand its market share even if the market size remains constant.

(True/False)

4.9/5 (28)

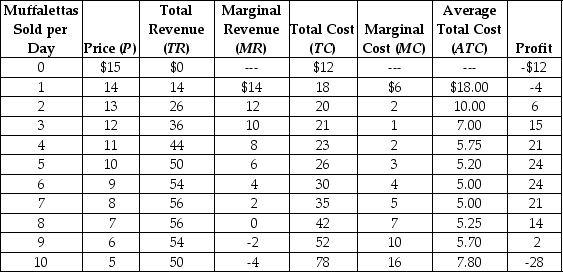

Central Grocery in New Orleans is famous for its muffaletta, a large round sandwich filled with deli meats and topped with a tangy olive salad. Suppose the following table represents cost and revenue data for Central Grocery.

Illustrate this data by graphing the demand, MR, MC, and ATC curves. Identify the profit-maximizing price and quantity, and show the area representing the total profit received by Central Grocery.

Illustrate this data by graphing the demand, MR, MC, and ATC curves. Identify the profit-maximizing price and quantity, and show the area representing the total profit received by Central Grocery.

(Essay)

4.8/5 (30)

Long-run equilibrium in a monopolistically competitive market is similar to long-run equilibrium in a perfectly competitive market in that in both markets, firms

(Multiple Choice)

4.9/5 (44)

Figure 13-11

-Refer to Figure 13-11. What is the monopolistic competitor's profit-maximizing output?

(Multiple Choice)

4.8/5 (29)

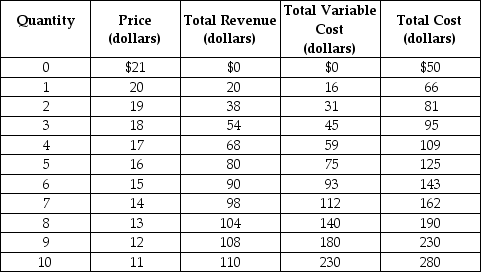

Table 13-4

Table 13-4 lists estimated revenues and costs (per week) for plastic vials (100 vials per box) for the Victoria Biological Supplies Company. Victoria sells plastic vials to university and private research laboratories.

-Refer to Table 13-4. At Victoria's profit-maximizing output,

Table 13-4 lists estimated revenues and costs (per week) for plastic vials (100 vials per box) for the Victoria Biological Supplies Company. Victoria sells plastic vials to university and private research laboratories.

-Refer to Table 13-4. At Victoria's profit-maximizing output,

(Multiple Choice)

4.8/5 (41)

A monopolistically competitive industry that earns economic profits in the short run will face a more elastic demand curve in the long run.

(True/False)

4.8/5 (29)

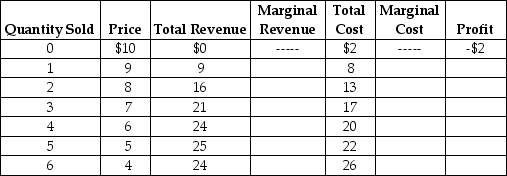

Table 13-3

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3. What is the best course of action for the firm in the short run?

Table 13-3 shows the demand and cost schedules for a monopolistically competitive firm.

-Refer to Table 13-3. What is the best course of action for the firm in the short run?

(Multiple Choice)

4.8/5 (29)

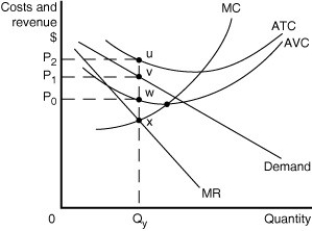

Figure 13-17  -Refer to Figure 13-17. What is the amount of excess capacity?

-Refer to Figure 13-17. What is the amount of excess capacity?

(Multiple Choice)

4.8/5 (25)

A monopolistically competitive firm is producing an output level where marginal revenue is greater than marginal cost. What should this firm do to increase its profit or reduce its losses?

(Multiple Choice)

4.9/5 (37)

Monopolistically competitive firms achieve allocative efficiency but not productive efficiency.

(True/False)

4.8/5 (37)

In the short run, a profit-maximizing firm's decision to produce should be guided by whether

(Multiple Choice)

4.9/5 (42)

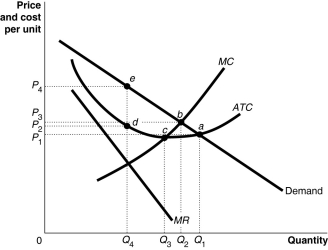

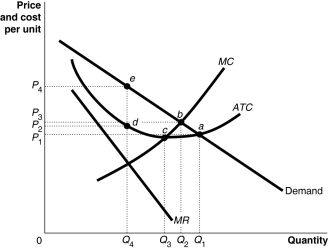

Figure 13-15  -Refer to Figure 13-15 to answer the following questions.

a. What is the profit-maximizing output level?

b. What is the profit-maximizing price?

c. What is the average total cost at the profit-maximizing output level?

d. What area represents the firm's profit?

e. At which output level are economies of scale exhausted?

f. Does this graph most likely represent the long run or the short run? Why?

-Refer to Figure 13-15 to answer the following questions.

a. What is the profit-maximizing output level?

b. What is the profit-maximizing price?

c. What is the average total cost at the profit-maximizing output level?

d. What area represents the firm's profit?

e. At which output level are economies of scale exhausted?

f. Does this graph most likely represent the long run or the short run? Why?

(Essay)

4.8/5 (39)

What is meant by "excess capacity"? How does it relate to consumer utility?

(Essay)

5.0/5 (42)

How does the long-run equilibrium of a monopolistically competitive industry differ from that of a perfectly competitive industry?

(Multiple Choice)

4.8/5 (27)

Figure 13-7  Figure 13-7 shows short-run cost and demand curves for a monopolistically competitive firm in the footwear market.

-Refer to Figure 13-7. Which of the following statements describes the best course of action for the firm depicted in the diagram?

Figure 13-7 shows short-run cost and demand curves for a monopolistically competitive firm in the footwear market.

-Refer to Figure 13-7. Which of the following statements describes the best course of action for the firm depicted in the diagram?

(Multiple Choice)

4.9/5 (41)

Figure 13-13  -Refer to Figure 13-13. What is the profit maximizing output level?

-Refer to Figure 13-13. What is the profit maximizing output level?

(Multiple Choice)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)