Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

A monopolistically competitive firm faces a downward-sloping demand curve because

(Multiple Choice)

4.7/5  (33)

(33)

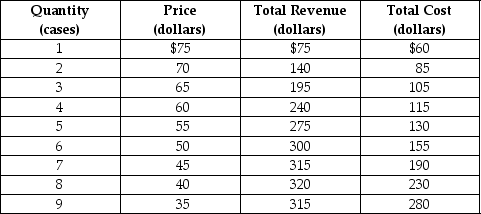

Table 13-2

Eco Energy is a monopolistically competitive producer of a sports beverage called Power On. Table 13-2 shows the firm's demand and cost schedules.

-Refer to Table 13-2. What is the output (Q) that maximizes profit and what is the price (P) charged?

Eco Energy is a monopolistically competitive producer of a sports beverage called Power On. Table 13-2 shows the firm's demand and cost schedules.

-Refer to Table 13-2. What is the output (Q) that maximizes profit and what is the price (P) charged?

(Multiple Choice)

4.8/5 (37)

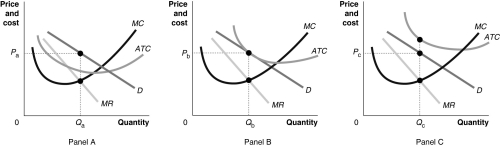

Figure 13-9  -Refer to Figure 13-9. Which of the graphs in the figure depicts a monopolistically competitive firm that is earning economic profits?

-Refer to Figure 13-9. Which of the graphs in the figure depicts a monopolistically competitive firm that is earning economic profits?

(Multiple Choice)

4.8/5 (26)

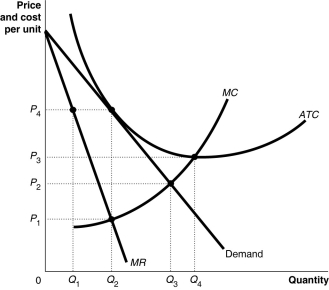

Figure 13-11  -Refer to Figure 13-11. The diagram depicts a firm

-Refer to Figure 13-11. The diagram depicts a firm

(Multiple Choice)

4.8/5 (34)

If some monopolistically competitive firms exit their market after suffering short-run losses, the demand curves of remaining firms will shift to the right.

(True/False)

4.8/5 (27)

Long-run equilibrium under monopolistic competition is similar to that under perfect competition in that

(Multiple Choice)

4.8/5 (42)

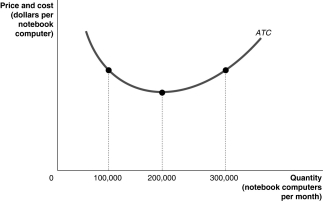

Figure 13-6  -Refer to Figure 13-6. Suppose the above graph represents the relationship between the average total cost of producing notebook computers and the quantity of notebook computers produced by Dell. On a graph, illustrate the demand, MR, MC, and ATC curves which would represent Dell maximizing profits at a quantity of 100,000 per month and identify the area on the graph which represents the profit.

-Refer to Figure 13-6. Suppose the above graph represents the relationship between the average total cost of producing notebook computers and the quantity of notebook computers produced by Dell. On a graph, illustrate the demand, MR, MC, and ATC curves which would represent Dell maximizing profits at a quantity of 100,000 per month and identify the area on the graph which represents the profit.

(Essay)

4.8/5 (35)

In what way does long-run equilibrium under monopolistic competition differ from long-run equilibrium under perfect competition?

(Multiple Choice)

4.8/5 (40)

When a monopolistically competitive firm breaks even in the long run, this is equivalent to earning a zero accounting profit.

(True/False)

4.8/5 (33)

Suppose a monopolistically competitive firm sells 25 units at a price of $10. Calculate its marginal revenue per unit of output if it sells 5 more units of output when it reduced its price to $9.

(Multiple Choice)

4.9/5 (35)

Every firm that has the ability to affect the price of the good or service it sells will

(Multiple Choice)

4.9/5 (35)

Being the first to sell a particular good can give a firm advantages over other firms that sell similar products. What is the name given to these advantages?

(Multiple Choice)

4.8/5 (34)

Which of the following is true for a monopolistically competitive firm in long-run equilibrium?

(Multiple Choice)

4.7/5 (27)

Which of the following describes a difference between the marginal revenue and demand curves of a perfectly competitive firm and a monopolistically competitive firm?

(Multiple Choice)

4.9/5 (34)

Compared to a perfectly competitive firm, the demand curve facing a monopolistically competitive firm is

(Multiple Choice)

4.8/5 (34)

A firm that successfully differentiates its product or lowers its average cost of production creates

(Multiple Choice)

4.8/5 (33)

Consumers in monopolistically competitive markets face a tradeoff between paying prices greater than marginal costs and purchasing products that are more closely suited to their tastes.

(True/False)

4.7/5 (38)

Which of the following is true for a firm with a downward-sloping demand curve for its product?

(Multiple Choice)

4.7/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)