Exam 17: Advanced Issues in Revenue Recognition

Exam 1: The Demand for and Supply of Financial Accounting Information89 Questions

Exam 2: Financial Reporting: Its Conceptual Framework87 Questions

Exam 3: Review of a Companys Accounting System146 Questions

Exam 4: The Balance Sheet and the Statement of Shareholders Equity112 Questions

Exam 5: The Income Statement and the Statement of Cash Flows151 Questions

Exam 6: Cash and Receivables149 Questions

Exam 7: Inventories: Cost Measurement and Flow Assumptions123 Questions

Exam 8: Inventories: Special Valuation Issues148 Questions

Exam 9: Current Liabilities and Contingencies128 Questions

Exam 10: Property, Plant, and Equipment: Acquisition and Subsequent Investments105 Questions

Exam 11: Depreciation, Depletion, Impairment, and Disposal143 Questions

Exam 12: Intangibles105 Questions

Exam 13: Investments and Long-Term Receivables140 Questions

Exam 14: Financing Liabilities: Bonds and Notes Payable171 Questions

Exam 15: Contributed Capital154 Questions

Exam 16: Retained Earnings and Earnings Per Share111 Questions

Exam 17: Advanced Issues in Revenue Recognition113 Questions

Exam 18: Accounting for Income Taxes108 Questions

Exam 19: Accounting for Postretirement Benefits98 Questions

Exam 20: Accounting for Leases149 Questions

Exam 21: The Statement of Cash Flows107 Questions

Exam 22: Accounting for Changes and Errors130 Questions

Exam 23: Time Value of Money Module121 Questions

Select questions type

Exhibit 17-5 Kusick Co. sold a franchise at an initial franchise fee of $15,000. A down payment of $4,800 was received with the balance covered by the issuance of a $10,200, 6% note payable by the franchisee in four equal annual installments. The refund period has expired and the collectibility of the note is reasonably assured.

-Refer to Exhibit 17-5. If all material services have not been substantially performed, which entry to record the franchise is correct?

(Multiple Choice)

4.8/5  (44)

(44)

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:  -Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the net amount reported for construction in progress inventory at the end of 2015 would be

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the net amount reported for construction in progress inventory at the end of 2015 would be

(Multiple Choice)

4.7/5 (43)

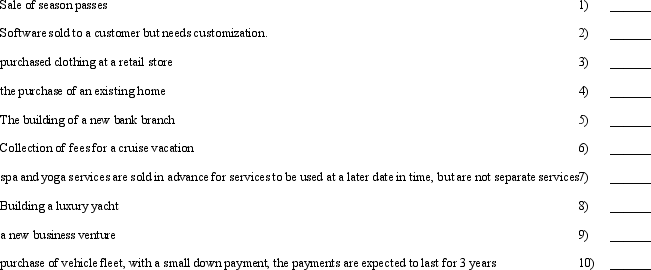

Revenue Recognition Methods:

Revenue Recognition Methods:  Required:

For each situation indicate what method of revenue recognition would be most appropriate.

Required:

For each situation indicate what method of revenue recognition would be most appropriate.

(Essay)

4.8/5 (42)

The period in which a company recognizes revenue is also the period in which it recognizes an increase in the

(Multiple Choice)

5.0/5 (40)

Exhibit 17-4 The following information is provided for Fort Myers Company:  Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much deferred gross profit is still on the books at the end of 2015?

Fort Myers used the installment sales method.

-Refer to Exhibit 17-4. How much deferred gross profit is still on the books at the end of 2015?

(Multiple Choice)

4.9/5 (37)

In real estate sales, what method of revenue recognition must be used if the sale is not consummated?

(Multiple Choice)

4.9/5 (41)

Under the completed-contract method of revenue recognition, the partial billings account is closed out against the

(Multiple Choice)

4.7/5 (39)

If a company has an agreement to deliver software that does not require significant production, modification, or customization of software then revenue is recognized based upon the percentage-of-completion method.

(True/False)

4.8/5 (32)

If the consignee uses a consignment-in account and has a debit balance, the

(Multiple Choice)

4.7/5 (32)

What are the advantages of using the percentage-of-completion method of revenue recognition?

(Essay)

4.8/5 (32)

It is important to understand the difference between an installment sale and the installment method of revenue recognition, which a company recognizes revenue in full at the time of the sale if collectibility is reasonably assured.

(True/False)

4.8/5 (32)

The installment and the cost recovery are methods that recognize revenue after the earnings process is complete and when realization occurs.

(True/False)

4.9/5 (33)

Exhibit 17-2 The following information relates to a project of the Cumberland Construction Company:  The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2014?

The contract price was $1,000,000. Cumberland used the percentage-of-completion method of revenue recognition.

-Refer to Exhibit 17-2. What amount of gross profit was recognized in 2014?

(Multiple Choice)

4.8/5 (37)

When revenue is recognized in the period of the sale, generally

(Multiple Choice)

4.8/5 (46)

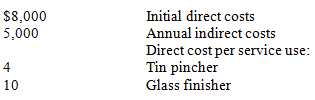

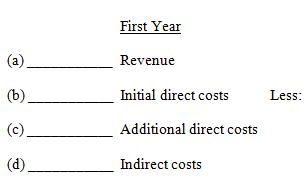

Charleston, Inc. sold 800 contracts at $400 each. Each contract permitted the buyer to use a tin pincher 16 times and a glass finisher 20 times. Cost information follows:  In the first year, the tin pincher was used 4,500 times and the glass finisher was used 4,800 times.

Required:

Fill in the lines below.

In the first year, the tin pincher was used 4,500 times and the glass finisher was used 4,800 times.

Required:

Fill in the lines below.

(Essay)

4.8/5 (35)

Exhibit 17-1 In 2014, Omega Construction began work on a contract with a price of $850,000 and estimated costs of $595,000. Data for each year of the contract are as follows:  -Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the balance in Construction in Progress at the end of 2015 would be

-Refer to Exhibit 17-1. Under the percentage-of-completion method of revenue recognition, the balance in Construction in Progress at the end of 2015 would be

(Multiple Choice)

4.8/5 (35)

In selecting the appropriate method of recognizing revenue, which of the following qualitative characteristics of useful accounting information is paramount to the decision?

(Multiple Choice)

4.8/5 (38)

A company may recognize revenue in full at the time of a sale if

(Multiple Choice)

4.8/5 (39)

At what point would using the cost recovery method over the installment method be appropriate?

(Essay)

4.8/5 (36)

Rising Sun, Inc. repossessed an item in 2014 with a gross profit of 15%. The fair value of the repossessed item was $11,900. The amount still unpaid was $15,000.

Required:

Prepare the journal entry to record the repossession of this item.

(Essay)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)