Exam 5: Uncertainty and Consumer Behavior

Exam 1: Preliminaries78 Questions

Exam 2: The Basics of Supply and Demand139 Questions

Exam 3: Consumer Behavior134 Questions

Exam 4: Individual and Market Demand131 Questions

Exam 5: Uncertainty and Consumer Behavior150 Questions

Exam 6: Production125 Questions

Exam 7: The Cost of Production178 Questions

Exam 8: Profit Maximization and Competitive Supply164 Questions

Exam 9: The Analysis of Competitive Markets183 Questions

Exam 10: Market Power: Monopoly and Monopsony158 Questions

Exam 11: Pricing With Market Power130 Questions

Exam 12: Monopolistic Competition and Oligopoly120 Questions

Exam 13: Game Theory and Competitive Strategy150 Questions

Exam 14: Markets for Factor Inputs134 Questions

Exam 15: Investment, Time, and Capital Markets153 Questions

Exam 16: General Equilibrium and Economic Efficiency126 Questions

Exam 17: Markets With Asymmetric Information133 Questions

Exam 18: Externalities and Public Goods131 Questions

Exam 19: Behavioral Economics101 Questions

Select questions type

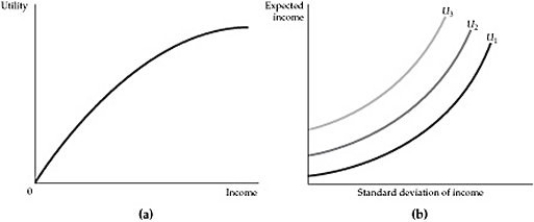

Figure 5.2.1

-Refer to Figure 5.2.1 above. Which of the two figures describes a risk averse individual?

Figure 5.2.1

-Refer to Figure 5.2.1 above. Which of the two figures describes a risk averse individual?

Free

(Multiple Choice)

4.9/5  (39)

(39)

Correct Answer: Verified

Verified

C

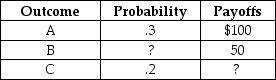

Scenario 5.4:

Suppose an individual is considering an investment in which there are exactly three possible outcomes, whose probabilities and payoffs are given below:

The expected value of the investment is $25. Although all the information is correct, information is missing.

-Refer to Scenario 5.4. What is the payoff of outcome C?

The expected value of the investment is $25. Although all the information is correct, information is missing.

-Refer to Scenario 5.4. What is the payoff of outcome C?

Free

(Multiple Choice)

4.9/5 (34)

Correct Answer:Verified

A

During the most recent recession, many people temporarily lost substantial value in their retirement investment portfolios because most of the assets (including stocks, bonds, and real estate) all declined in value at the same time. In hindsight, what was the problem with these portfolios?

Free

(Multiple Choice)

4.9/5 (36)

Correct Answer:Verified

B

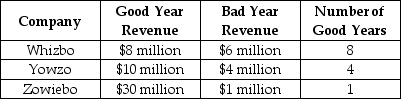

Scenario 5.3:

Wanting to invest in the computer games industry, you select Whizbo, Yowzo and Zowiebo as the three best firms. Over the past 10 years, the three firms have had good years and bad years. The following table shows their performance:

-Refer to Scenario 5.3. Where is the highest expected revenue, based on the 10 years' past performance?

-Refer to Scenario 5.3. Where is the highest expected revenue, based on the 10 years' past performance?

(Multiple Choice)

4.9/5 (27)

Scenario 5.10:

Hillary can invest her family savings in two assets: riskless Treasury bills or a risky vacation home real estate project on an Arkansas river. The expected return on Treasury bills is 4 percent with a standard deviation of zero. The expected return on the real estate project is 30 percent with a standard deviation of 40 percent.

-Refer to Scenario 5.10. If Hillary invests 30 percent of her savings in the real estate project and the remainder in Treasury bills, the expected return on her portfolio is:

(Multiple Choice)

4.9/5 (31)

Blanca would prefer a certain income of $20,000 to a gamble with a 0.5 probability of $10,000 and a 0.5 probability of $30,000. Based on this information:

(Multiple Choice)

4.9/5 (34)

When facing a 50% chance of receiving $50 and a 50% chance of receiving $100, the individual pictured in Figure 5.2.2:

(Multiple Choice)

4.8/5 (33)

Bill's utility function takes the form U(I) = exp(I) where I is Bill's income. Based on this utility function, we can see that Bill is:

(Multiple Choice)

4.9/5 (40)

The weighted average of all possible outcomes of a project, with the probabilities of the outcomes used as weights, is known as the:

(Multiple Choice)

4.9/5 (33)

In Eugene, Oregon, next year there is a 2% chance of an earthquake severe enough to destroy all buildings and personal property. Quincy, who has $3,000,000 in buildings and personal property, has the opportunity to purchase complete earthquake insurance. Which is true?

(Multiple Choice)

4.7/5 (30)

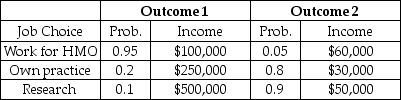

The information in the table below describes choices for a new doctor. The outcomes represent different macroeconomic environments, which the individual cannot predict.Table 5.3

-In Table 5.3, the standard deviation is:

-In Table 5.3, the standard deviation is:

(Multiple Choice)

4.9/5 (34)

Irene's utility of income function is  Irene is offered the following game of chance. The odds of winning are 1/100 and the payoff is 75 times the wager. If she loses, she loses her wager amount. Calculate Irene's expected utility of the game.

Irene is offered the following game of chance. The odds of winning are 1/100 and the payoff is 75 times the wager. If she loses, she loses her wager amount. Calculate Irene's expected utility of the game.

(Essay)

4.8/5 (26)

The standard deviation of a two-asset portfolio (with a risky and a non-risky asset) is equal to:

(Multiple Choice)

4.9/5 (39)

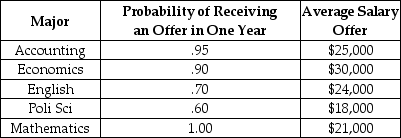

Consider the following information about job opportunities for new college graduates in Megalopolis:Table 5.1

-Refer to Table 5.1. A risk-neutral individual making a decision solely on the basis of the above information would choose to major in:

-Refer to Table 5.1. A risk-neutral individual making a decision solely on the basis of the above information would choose to major in:

(Multiple Choice)

4.8/5 (36)

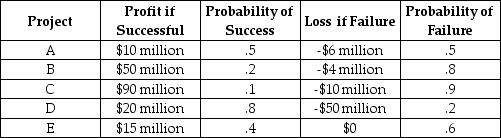

Scenario 5.7:

As president and CEO of MegaWorld Industries, Natasha must decide on some very risky alternative investments. Consider the following:

-Refer to Scenario 5.7. As a risk-neutral executive, Natasha:

-Refer to Scenario 5.7. As a risk-neutral executive, Natasha:

(Multiple Choice)

4.9/5 (30)

Individuals who fully insure their house and belongings against fire:

(Multiple Choice)

4.7/5 (33)

To optimally deter crime, law enforcement authorities should:

(Multiple Choice)

4.8/5 (22)

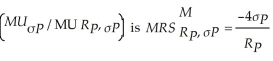

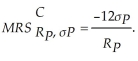

Mel and Christy are co-workers with different risk attitudes. Both have investments in the stock market and hold U.S. Treasury securities (which provide the risk free rate of return). Mel's marginal rate of substitution of return for risk  where

where  is the individual's portfolio rate of return and σP is the individual's portfolio risk. Christy's

is the individual's portfolio rate of return and σP is the individual's portfolio risk. Christy's  Each co-worker's budget constraint is

Each co-worker's budget constraint is  where

where  is the risk-free rate of return,

is the risk-free rate of return,  is the stock market rate of return, and

is the stock market rate of return, and  is the stock market risk. Solve for each co-worker's optimal portfolio rate of return as a function of

is the stock market risk. Solve for each co-worker's optimal portfolio rate of return as a function of  ,

,  and

and  .

.

(Essay)

4.9/5 (35)

Jack is near retirement and worried that if the stock market falls he will not be able to wait to take his funds out, and will have to sell at the bottom of the market. Richard thinks the probability of a stock market downturn is the same, but he is only 40 and could therefore wait for another turnaround. They face the same budget line. Jack's risk/return indifference curve:

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)