Exam 16: Time-Series Forecasting

Exam 1: Defining and Collecting Data189 Questions

Exam 3: Numerical Descriptive Measures184 Questions

Exam 4: Basic Probability156 Questions

Exam 5: Discrete Probability Distributions218 Questions

Exam 6: The Normal Distribution and Other Continuous Distributions189 Questions

Exam 7: Sampling Distributions127 Questions

Exam 8: Confidence Interval Estimation196 Questions

Exam 9: Fundamentals of Hypothesis Testing: One-Sample Tests170 Questions

Exam 10: Two-Sample Tests210 Questions

Exam 11: Analysis of Variance130 Questions

Exam 12: Chi-Square Tests and Nonparametric Tests175 Questions

Exam 13: Simple Linear Regression213 Questions

Exam 14: Introduction to Multiple Regression337 Questions

Exam 15: Multiple Regression Model Building96 Questions

Exam 16: Time-Series Forecasting165 Questions

Exam 17: A Roadmap for Analyzing Data303 Questions

Exam 18: Statistical Applications in Quality Management130 Questions

Exam 19: Decision Making126 Questions

Exam 20: Index Numbers44 Questions

Exam 21: Chi-Square Tests for the Variance or Standard Deviation11 Questions

Exam 22: Mcnemar Test for the Difference Between Two Proportions Related Samples15 Questions

Exam 25: The Analysis of Means Anom2 Questions

Exam 23: The Analysis of Proportions Anop3 Questions

Exam 24: The Randomized Block Design85 Questions

Exam 26: The Power of a Test41 Questions

Exam 27: Estimation and Sample Size Determination for Finite Populations13 Questions

Exam 28: Application of Confidence Interval Estimation in Auditing13 Questions

Exam 29: Sampling From Finite Populations20 Questions

Exam 30: The Normal Approximation to the Binomial Distribution27 Questions

Exam 31: Counting Rules14 Questions

Exam 32: Lets Get Started Big Things to Learn First33 Questions

Select questions type

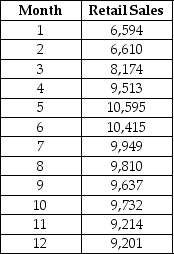

TABLE 16-5

The number of passengers arriving at San Francisco on the Amtrak cross-country express on 6 successive Mondays were: 60,72,96,84,36,and 48.

-Referring to Table 16-5,the number of arrivals will be smoothed with a 5-term moving average.The last smoothed value will be ________.

(Short Answer)

4.7/5  (33)

(33)

TABLE 16-13

Given below is the monthly time-series data for U.S.retail sales of building materials over a specific year.  The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

Linear trend model:

The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

Linear trend model:  Quadratic trend model:

Quadratic trend model:  Exponential trend model:

Exponential trend model:  First-order autoregressive:

First-order autoregressive:  Second-order autoregressive:

Second-order autoregressive:  Third-order autoregressive:

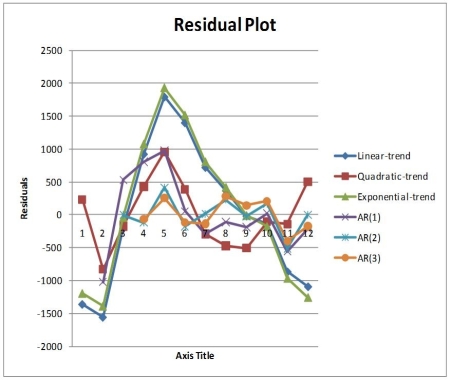

Third-order autoregressive:  Below is the residual plot of the various models:

Below is the residual plot of the various models:  -True or False: Referring to Table 16-13,the best model based on the residual plots is the exponential-trend regression model.

-True or False: Referring to Table 16-13,the best model based on the residual plots is the exponential-trend regression model.

(True/False)

4.8/5 (41)

TABLE 16-13

Given below is the monthly time-series data for U.S.retail sales of building materials over a specific year. The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

Linear trend model: Quadratic trend model: Exponential trend model: First-order autoregressive: Second-order autoregressive: Third-order autoregressive: Below is the residual plot of the various models:

-Referring to Table 16-13,what is the exponentially smoothed value for the first month using a smoothing coefficient of W = 0.25?

(Short Answer)

4.8/5 (37)

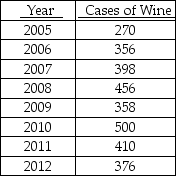

TABLE 16-4

The number of cases of merlot wine sold by a Paso Robles winery in an 8-year period follows.  -Referring to Table 16-4,exponential smoothing with a weight or smoothing constant of 0.4 will be used to forecast wine sales.The forecast for 2013 is ________.

-Referring to Table 16-4,exponential smoothing with a weight or smoothing constant of 0.4 will be used to forecast wine sales.The forecast for 2013 is ________.

(Short Answer)

4.9/5 (45)

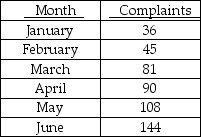

TABLE 16-3

The following table contains the number of complaints received in a department store for the first 6 months of last year.  -Referring to Table 16-3,if this series is smoothed using exponential smoothing with a smoothing constant of

-Referring to Table 16-3,if this series is smoothed using exponential smoothing with a smoothing constant of  ,what would be the third value?

,what would be the third value?

(Multiple Choice)

4.9/5 (29)

TABLE 16-4

The number of cases of merlot wine sold by a Paso Robles winery in an 8-year period follows.

-Referring to Table 16-4,exponentially smooth the wine sales with a weight or smoothing constant of 0.4.

(Essay)

4.9/5 (36)

TABLE 16-13

Given below is the monthly time-series data for U.S.retail sales of building materials over a specific year. The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

Linear trend model: Quadratic trend model: Exponential trend model: First-order autoregressive: Second-order autoregressive: Third-order autoregressive: Below is the residual plot of the various models:

-Referring to Table 16-13,what is the p-value of the t test statistic for testing the appropriateness of the third-order autoregressive model?

(Short Answer)

4.8/5 (40)

TABLE 16-3

The following table contains the number of complaints received in a department store for the first 6 months of last year.

-Referring to Table 16-3,if a three-month moving average is used to smooth this series,what would be the second calculated value?

(Multiple Choice)

4.9/5 (30)

TABLE 16-13

Given below is the monthly time-series data for U.S.retail sales of building materials over a specific year. The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

Linear trend model: Quadratic trend model: Exponential trend model: First-order autoregressive: Second-order autoregressive: Third-order autoregressive: Below is the residual plot of the various models:

-Referring to Table 16-13,what is the exponentially smoothed forecast for the 13th month using a smoothing coefficient of W = 0.25 if the exponentially smooth value for the 10th and 11th month are 9,477.7776 and 9,411.8332,respectively?

(Short Answer)

4.9/5 (44)

TABLE 16-9

Given below are EXCEL outputs for various estimated autoregressive models for a company's real operating revenues (in billions of dollars)from 1989 to 2012.From the data,you also know that the real operating revenues for 2010,2011,and 2012 are 11.7909,11.7757 and 11.5537,respectively.

First-Order Autoregressive Model:  Second-Order Autoregressive Model:

Second-Order Autoregressive Model:  Third-Order Autoregressive Model:

Third-Order Autoregressive Model:  -Referring to Table 16-9,if one decides to use the Third-Order Autoregressive model,what will the predicted real operating revenue for the company be in 2014?

-Referring to Table 16-9,if one decides to use the Third-Order Autoregressive model,what will the predicted real operating revenue for the company be in 2014?

(Multiple Choice)

4.8/5 (34)

The annual multiplicative time-series model does not possess ________ component.

(Multiple Choice)

4.8/5 (35)

TABLE 16-5

The number of passengers arriving at San Francisco on the Amtrak cross-country express on 6 successive Mondays were: 60,72,96,84,36,and 48.

-Referring to Table 16-5,the number of arrivals will be exponentially smoothed with a smoothing constant of 0.25.The forecast of the number of arrivals on the seventh Monday will be ________.

(Short Answer)

4.8/5 (33)

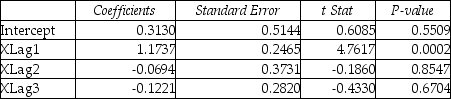

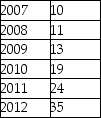

TABLE 16-10

Business closures in Laramie,Wyoming from 2007 to 2012 were:  Microsoft Excel was used to fit both first-order and second-order autoregressive models,resulting in the following partial outputs:

SUMMARY OUTPUT - 2nd Order Model

Coefficients

Intercept -5.77

X Variable 1 0.80

X Variable 2 1.14

SUMMARY OUTPUT - 1st Order Model

Coefficients

Intercept -4.16

X Variable 1 1.59

-Referring to Table 16-10,the value of the MAD for the second-order autoregressive model is ________.

Microsoft Excel was used to fit both first-order and second-order autoregressive models,resulting in the following partial outputs:

SUMMARY OUTPUT - 2nd Order Model

Coefficients

Intercept -5.77

X Variable 1 0.80

X Variable 2 1.14

SUMMARY OUTPUT - 1st Order Model

Coefficients

Intercept -4.16

X Variable 1 1.59

-Referring to Table 16-10,the value of the MAD for the second-order autoregressive model is ________.

(Short Answer)

4.9/5 (36)

TABLE 16-9

Given below are EXCEL outputs for various estimated autoregressive models for a company's real operating revenues (in billions of dollars)from 1989 to 2012.From the data,you also know that the real operating revenues for 2010,2011,and 2012 are 11.7909,11.7757 and 11.5537,respectively.

First-Order Autoregressive Model: Second-Order Autoregressive Model: Third-Order Autoregressive Model:

-Referring to Table 16-9 and using a 5% level of significance,what is the appropriate autoregressive model for the company's real operating revenue?

(Multiple Choice)

4.8/5 (40)

True or False: Given a data set with 15 yearly observations,there are only thirteen 3-year moving averages.

(True/False)

4.9/5 (35)

TABLE 16-14

A contractor developed a multiplicative time-series model to forecast the number of contracts in future quarters,using quarterly data on number of contracts during the 3-year period from 2010 to 2012.The following is the resulting regression equation:

ln  = 3.37 + 0.117 X - 0.083 Q1 + 1.28 Q2 + 0.617 Q3

where

= 3.37 + 0.117 X - 0.083 Q1 + 1.28 Q2 + 0.617 Q3

where  is the estimated number of contracts in a quarter

X is the coded quarterly value with X = 0 in the first quarter of 2010

Q1 is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise

Q2 is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise

Q3 is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise

-Referring to Table 16-14,to obtain a forecast for the first quarter of 2013 using the model,which of the following sets of values should be used in the regression equation?

is the estimated number of contracts in a quarter

X is the coded quarterly value with X = 0 in the first quarter of 2010

Q1 is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise

Q2 is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise

Q3 is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise

-Referring to Table 16-14,to obtain a forecast for the first quarter of 2013 using the model,which of the following sets of values should be used in the regression equation?

(Multiple Choice)

4.8/5 (42)

TABLE 16-8

The manager of a marketing consulting firm has been examining his company's yearly profits.He believes that these profits have been showing a quadratic trend since 1994.He uses Microsoft Excel to obtain the partial output below.The dependent variable is profit (in thousands of dollars),while the independent variables are coded years and squared of coded years,where 1994 is coded as 0,1995 is coded as 1,etc.

SUMMARY OUTPUT

Regression Statistics

Multiple R 0.998

R Square 0.996

Adjusted R Square 0.996

Standard Error 4.996

Observations 17

Coefficients

Intercept 35.5

Coded Year 0.45

Year Squared 1.00

-Referring to Table 16-8,the fitted value for 1994 is ________.

(Short Answer)

4.8/5 (40)

The effect of an unpredictable,rare event will be contained in the ________ component.

(Multiple Choice)

4.9/5 (39)

TABLE 16-13

Given below is the monthly time-series data for U.S.retail sales of building materials over a specific year. The results of the linear trend,quadratic trend,exponential trend,first-order autoregressive,second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the 1st month is 0:

Linear trend model: Quadratic trend model: Exponential trend model: First-order autoregressive: Second-order autoregressive: Third-order autoregressive: Below is the residual plot of the various models:

-Referring to Table 16-13,if a five-month moving average is used to smooth this series,how many moving averages can you compute?

(Short Answer)

4.9/5 (31)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)