Exam 22: Accounting Changes and Error Analysis

Exam 1: Financial Accounting and Accounting Standards103 Questions

Exam 2: Conceptual Framework for Financial Reporting155 Questions

Exam 3: The Accounting Information System144 Questions

Exam 4: Income Statement and Related Information139 Questions

Exam 5: Balance Sheet and Statement of Cash Flows127 Questions

Exam 6: Accounting and the Time Value of Money152 Questions

Exam 7: Cash and Receivables173 Questions

Exam 8: Valuation of Inventories: a Cost-Basis Approach173 Questions

Exam 9: Inventories: Additional Valuation Issues168 Questions

Exam 10: Acquisition and Disposition of Property, Plant, and Equipment170 Questions

Exam 11: Depreciation, Impairments, and Depletion156 Questions

Exam 12: Intangible Assets171 Questions

Exam 13: Current Liabilities and Contingencies170 Questions

Exam 14: Long-Term Liabilities140 Questions

Exam 15: Stockholders Equity155 Questions

Exam 16: Dilutive Securities and Earnings Per Share160 Questions

Exam 17: Investments141 Questions

Exam 18: Revenue Recognition145 Questions

Exam 19: Accounting for Income Taxes127 Questions

Exam 20: Accounting for Pensions and Postretirement Benefits137 Questions

Exam 21: Accounting for Leases128 Questions

Exam 22: Accounting Changes and Error Analysis103 Questions

Exam 23: Statement of Cash Flows143 Questions

Exam 24: Full Disclosure in Financial Reporting108 Questions

Exam 25: Appendix89 Questions

Select questions type

On January 1, 2010, Powell Company purchased a building and machinery that have the following useful lives, salvage value, and costs.Building, 25-year estimated useful life, $6,000,000 cost, $600,000 salvage valueMachinery, 10-year estimated useful life, $800,000 cost, no salvage valueThe building has been depreciated under the straight-line method through 2014. In 2015, the company decided to switch to the double-declining balance method of depreciation for the building. Powell also decided to change the total useful life of the machinery to 8 years, with a salvage value of $40,000 at the end of that time. The machinery is depreciated using the straight-line method.

Instructions

(a) Prepare the journal entry necessary to record the depreciation expense on the building in 2015.

(b) Compute depreciation expense on the machinery for 2015.

(Essay)

4.8/5  (38)

(38)

On January 1, 2012, Piper Co., purchased a machine (its only depreciable asset) for $600,000. The machine has a five-year life, and no salvage value. Sum-of-the-years'-digits depreciation has been used for financial statement reporting and the elective straight-line method for income tax reporting. Effective January 1, 2015, for financial statement reporting, Piper decided to change to the straight-line method for depreciation of the machine. Assume that Piper can justify the change.Piper's income before depreciation, before income taxes, and before the cumulative effect of the accounting change (if any), for the year ended December 31, 2015, is $500,000. The income tax rate for 2015, as well as for the years 2012-2014, is 30%. What amount should Piper report as net income for the year ended December 31, 2015?

(Multiple Choice)

4.9/5 (42)

Use the following information for questions 61 through 63.

Bishop Co. began operations on January 1, 2014. Financial statements for 2014 and 2015 con- tained the following errors:  In addition, on December 31, 2015 fully depreciated equipment was sold for $28,800, but the sale was not recorded until 2016. No corrections have been made for any of the errors. Ignore income tax considerations.

-The total effect of the errors on the amount of Bishop's working capital at December 31, 2015 is understated by

In addition, on December 31, 2015 fully depreciated equipment was sold for $28,800, but the sale was not recorded until 2016. No corrections have been made for any of the errors. Ignore income tax considerations.

-The total effect of the errors on the amount of Bishop's working capital at December 31, 2015 is understated by

(Multiple Choice)

4.8/5 (36)

Under IFRS, the direct effects of changes in the accounting policies are applied retrospectively.

(True/False)

4.8/5 (49)

Discuss the accounting procedures for and illustrate the following:(a) Change in estimate(b) Change in reporting entity(c) Correction of an error

(Essay)

4.8/5 (37)

An indirect effect of an accounting change is any change to current or future cash flows of a company that result from making a change in accounting principle that is applied retrospectively.

(True/False)

4.8/5 (34)

Dyke Company's net incomes for the past three years are presented below:  During the 2016 year-end audit, the following items come to your attention:1. Dyke bought equipment on January 1, 2013 for $392,000 with a $32,000 estimated salvage value and a six-year life. The company debited an expense account and credited cash on the purchase date for the entire cost of the asset. (Straight-line method)"2. During 2016, Dyke changed from the straight-line method of depreciating its cement plant to the double-declining balance method. The following computations present depreciation on both bases:

During the 2016 year-end audit, the following items come to your attention:1. Dyke bought equipment on January 1, 2013 for $392,000 with a $32,000 estimated salvage value and a six-year life. The company debited an expense account and credited cash on the purchase date for the entire cost of the asset. (Straight-line method)"2. During 2016, Dyke changed from the straight-line method of depreciating its cement plant to the double-declining balance method. The following computations present depreciation on both bases:  The net income for 2016 was computed using the double-declining balance method, on the January 1, 2016 book value, over the useful life remaining at that time. The depreciation recorded in 2016 was $72,000.""3. Dyke, in reviewing its provision for uncollectibles during 2014, has determined that 1% is the appropriate amount of bad debt expense to be charged to operations. The company had used 1/2 of 1% as its rate in 2015 and 2016 when the expense had been $18,000 and $12,000, respectively. The company recorded bad debt expense under the new rate for 2016. The company would have recorded $6,000 less of bad debt expense on December 31, 2016 under the old rate.

Instructions

(a) Prepare in general journal form the entry necessary to correct the books for the transaction in part 1 of this problem, assuming that the books have not been closed for the current year.

(b) Compute the net income to be reported each year 2014 through 2016.

(c) Assume that the beginning retained earnings balance (unadjusted) for 2014 was $1,260,000. At what adjusted amount should this beginning retained earnings balance for 2014 be stated, assuming that comparative financial statements were prepared?(d) Assume that the beginning retained earnings balance (unadjusted) for 2016 is $1,800,000 and that non-comparative financial statements are prepared. At what adjusted amount should this beginning retained earnings balance be stated?"

The net income for 2016 was computed using the double-declining balance method, on the January 1, 2016 book value, over the useful life remaining at that time. The depreciation recorded in 2016 was $72,000.""3. Dyke, in reviewing its provision for uncollectibles during 2014, has determined that 1% is the appropriate amount of bad debt expense to be charged to operations. The company had used 1/2 of 1% as its rate in 2015 and 2016 when the expense had been $18,000 and $12,000, respectively. The company recorded bad debt expense under the new rate for 2016. The company would have recorded $6,000 less of bad debt expense on December 31, 2016 under the old rate.

Instructions

(a) Prepare in general journal form the entry necessary to correct the books for the transaction in part 1 of this problem, assuming that the books have not been closed for the current year.

(b) Compute the net income to be reported each year 2014 through 2016.

(c) Assume that the beginning retained earnings balance (unadjusted) for 2014 was $1,260,000. At what adjusted amount should this beginning retained earnings balance for 2014 be stated, assuming that comparative financial statements were prepared?(d) Assume that the beginning retained earnings balance (unadjusted) for 2016 is $1,800,000 and that non-comparative financial statements are prepared. At what adjusted amount should this beginning retained earnings balance be stated?"

(Essay)

4.9/5 (40)

Which type of accounting change should always be accounted for in current and future periods?

(Multiple Choice)

4.8/5 (39)

Under IFRS, errors in financial statements are considered as an accounting change.

(True/False)

4.9/5 (37)

In the process of conversion from the equity method to the fair value method, the earnings or losses that the investor previously recognized under the equity method should:

(Multiple Choice)

4.7/5 (30)

Stone Company changed its method of pricing inventories from FIFO to LIFO. What type of accounting change does this represent?

(Multiple Choice)

4.7/5 (30)

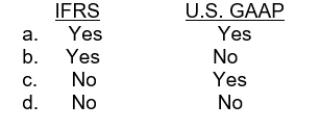

Is the following exception applicable to IFRS or U.S. GAAP?"If determining the effect of a correction of an error is considered impracticable, then a company should report the effect of the error correction in the period in which it believes it practicable to do so."

(Short Answer)

4.7/5 (35)

On January 1, 2012, Hess Co. purchased a patent for $952,000. The patent is being amortized over its remaining legal life of 15 years expiring on January 1, 2027. During 2015, Hess determined that the economic benefits of the patent would not last longer than ten years from the date of acquisition. What amount should be reported in the balance sheet for the patent, net of accumulated amortization, at December 31, 2015?

(Multiple Choice)

4.9/5 (37)

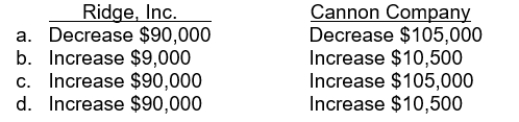

Ridge, Inc. follows IFRS for its external financial reporting, and Cannon Company follows U.S. GAAP for its external financial reporting. During 2015, both companies changed depreciation methods, from double-declining balance to straight-line. Compared to double-declining balance, for Ridge, Inc. the change resulted in a decrease in reported depreciation expense of $90,000, and for Cannon Company the change resulted in a reported decrease in depreciation expense of $105,000. The remaining useful lives of the assets impacted by the change in depreciation method is 10 years for both companies. How would this change impact the net income reported by Ridge, Inc. and Cannon Company for the year ended December 31, 2015?

(Short Answer)

4.7/5 (37)

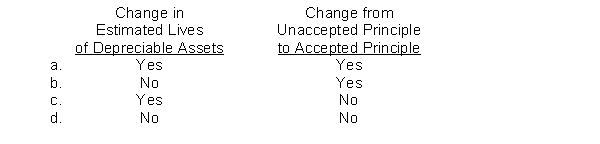

Matching accounting changes to situations.The four types of accounting changes, including error correction, are:Code

a. Change in accounting principle.

b. Change in accounting estimate.

c. Change in reporting entity.

d. Error correction.

Instructions

Following are a series of situations. You are to enter a code letter to the left to indicate the type of change.

1. Change from presenting nonconsolidated to consolidated financial statements.

2. Change due to charging a new asset directly to an expense account.

3. Change from expensing to capitalizing certain costs, due to a change in periods benefited.

4. Change from FIFO to LIFO inventory procedures.

5. Change due to failure to recognize an accrued (uncollected) revenue.

6. Change in amortization period for an intangible asset.

7. Changing the companies included in combined financial statements.

8. Change in the loss rate on warranty costs.

9. Change due to failure to recognize and accrue income.

10. Change in residual value of a depreciable plant asset.

11. Change from an unacceptable to an acceptable accounting principle.

12. Change in both estimate and acceptable accounting principles.

13. Change due to failure to recognize a prepaid asset.

14. Change from straight-line to sum-of-the-years'-digits method of depreciation.

15. Change in life of a depreciable plant asset.

16. Change from one acceptable principle to another acceptable principle.

17. Change due to understatement of inventory.

18. Change in expected recovery of an account receivable.

(Essay)

4.9/5 (32)

Which of the following describes a change in reporting entity?

(Multiple Choice)

4.8/5 (36)

Quigley Co. bought a machine on January 1, 2013 for $1,400,000. It had a $120,000 estimated residual value and a ten-year life. An expense account was debited on the purchase date. Quigley uses straight-line depreciation. This was discovered in 2015.

InstructionsPrepare the entry or entries related to the machine for 2015.

(Essay)

5.0/5 (42)

Use the following information for questions 57 through 59.

Langley Company's December 31 year-end financial statements contained the following errors:  An insurance premium of $54,000 was prepaid in 2014 covering the years 2014, 2015, and 2016. The prepayment was recorded with a debit to insurance expense. In addition, on December 31, 2015, fully depreciated machinery was sold for $28,500 cash, but the sale was not recorded until 2016. There were no other errors during 2015 or 2016 and no corrections have been made for any of the errors. Ignore income tax considerations.

-What is the total net effect of the errors on Langley's 2015 net income?

An insurance premium of $54,000 was prepaid in 2014 covering the years 2014, 2015, and 2016. The prepayment was recorded with a debit to insurance expense. In addition, on December 31, 2015, fully depreciated machinery was sold for $28,500 cash, but the sale was not recorded until 2016. There were no other errors during 2015 or 2016 and no corrections have been made for any of the errors. Ignore income tax considerations.

-What is the total net effect of the errors on Langley's 2015 net income?

(Multiple Choice)

5.0/5 (40)

Which of the following should be reported as a prior period adjustment?

(Short Answer)

4.8/5 (35)

Use the following information for questions 53 and 54.

Swift Company purchased a machine on January 1, 2012, for $600,000. At the date of acquisition, the machine had an estimated useful life of six years with no salvage. The machine is being depreciated on a straight-line basis. On January 1, 2015, Swift determined, as a result of additional information, that the machine had an estimated useful life of eight years from the date of acquisition with no salvage. An accounting change was made in 2015 to reflect this additional information.

-What is the amount of depreciation expense on this machine that should be charged in Swift's income statement for the year ended December 31, 2015?

(Multiple Choice)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)