Exam 22: Accounting Changes and Error Analysis

Exam 1: Financial Accounting and Accounting Standards103 Questions

Exam 2: Conceptual Framework for Financial Reporting155 Questions

Exam 3: The Accounting Information System144 Questions

Exam 4: Income Statement and Related Information139 Questions

Exam 5: Balance Sheet and Statement of Cash Flows127 Questions

Exam 6: Accounting and the Time Value of Money152 Questions

Exam 7: Cash and Receivables173 Questions

Exam 8: Valuation of Inventories: a Cost-Basis Approach173 Questions

Exam 9: Inventories: Additional Valuation Issues168 Questions

Exam 10: Acquisition and Disposition of Property, Plant, and Equipment170 Questions

Exam 11: Depreciation, Impairments, and Depletion156 Questions

Exam 12: Intangible Assets171 Questions

Exam 13: Current Liabilities and Contingencies170 Questions

Exam 14: Long-Term Liabilities140 Questions

Exam 15: Stockholders Equity155 Questions

Exam 16: Dilutive Securities and Earnings Per Share160 Questions

Exam 17: Investments141 Questions

Exam 18: Revenue Recognition145 Questions

Exam 19: Accounting for Income Taxes127 Questions

Exam 20: Accounting for Pensions and Postretirement Benefits137 Questions

Exam 21: Accounting for Leases128 Questions

Exam 22: Accounting Changes and Error Analysis103 Questions

Exam 23: Statement of Cash Flows143 Questions

Exam 24: Full Disclosure in Financial Reporting108 Questions

Exam 25: Appendix89 Questions

Select questions type

Use the following information for questions 57 through 59.

Langley Company's December 31 year-end financial statements contained the following errors:  An insurance premium of $54,000 was prepaid in 2014 covering the years 2014, 2015, and 2016. The prepayment was recorded with a debit to insurance expense. In addition, on December 31, 2015, fully depreciated machinery was sold for $28,500 cash, but the sale was not recorded until 2016. There were no other errors during 2015 or 2016 and no corrections have been made for any of the errors. Ignore income tax considerations.

-What is the total effect of the errors on the balance of Langley's retained earnings at December 31, 2015?

An insurance premium of $54,000 was prepaid in 2014 covering the years 2014, 2015, and 2016. The prepayment was recorded with a debit to insurance expense. In addition, on December 31, 2015, fully depreciated machinery was sold for $28,500 cash, but the sale was not recorded until 2016. There were no other errors during 2015 or 2016 and no corrections have been made for any of the errors. Ignore income tax considerations.

-What is the total effect of the errors on the balance of Langley's retained earnings at December 31, 2015?

(Multiple Choice)

4.7/5  (39)

(39)

Which of the following is accounted for as a change in accounting principle?

(Multiple Choice)

4.8/5 (25)

On January 1, 2012, Knapp Corporation acquired machinery at a cost of $750,000. Knapp adopted the double-declining balance method of depreciation for this machinery and had been recording depreciation over an estimated useful life of ten years, with no residual value. At the beginning of 2015, a decision was made to change to the straight-line method of depreciation for the machinery. The depreciation expense for 2015 would be

(Multiple Choice)

4.8/5 (37)

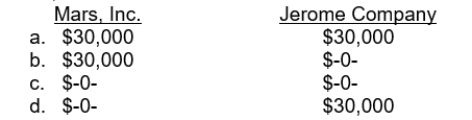

Mars, Inc. follows IFRS for its external financial reporting, while Jerome Company uses U.S. GAAP for its external financial reporting. During the year ended December 31, 2015, both companies changed from using the completed-contract method of revenue recognition for long-term construction contracts to the percentage-of-completion method. Both companies experienced an indirect effect, related to increased profit-sharing payments in 2015, of $30,000. As a result of this change, how much expense related to the profit-sharing payment must be recognized by each company on the income statement for the year ended December 31, 2015?

(Short Answer)

4.9/5 (26)

During 2015, a construction company changed from the completed-contract method to the percentage-of-completion method for accounting purposes but not for tax purposes. Gross profit figures under both methods for the past three years appear below:  Assuming an income tax rate of 40% for all years, the affect of this accounting change on prior periods should be reported by a credit of

Assuming an income tax rate of 40% for all years, the affect of this accounting change on prior periods should be reported by a credit of

(Multiple Choice)

4.8/5 (38)

For counterbalancing errors, restatement of comparative financial statements is necessary even if a correcting entry is not required.

(True/False)

4.9/5 (44)

Show how the following independent errors will affect net income on the Income Statement and the stockholders' equity section of the Balance Sheet using the symbol + (plus) for overstated, - (minus) for understated, and 0 (zero) for no effect.  1. Ending inventory in 2014 overstated."2. Failed to accrue 2014 interestrevenue."3. A capital expenditure for factory equipment (useful life, 5 years) was erroneously charged to Maintenance Expense in 2014.

1. Ending inventory in 2014 overstated."2. Failed to accrue 2014 interestrevenue."3. A capital expenditure for factory equipment (useful life, 5 years) was erroneously charged to Maintenance Expense in 2014.  4. Failed to count office supplies on hand at 12/31/14. Cash expenditures have been charged to Supplies Expense during the year 2014.5. Failed to accrue 2014 wages.6. Ending inventory in 2014 understated."7. Overstated 2014 depreciationexpense; 2015 expense correct."

4. Failed to count office supplies on hand at 12/31/14. Cash expenditures have been charged to Supplies Expense during the year 2014.5. Failed to accrue 2014 wages.6. Ending inventory in 2014 understated."7. Overstated 2014 depreciationexpense; 2015 expense correct."

(Essay)

4.9/5 (36)

Use the following information for questions 47 and 48.

On January 1, 2012, Nobel Corporation acquired machinery at a cost of $1,200,000. Nobel adopted the straight-line method of depreciation for this machine and had been recording depreciation over an estimated life of ten years, with no residual value. At the beginning of 2015, a decision was made to change to the double-declining balance method of depreciation for this machine.

-The amount that Nobel should record as depreciation expense for 2015 is

(Multiple Choice)

5.0/5 (35)

Use the following information for questions 66 and 67.

Ernst Company purchased equipment that cost $2,250,000 on January 1, 2014. The entire cost was recorded as an expense. The equipment had a nine-year life and a $90,000 residual value. Ernst uses the straight-line method to account for depreciation expense. The error was discovered on December 10, 2016. Ernst is subject to a 40% tax rate.

-Ernst's net income for the year ended December 31, 2014, was understated by

(Multiple Choice)

4.8/5 (39)

If, at the end of a period, a company erroneously excluded some goods from its ending inventory and also erroneously did not record the purchase of these goods in its accounting records, these errors would cause

(Multiple Choice)

4.8/5 (34)

Ben, Inc. follows U.S. GAAP for its external financial reporting. Ben, Inc. owns 25% of the outstanding stock of Black, Inc. and accordingly uses the equity method to account for its investment. Which of the following is true regarding Ben, Inc.'s policies related to Black, Inc.?

(Multiple Choice)

4.9/5 (33)

Use the following information for questions 55 and 56.

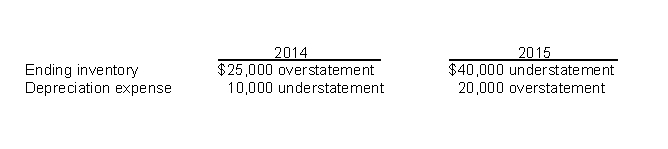

Armstrong Inc. is a calendar-year corporation. Its financial statements for the years ended 12/31/14 and 12/31/15 contained the following errors:  -Assume that no correcting entries were made at 12/31/14, or 12/31/15. Ignoring income taxes, by how much will retained earnings at 12/31/15 be overstated or understated?

-Assume that no correcting entries were made at 12/31/14, or 12/31/15. Ignoring income taxes, by how much will retained earnings at 12/31/15 be overstated or understated?

(Multiple Choice)

4.8/5 (37)

The controller for Haley Corporation is concerned about certain business transactions that the company experienced during 2015. The controller, after discussing these matters with various individuals, has come to you for advice. The transactions at issue are presented below."1. The company has decided to switch from the direct write-off method in accounting for bad debt expense to the percentage-of-sales approach. Assume that Haley Corporation has recognized bad debt expense as the receivables have actually become uncollectible in the following way:  The controller estimates that an additional $65,400 will be charged off in 2016: $11,400 applicable to 2014 sales and $54,000 to 2015 sales."2. Inventory has been shipped on consignment. These transactions have been recorded as ordinary sales and billed as such on account. At December 31, 2015, inventory billed and in the hands of consignees amounted to $425,000. The percentage markup on selling price is 20%. Assume that consigned inventory is sold the following year. The company uses the perpetual inventory system."3. During the current year, the company sold $600,000 of goods on the installment basis. The cost of sales associated with these goods sold is $450,000. The company inadvertently handled these sales and related costs as part of the regular sales transactions. Cash of $172,000, including a down payment of $60,000, was collected on these installment sales during the current year. Due to questionable collectibility, the installment-sales method was considered appropriate.

Instructions

(a) Assume that Haley Corporation reported net income of $1,200,000 for 2015. Present a schedule showing the corrected net income after reviewing the above transactions.

(b) Prepare the journal entries necessary at December 31, 2015, assuming that the books have been closed."

The controller estimates that an additional $65,400 will be charged off in 2016: $11,400 applicable to 2014 sales and $54,000 to 2015 sales."2. Inventory has been shipped on consignment. These transactions have been recorded as ordinary sales and billed as such on account. At December 31, 2015, inventory billed and in the hands of consignees amounted to $425,000. The percentage markup on selling price is 20%. Assume that consigned inventory is sold the following year. The company uses the perpetual inventory system."3. During the current year, the company sold $600,000 of goods on the installment basis. The cost of sales associated with these goods sold is $450,000. The company inadvertently handled these sales and related costs as part of the regular sales transactions. Cash of $172,000, including a down payment of $60,000, was collected on these installment sales during the current year. Due to questionable collectibility, the installment-sales method was considered appropriate.

Instructions

(a) Assume that Haley Corporation reported net income of $1,200,000 for 2015. Present a schedule showing the corrected net income after reviewing the above transactions.

(b) Prepare the journal entries necessary at December 31, 2015, assuming that the books have been closed."

(Essay)

4.8/5 (39)

Use the following information for questions 61 through 63.

Bishop Co. began operations on January 1, 2014. Financial statements for 2014 and 2015 con- tained the following errors:  In addition, on December 31, 2015 fully depreciated equipment was sold for $28,800, but the sale was not recorded until 2016. No corrections have been made for any of the errors. Ignore income tax considerations.

-The total effect of the errors on the balance of Bishop's retained earnings at December 31, 2015 is understated by

In addition, on December 31, 2015 fully depreciated equipment was sold for $28,800, but the sale was not recorded until 2016. No corrections have been made for any of the errors. Ignore income tax considerations.

-The total effect of the errors on the balance of Bishop's retained earnings at December 31, 2015 is understated by

(Multiple Choice)

4.9/5 (40)

Accounting errors include changes in estimates that occur because a company acquires more experience, or as it obtains additional information.

(True/False)

4.7/5 (33)

Use the following information for questions 57 through 59.

Langley Company's December 31 year-end financial statements contained the following errors: An insurance premium of $54,000 was prepaid in 2014 covering the years 2014, 2015, and 2016. The prepayment was recorded with a debit to insurance expense. In addition, on December 31, 2015, fully depreciated machinery was sold for $28,500 cash, but the sale was not recorded until 2016. There were no other errors during 2015 or 2016 and no corrections have been made for any of the errors. Ignore income tax considerations.

-What is the total net effect of the errors on the amount of Langley's working capital at December 31, 2015?

(Multiple Choice)

5.0/5 (35)

In 2015, Fischer Corporation changed its method of inventory pricing from LIFO to FIFO. Net income computed on a LIFO as compared to a FIFO basis for the four years involved is: (Ignore income taxes.)  Instructions

(a) Indicate the net income that would be shown on comparative financial statements issued at 12/31/15 for each of the four years, assuming that the company changed to the FIFO method in 2015.

(b) Assume that the company had switched from the average cost method to the FIFO method with net income on an average cost basis for the four years as follows: 2012, $80,400; 2013, $86,120; 2014, $90,300; and 2015, $93,600. Indicate the net income that would be shown on comparative financial statements issued at 12/31/15 for each of the four years under these conditions.

(c) Assuming that the company switched from the FIFO to the LIFO method, what would be the net income reported on comparative financial statements issued at 12/31/15 for 2012, 2013, and 2014?

Instructions

(a) Indicate the net income that would be shown on comparative financial statements issued at 12/31/15 for each of the four years, assuming that the company changed to the FIFO method in 2015.

(b) Assume that the company had switched from the average cost method to the FIFO method with net income on an average cost basis for the four years as follows: 2012, $80,400; 2013, $86,120; 2014, $90,300; and 2015, $93,600. Indicate the net income that would be shown on comparative financial statements issued at 12/31/15 for each of the four years under these conditions.

(c) Assuming that the company switched from the FIFO to the LIFO method, what would be the net income reported on comparative financial statements issued at 12/31/15 for 2012, 2013, and 2014?

(Essay)

4.8/5 (43)

Black, Inc. is a calendar-year corporation whose financial statements for 2014 and 2015 included errors as follows:  Assume that purchases were recorded correctly and that no correcting entries were made at December 31, 2014, or at December 31, 2015. Ignoring income taxes, by how much should Black's retained earnings be retroactively adjusted at January 1, 2016?

Assume that purchases were recorded correctly and that no correcting entries were made at December 31, 2014, or at December 31, 2015. Ignoring income taxes, by how much should Black's retained earnings be retroactively adjusted at January 1, 2016?

(Multiple Choice)

4.8/5 (39)

One of the disclosure requirements for a change in accounting principle is to show the cumulative effect of the change on retained earnings as of the beginning of the earliest period presented.

(True/False)

4.7/5 (38)

For each of the following items, indicate the type of accounting change and how each is recognized in the accounting records in the current year.(a) Change from straight-line method of depreciation to sum-of-the-years'-digits(b) Change from the cash basis to accrual basis of accounting(c) Change from FIFO to LIFO method for inventory valuation purposes (retrospective application impractical)(d) Change from presentation of statements of individual companies to presentation of consolidated statements(e) Change due to failure to record depreciation in a previous period(f) Change in the realizability of certain receivables(g) Change from LIFO to FIFO method for inventory valuation purposes

(Essay)

4.9/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)