Exam 3: Where Prices Come From: the Interaction of Demand and Supply

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

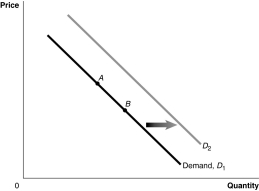

Figure 3-1  -Refer to Figure 3-1. An increase in the expected future price of the product would be represented by a movement from

-Refer to Figure 3-1. An increase in the expected future price of the product would be represented by a movement from

(Multiple Choice)

4.8/5  (30)

(30)

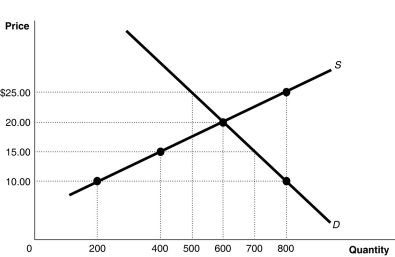

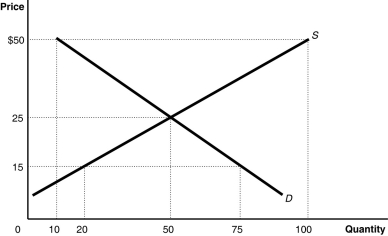

Figure 3-4  -Refer to Figure 3-4. At a price of $10, how many units will be sold?

-Refer to Figure 3-4. At a price of $10, how many units will be sold?

(Multiple Choice)

4.8/5 (36)

What would happen in the market for knee replacement surgery if insurance companies started to cover a smaller portion of the cost of the surgery?

(Multiple Choice)

4.7/5 (33)

Table 3-2

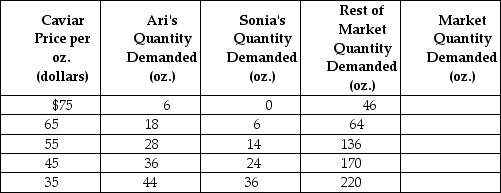

-Refer to Table 3-2. The table above shows the demand schedules for caviar of two individuals (Ari and Sonia) and the rest of the market. If the price of caviar rises from $65 to $75, the market quantity demanded would

-Refer to Table 3-2. The table above shows the demand schedules for caviar of two individuals (Ari and Sonia) and the rest of the market. If the price of caviar rises from $65 to $75, the market quantity demanded would

(Multiple Choice)

4.9/5 (44)

The demand by all the consumers of a given good or service is the ________ for the good or service.

(Multiple Choice)

4.9/5 (37)

Figure 3-8  -Blu-ray players were introduced to the market in 2006, and new technology has allowed for the cost of manufacturing the players to decline significantly since the initial introduction. How did this change in technology affect the market for Blu-ray players?

-Blu-ray players were introduced to the market in 2006, and new technology has allowed for the cost of manufacturing the players to decline significantly since the initial introduction. How did this change in technology affect the market for Blu-ray players?

(Multiple Choice)

4.9/5 (35)

If a decrease in income leads to in a decrease in the demand for ice cream, then ice cream is

(Multiple Choice)

5.0/5 (35)

If, in response to an increase in the price of chocolate the quantity of chocolate demanded decreases, economists would describe this as

(Multiple Choice)

4.8/5 (26)

"Because Coke and Pepsi are substitutes, a decrease in the price of Pepsi will cause the demand for Coke to decrease. This initial shift in demand for Coke results in a lower price for Coke; this lower price will cause the demand curve for Coke to shift to the left." Which of the following correctly comments on this statement?

(Multiple Choice)

4.8/5 (34)

If consumers believe the price of iPads will decrease in the future, this will cause the demand for iPads to decrease now.

(True/False)

4.7/5 (27)

In July, market analysts predict that the price of gold will rise in August. What happens in the gold market in July, holding everything else constant?

(Multiple Choice)

4.9/5 (33)

If the price of gasoline increases, what will be the impact in the market for public transportation?

(Multiple Choice)

4.9/5 (33)

If tablet computers are considered substitutes for e-readers, the decline in the price of e-readers would, all else equal,

(Multiple Choice)

4.8/5 (40)

What would happen in the market for knee replacement surgery if insurance companies started to cover a smaller portion of the cost of the surgery, and fewer doctors decide to enter the field of joint replacement surgery?

(Multiple Choice)

4.9/5 (40)

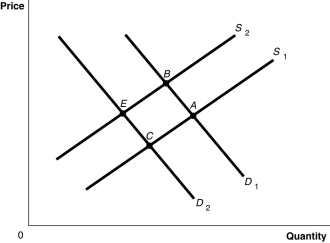

Figure 3-6  -Refer to Figure 3-6. The figure above represents the market for coffee grinders. Assume that the market price is $21. Which of the following statements is true?

-Refer to Figure 3-6. The figure above represents the market for coffee grinders. Assume that the market price is $21. Which of the following statements is true?

(Multiple Choice)

4.8/5 (33)

Which of the following would cause a decrease in the equilibrium price and decrease in the equilibrium quantity of papayas?

(Multiple Choice)

4.9/5 (34)

A surplus is defined as the situation that exists when the quantity of a good supplied is greater than the quantity demanded.

(True/False)

4.8/5 (35)

For each of the following pairs of products state which are complements, which are substitutes, and which are unrelated.

a. House plants and potato chips

b. Eyeglasses and contact lenses

c. Motorcycles and gasoline

d. Smartphone and smartphone apps

e. Red wine and white wine

(Essay)

4.9/5 (19)

Use the following supply schedule for cherries to draw a graph of the supply curve. Be sure to label the supply curve and each axis, and show each point on the supply curve.

(Essay)

4.7/5 (26)

If the population increases and input prices increase, the equilibrium price of a product will definitely increase.

(True/False)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)