Exam 3: Where Prices Come From: the Interaction of Demand and Supply

Exam 1: Economics: Foundations and Models444 Questions

Exam 2: Trade-Offs, Comparative Advantage, and the Market System498 Questions

Exam 3: Where Prices Come From: the Interaction of Demand and Supply475 Questions

Exam 4: Economic Efficiency, Government Price Setting, and Taxes419 Questions

Exam 5: Externalities, Environmental Policy, and Public Goods266 Questions

Exam 6: Elasticity: the Responsiveness of Demand and Supply295 Questions

Exam 7: The Economics of Health Care334 Questions

Exam 8: Firms, the Stock Market, and Corporate Governance278 Questions

Exam 9: Comparative Advantage and the Gains From International Trade379 Questions

Exam 10: Consumer Choice and Behavioral Economics302 Questions

Exam 11: Technology, Production, and Costs330 Questions

Exam 12: Firms in Perfectly Competitive Markets298 Questions

Exam 13: Monopolistic Competition: the Competitive Model in a More Realistic Setting276 Questions

Exam 14: Oligopoly: Firms in Less Competitive Markets262 Questions

Exam 15: Monopoly and Antitrust Policy271 Questions

Exam 16: Pricing Strategy263 Questions

Exam 17: The Markets for Labor and Other Factors of Production286 Questions

Exam 18: Public Choice, Taxes, and the Distribution of Income258 Questions

Exam 19: GDP: Measuring Total Production and Income266 Questions

Exam 20: Unemployment and Inflation292 Questions

Exam 21: Economic Growth, the Financial System, and Business Cycles257 Questions

Exam 22: Long-Run Economic Growth: Sources and Policies268 Questions

Exam 23: Aggregate Expenditure and Output in the Short Run306 Questions

Exam 24: Aggregate Demand and Aggregate Supply Analysis284 Questions

Exam 25: Money, Banks, and the Federal Reserve System280 Questions

Exam 26: Monetary Policy277 Questions

Exam 27: Fiscal Policy303 Questions

Exam 28: Inflation, Unemployment, and Federal Reserve Policy257 Questions

Exam 29: Macroeconomics in an Open Economy278 Questions

Exam 30: The International Financial System262 Questions

Select questions type

Suppose a positive technological change in the production of disease-resistant corn caused the price of corn to fall. Holding everything else constant, how would this affect the market for wheat (a substitute for corn)?

(Multiple Choice)

4.9/5  (33)

(33)

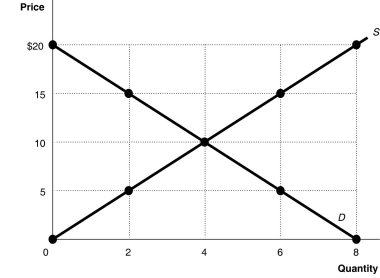

Figure 3-5  -Refer to Figure 3-5. At a price of $5, the quantity sold

-Refer to Figure 3-5. At a price of $5, the quantity sold

(Multiple Choice)

4.7/5 (23)

Figure 3-4  -Refer to Figure 3-4. At a price of $20, how many units will be supplied?

-Refer to Figure 3-4. At a price of $20, how many units will be supplied?

(Multiple Choice)

4.8/5 (26)

A shortage is defined as the situation that exists when the quantity of a good supplied is greater than the quantity demanded.

(True/False)

4.7/5 (29)

A change in which variable will change the market demand for a product?

(Multiple Choice)

4.9/5 (35)

Assume that the hourly price for the services of tarot card readers has risen and sales of these services have also risen. One can conclude that

(Multiple Choice)

4.7/5 (34)

Figure 3-1  -Refer to Figure 3-1. A decrease in the price of a complementary good would be represented by a movement from

-Refer to Figure 3-1. A decrease in the price of a complementary good would be represented by a movement from

(Multiple Choice)

4.7/5 (43)

If the quantity demanded for a product exceeds the quantity supplied, the market price will rise until

(Multiple Choice)

4.8/5 (29)

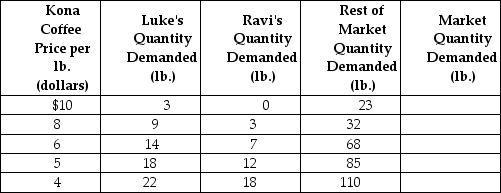

Table 3-3

-Refer to Table 3-3. The table above shows the demand schedules for Kona coffee of two individuals (Luke and Ravi) and the rest of the market. If the price of Kona coffee rises from $4 to $5, the market quantity demanded would

-Refer to Table 3-3. The table above shows the demand schedules for Kona coffee of two individuals (Luke and Ravi) and the rest of the market. If the price of Kona coffee rises from $4 to $5, the market quantity demanded would

(Multiple Choice)

4.7/5 (38)

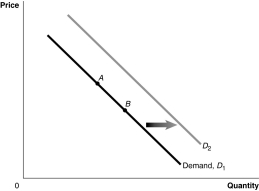

Figure 3-2  -Refer to Figure 3-2. A technological advancement would be represented by a movement from

-Refer to Figure 3-2. A technological advancement would be represented by a movement from

(Multiple Choice)

5.0/5 (35)

What is the difference between a demand schedule and a demand curve?

(Essay)

4.8/5 (26)

During the 1990s positive technological change in the production of chicken caused the price of chicken to fall. Holding everything else constant, how would this affect the market for pork (a substitute for chicken)?

(Multiple Choice)

4.9/5 (45)

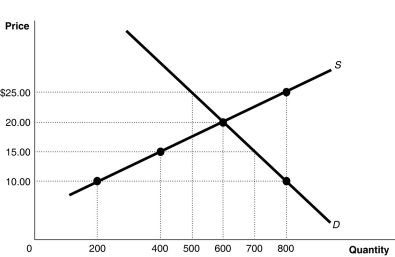

Figure 3-4

-Refer to Figure 3-4. At a price of $25, how many units will be supplied?

(Multiple Choice)

4.8/5 (32)

Shrimp is an increasingly popular part of the American diet. Louisiana shrimpers, who represent the bulk of the U.S. industry, were almost all put out of business by Hurricane Katrina. How did this affect the equilibrium price and quantity of shrimp?

(Essay)

4.8/5 (25)

All else equal, the decrease in consumer preference predicted by Apple for its iPhone 5 would be represented by a

(Multiple Choice)

4.8/5 (33)

Suppose a negative technological change in the production of disease-resistant wheat caused the price of wheat to rise. Holding everything else constant, how would this affect the market for corn (a substitute for wheat)?

(Multiple Choice)

4.8/5 (36)

If pilots and flight attendants agree to wage and benefit reductions in the wake of the financial difficulties in the airline industry, what impact would this have on the supply and demand in the market for airline service, assuming no other changes take place in this market?

(Essay)

4.9/5 (33)

If the demand for a product increases and the supply of the same product decreases, the equilibrium price will increase.

(True/False)

4.7/5 (37)

If the demand for a product decreases and the supply of the same product decreases, the equilibrium price will decrease.

(True/False)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)