Exam 7: Consumers, Producers, and the Efficiency of Markets

Exam 1: Ten Principles of Economics439 Questions

Exam 2: Thinking Like an Economist617 Questions

Exam 3: Interdependence and the Gains From Trade527 Questions

Exam 4: The Market Forces of Supply and Demand697 Questions

Exam 5: Elasticity and Its Application594 Questions

Exam 6: Supply, Demand, and Government Policies645 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets549 Questions

Exam 8: Application: the Costs of Taxation513 Questions

Exam 9: Application: International Trade492 Questions

Exam 10: Externalities524 Questions

Exam 11: Public Goods and Common Resources433 Questions

Exam 12: The Design of the Tax System549 Questions

Exam 13: The Costs of Production420 Questions

Exam 14: Firms in Competitive Markets543 Questions

Exam 15: Monopoly637 Questions

Exam 16: Monopolistic Competition580 Questions

Exam 17: Oligopoly488 Questions

Exam 18: The Markets for the Factors of Production564 Questions

Exam 19: Earnings and Discrimination490 Questions

Exam 20: Income Inequality and Poverty455 Questions

Exam 21: The Theory of Consumer Choice431 Questions

Exam 22: Frontiers of Microeconomics440 Questions

Exam 23: Measuring a Nations Income520 Questions

Exam 24: Measuring the Cost of Living529 Questions

Exam 25: Production and Growth505 Questions

Exam 26: Saving, Investment, and the Financial System564 Questions

Exam 27: The Basic Tools of Finance500 Questions

Exam 28: Unemployment678 Questions

Exam 29: The Monetary System515 Questions

Exam 30: Money Growth and Inflation481 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts522 Questions

Exam 32: A Macroeconomic Theory of the Open Economy475 Questions

Exam 33: Aggregate Demand and Aggregate Supply562 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand508 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment491 Questions

Exam 36: Six Debates Over Macroeconomic Policy372 Questions

Select questions type

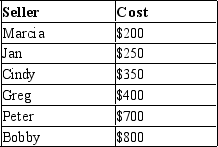

Table 7-13

The numbers reveal the opportunity costs of providing 10 piano lessons of equal quality.  -Refer to Table 7-13. You wish to purchase 10 piano lessons, so you take bids from each of the sellers. The bids are required to be rounded to the nearest dollar. You will not accept a bid below a seller's cost because you are concerned that the seller will not provide all 10 lessons. Your parents have given you $450 to spend on piano lessons. You believe that the sellers with higher opportunity costs offer higher quality lessons. You want the highest quality lessons that you can afford, but you can spend any remaining money on dinner with friends. From whom will you take lessons, and how much money will you spend?

-Refer to Table 7-13. You wish to purchase 10 piano lessons, so you take bids from each of the sellers. The bids are required to be rounded to the nearest dollar. You will not accept a bid below a seller's cost because you are concerned that the seller will not provide all 10 lessons. Your parents have given you $450 to spend on piano lessons. You believe that the sellers with higher opportunity costs offer higher quality lessons. You want the highest quality lessons that you can afford, but you can spend any remaining money on dinner with friends. From whom will you take lessons, and how much money will you spend?

(Multiple Choice)

4.8/5  (40)

(40)

The area below the demand curve and above the supply curve measures the producer surplus in a market.

(True/False)

4.9/5 (42)

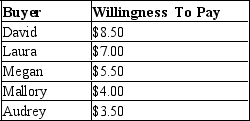

Table 7-2

This table refers to five possible buyers' willingness to pay for a case of Vanilla Coke.  -Refer to Table 7-2. If the price of Vanilla Coke is $6.90, who will purchase the good?

-Refer to Table 7-2. If the price of Vanilla Coke is $6.90, who will purchase the good?

(Multiple Choice)

4.8/5 (29)

We can say that the allocation of resources is efficient if

(Multiple Choice)

4.9/5 (32)

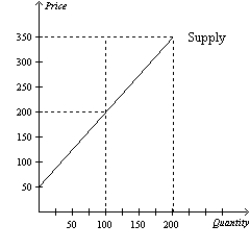

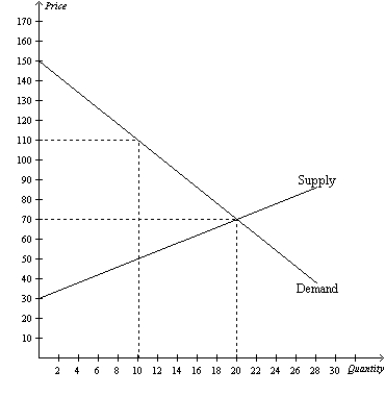

Figure 7-12  -Refer to Figure 7-12. If the equilibrium price is $350, what is the producer surplus?

-Refer to Figure 7-12. If the equilibrium price is $350, what is the producer surplus?

(Multiple Choice)

4.9/5 (37)

If producing a soccer ball costs Jake $5, and he sells it for $40, his producer surplus is $45.

(True/False)

4.8/5 (39)

Steak and chicken are substitutes. A sharp reduction in the supply of steak would

(Multiple Choice)

4.8/5 (39)

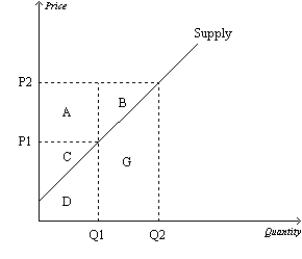

Figure 7-15  -Refer to Figure 7-15. When the price falls from P2 to P1, which of the following would not be true?

-Refer to Figure 7-15. When the price falls from P2 to P1, which of the following would not be true?

(Multiple Choice)

4.8/5 (39)

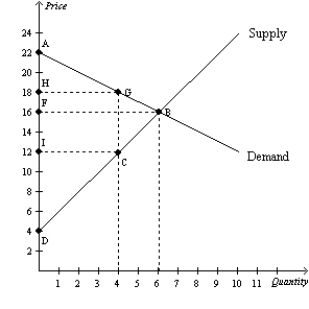

Figure 7-24  -Refer to Figure 7-24. If 6 units of the good are produced and sold, then

-Refer to Figure 7-24. If 6 units of the good are produced and sold, then

(Multiple Choice)

4.8/5 (42)

Table 7-13

The numbers reveal the opportunity costs of providing 10 piano lessons of equal quality.

-Refer to Table 7-13. The equilibrium market price for 10 piano lessons is $300. What is the total producer surplus in the market?

(Short Answer)

4.8/5 (33)

Figure 7-34  -Refer to Figure 7-34. Suppose the government imposes a price floor at $10 per unit in this market. With the price floor, how much is total consumer surplus?

-Refer to Figure 7-34. Suppose the government imposes a price floor at $10 per unit in this market. With the price floor, how much is total consumer surplus?

(Essay)

4.9/5 (37)

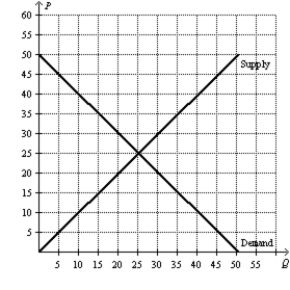

Figure 7-32  -Refer to Figure 7-32. At what price will total surplus be maximized in this market?

-Refer to Figure 7-32. At what price will total surplus be maximized in this market?

(Essay)

5.0/5 (42)

Figure 7-34

-Refer to Figure 7-34. Suppose there is initially a price ceiling set at $4 in this market. If the government removed the price ceiling, by how much would total producer surplus increase for those producers entering the market after the price ceiling is removed?

(Essay)

4.8/5 (43)

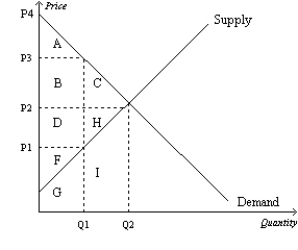

Figure 7-23  -Refer to Figure 7-23. At equilibrium, producer surplus is represented by the area

-Refer to Figure 7-23. At equilibrium, producer surplus is represented by the area

(Multiple Choice)

4.8/5 (36)

Suppose your own demand curve for tomatoes slopes downward. Suppose also that, for the last tomato you bought this week, you paid a price exactly equal to your willingness to pay. Then

(Multiple Choice)

4.8/5 (33)

Which of the following will cause no change in producer surplus?

(Multiple Choice)

4.8/5 (26)

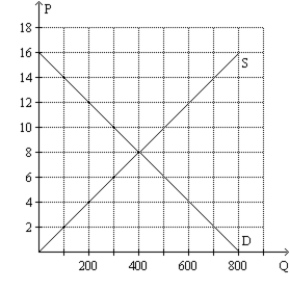

Figure 7-11  -Refer to Figure 7-11. If the supply curve is S and the demand curve shifts from D to D', what is the change in producer surplus?

-Refer to Figure 7-11. If the supply curve is S and the demand curve shifts from D to D', what is the change in producer surplus?

(Multiple Choice)

4.8/5 (29)

Table 7-6

For each of three potential buyers of apples, the table displays the willingness to pay for the first three apples of the day. Assume Xavier, Yadier, and Zavi are the only three buyers of apples, and only three apples can be supplied per day.  -Refer to Table 7-6. If the market price of an apple increases from $1.40 to $1.60, then consumer surplus

-Refer to Table 7-6. If the market price of an apple increases from $1.40 to $1.60, then consumer surplus

(Multiple Choice)

4.9/5 (34)

Figure 7-6  -Refer to Figure 7-6. At the equilibrium price, consumer surplus is

-Refer to Figure 7-6. At the equilibrium price, consumer surplus is

(Multiple Choice)

4.8/5 (47)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)