Exam 7: Consumers, Producers, and the Efficiency of Markets

Exam 1: Ten Principles of Economics439 Questions

Exam 2: Thinking Like an Economist617 Questions

Exam 3: Interdependence and the Gains From Trade527 Questions

Exam 4: The Market Forces of Supply and Demand697 Questions

Exam 5: Elasticity and Its Application594 Questions

Exam 6: Supply, Demand, and Government Policies645 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets549 Questions

Exam 8: Application: the Costs of Taxation513 Questions

Exam 9: Application: International Trade492 Questions

Exam 10: Externalities524 Questions

Exam 11: Public Goods and Common Resources433 Questions

Exam 12: The Design of the Tax System549 Questions

Exam 13: The Costs of Production420 Questions

Exam 14: Firms in Competitive Markets543 Questions

Exam 15: Monopoly637 Questions

Exam 16: Monopolistic Competition580 Questions

Exam 17: Oligopoly488 Questions

Exam 18: The Markets for the Factors of Production564 Questions

Exam 19: Earnings and Discrimination490 Questions

Exam 20: Income Inequality and Poverty455 Questions

Exam 21: The Theory of Consumer Choice431 Questions

Exam 22: Frontiers of Microeconomics440 Questions

Exam 23: Measuring a Nations Income520 Questions

Exam 24: Measuring the Cost of Living529 Questions

Exam 25: Production and Growth505 Questions

Exam 26: Saving, Investment, and the Financial System564 Questions

Exam 27: The Basic Tools of Finance500 Questions

Exam 28: Unemployment678 Questions

Exam 29: The Monetary System515 Questions

Exam 30: Money Growth and Inflation481 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts522 Questions

Exam 32: A Macroeconomic Theory of the Open Economy475 Questions

Exam 33: Aggregate Demand and Aggregate Supply562 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand508 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment491 Questions

Exam 36: Six Debates Over Macroeconomic Policy372 Questions

Select questions type

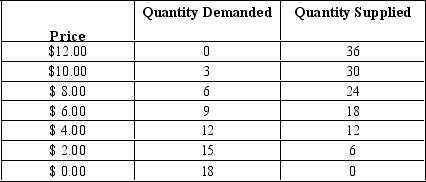

Table 7-17  -Refer to Table 7-17. Both the demand curve and the supply curve are straight lines. If the price is $4 but only 6 units are bought and sold, consumer surplus will be

-Refer to Table 7-17. Both the demand curve and the supply curve are straight lines. If the price is $4 but only 6 units are bought and sold, consumer surplus will be

(Multiple Choice)

5.0/5  (30)

(30)

Table 7-11

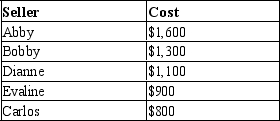

The following table represents the costs of five possible sellers.  -Refer to Table 7-11. Suppose each of the five sellers can supply at most one unit of the good. The market quantity supplied is exactly 2 if the price is

-Refer to Table 7-11. Suppose each of the five sellers can supply at most one unit of the good. The market quantity supplied is exactly 2 if the price is

(Multiple Choice)

4.8/5 (43)

Bill created a new software program he is willing to sell for $300. He sells his first copy and enjoys a producer surplus of $250. What is the price paid for the software?

(Multiple Choice)

4.7/5 (35)

According to many economists, government restrictions on ticket scalping do all of the following except

(Multiple Choice)

4.8/5 (52)

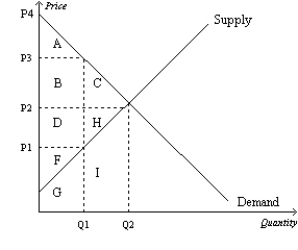

Figure 7-23  -Refer to Figure 7-23. If the price were P3, consumer surplus would be represented by the area

-Refer to Figure 7-23. If the price were P3, consumer surplus would be represented by the area

(Multiple Choice)

4.9/5 (38)

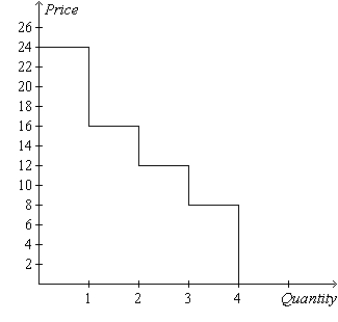

Figure 7-16  -Refer to Figure 7-16. Suppose the price of the good is $450. Then, on the first unit of the good that is sold, producer surplus is

-Refer to Figure 7-16. Suppose the price of the good is $450. Then, on the first unit of the good that is sold, producer surplus is

(Multiple Choice)

4.9/5 (42)

Which of the Ten Principles of Economics does welfare economics explain more fully?

(Multiple Choice)

4.9/5 (40)

Producer surplus is the amount a seller is paid minus the cost of production.

(True/False)

4.8/5 (32)

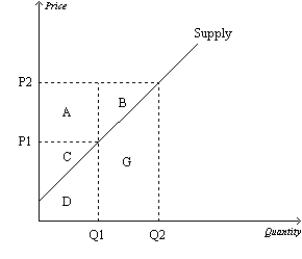

Figure 7-15  -Refer to Figure 7-15. When the price rises from P1 to P2, which area represents the increase in producer surplus to existing producers?

-Refer to Figure 7-15. When the price rises from P1 to P2, which area represents the increase in producer surplus to existing producers?

(Multiple Choice)

4.8/5 (33)

The study of how the allocation of resources affects economic well-being is called

(Multiple Choice)

4.8/5 (46)

Figure 7-5  -Refer to Figure 7-5. If the price of the good is $6, then consumer surplus is

-Refer to Figure 7-5. If the price of the good is $6, then consumer surplus is

(Multiple Choice)

4.9/5 (42)

Ticket scalping can increase total surplus in the market for tickets to sporting events.

(True/False)

4.7/5 (38)

At the equilibrium price of a good, the good will be sold by those sellers

(Multiple Choice)

4.8/5 (37)

Suppose Larry, Moe, and Curly are bidding in an auction for a mint-condition video of Charlie Chaplin's first movie. Each has in mind a maximum amount that he will bid. This maximum is called

(Multiple Choice)

4.9/5 (39)

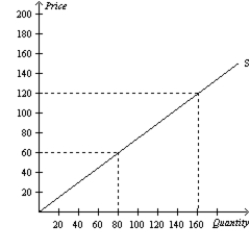

Figure 7-13  -Refer to Figure 7-13. If the equilibrium price rises from $60 to $120, what is the additional producer surplus to initial producers in the market?

-Refer to Figure 7-13. If the equilibrium price rises from $60 to $120, what is the additional producer surplus to initial producers in the market?

(Multiple Choice)

5.0/5 (40)

Suppose televisions are a normal good and buyers of televisions experience a decrease in income. As a result, consumer surplus in the television market

(Multiple Choice)

4.8/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)