Exam 7: Consumers, Producers, and the Efficiency of Markets

Exam 1: Ten Principles of Economics439 Questions

Exam 2: Thinking Like an Economist617 Questions

Exam 3: Interdependence and the Gains From Trade527 Questions

Exam 4: The Market Forces of Supply and Demand697 Questions

Exam 5: Elasticity and Its Application594 Questions

Exam 6: Supply, Demand, and Government Policies645 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets549 Questions

Exam 8: Application: the Costs of Taxation513 Questions

Exam 9: Application: International Trade492 Questions

Exam 10: Externalities524 Questions

Exam 11: Public Goods and Common Resources433 Questions

Exam 12: The Design of the Tax System549 Questions

Exam 13: The Costs of Production420 Questions

Exam 14: Firms in Competitive Markets543 Questions

Exam 15: Monopoly637 Questions

Exam 16: Monopolistic Competition580 Questions

Exam 17: Oligopoly488 Questions

Exam 18: The Markets for the Factors of Production564 Questions

Exam 19: Earnings and Discrimination490 Questions

Exam 20: Income Inequality and Poverty455 Questions

Exam 21: The Theory of Consumer Choice431 Questions

Exam 22: Frontiers of Microeconomics440 Questions

Exam 23: Measuring a Nations Income520 Questions

Exam 24: Measuring the Cost of Living529 Questions

Exam 25: Production and Growth505 Questions

Exam 26: Saving, Investment, and the Financial System564 Questions

Exam 27: The Basic Tools of Finance500 Questions

Exam 28: Unemployment678 Questions

Exam 29: The Monetary System515 Questions

Exam 30: Money Growth and Inflation481 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts522 Questions

Exam 32: A Macroeconomic Theory of the Open Economy475 Questions

Exam 33: Aggregate Demand and Aggregate Supply562 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand508 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment491 Questions

Exam 36: Six Debates Over Macroeconomic Policy372 Questions

Select questions type

At Nick's Bakery, the cost to make a cheese danish is $1.50 per danish. As a result of selling ten danishes, Nick experiences a producer surplus in the amount of $20. Nick must be selling his danishes for

(Multiple Choice)

4.8/5  (41)

(41)

If the cost of producing sofas decreases, then consumer surplus in the sofa market will

(Multiple Choice)

5.0/5 (30)

Scenario 7-2

Suppose market demand and market supply are given by the equations:  -Refer to Scenario 7-2. How much is total surplus at the equilibrium price in this market?

-Refer to Scenario 7-2. How much is total surplus at the equilibrium price in this market?

(Essay)

4.9/5 (31)

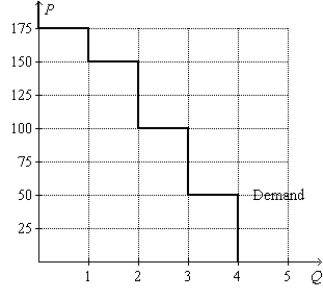

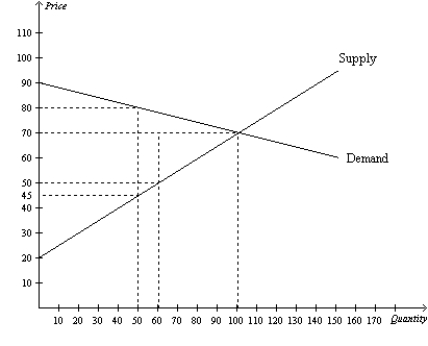

Figure 7-2  -Refer to Figure 7-2. If the price of the good is $80, then consumer surplus amounts to

-Refer to Figure 7-2. If the price of the good is $80, then consumer surplus amounts to

(Multiple Choice)

4.8/5 (34)

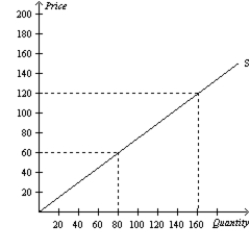

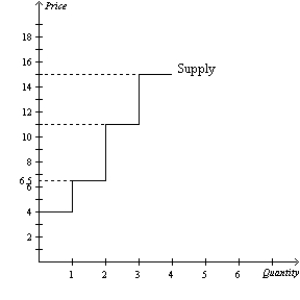

Figure 7-13  -Refer to Figure 7-13. If the equilibrium price is $60, what is the producer surplus?

-Refer to Figure 7-13. If the equilibrium price is $60, what is the producer surplus?

(Multiple Choice)

4.8/5 (39)

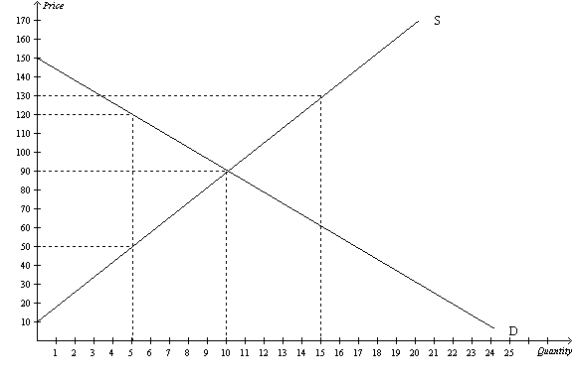

Figure 7-14  -Refer to Figure 7-14. If the market price increases to $130 due to an increase in demand, then producer surplus is

-Refer to Figure 7-14. If the market price increases to $130 due to an increase in demand, then producer surplus is

(Multiple Choice)

4.8/5 (37)

Kristi and Rebecca sell lemonade on the corner. It costs them 7 cents to make each cup. On a certain day, they sell 40 cups. Their producer surplus for that day amounts to $19.20. Kristi & Rebecca sold each cup for

(Multiple Choice)

4.8/5 (48)

Consumer surplus is the amount a buyer is willing to pay for a good minus the amount the buyer actually has to pay for it.

(True/False)

4.7/5 (35)

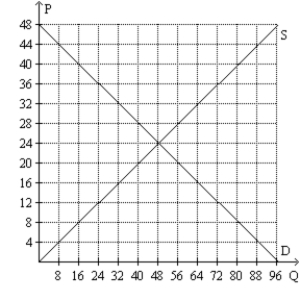

Figure 7-26  -Refer to Figure 7-26. At the equilibrium price, total surplus is

-Refer to Figure 7-26. At the equilibrium price, total surplus is

(Multiple Choice)

4.8/5 (40)

Table 7-9

During the last two days, Chad purchased a latte from two different stores. The table below shows Chad's willingness to pay on each day and his consumer surplus from each purchase.  -Refer to Table 7-9. The price that Chad paid for a latte on the second day is

-Refer to Table 7-9. The price that Chad paid for a latte on the second day is

(Multiple Choice)

4.9/5 (32)

All else equal, a decrease in demand will cause an increase in producer surplus.

(True/False)

4.8/5 (31)

Figure 7-9  -Refer to Figure 7-9. If producer surplus is $19, then the price of the good is

-Refer to Figure 7-9. If producer surplus is $19, then the price of the good is

(Multiple Choice)

4.8/5 (37)

Suppose there is an early freeze in California that reduces the size of the lemon crop. What happens to consumer surplus in the market for lemons?

(Multiple Choice)

4.8/5 (41)

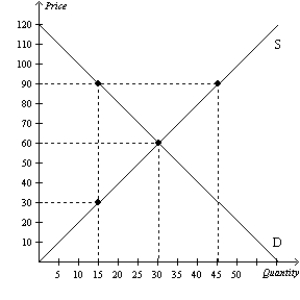

Figure 7-22  -Refer to Figure 7-22. Assume demand increases, which causes the equilibrium price to increase from $50 to $70. The increase in producer surplus to producers already in the market would be

-Refer to Figure 7-22. Assume demand increases, which causes the equilibrium price to increase from $50 to $70. The increase in producer surplus to producers already in the market would be

(Multiple Choice)

4.9/5 (46)

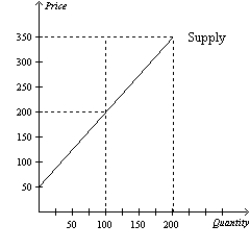

Figure 7-12  -Refer to Figure 7-12. If the equilibrium price rises from $200 to $350, what is the producer surplus to new producers

-Refer to Figure 7-12. If the equilibrium price rises from $200 to $350, what is the producer surplus to new producers

(Multiple Choice)

4.9/5 (44)

Figure 7-2

-Refer to Figure 7-2. If the price of the good is $100, then consumer surplus amounts to

(Multiple Choice)

4.8/5 (33)

Scenario 7-2

Suppose market demand and market supply are given by the equations:

-Refer to Scenario 7-2. Suppose a reduction in input prices shifts the market supply curve to  By how much does total consumer surplus increase as a result of this supply shift?

By how much does total consumer surplus increase as a result of this supply shift?

(Essay)

4.9/5 (42)

ABC Company incurs a cost of 50 cents to produce a dozen eggs, while XYZ Company incurs a cost of 70 cents to produce a dozen eggs. Which of the following price increases would cause both companies to experience an increase in producer surplus?

(Multiple Choice)

4.8/5 (32)

Figure 7-25  -Refer to Figure 7-25. Suppose the government imposes a price ceiling of $16 in this market. If the buyers with the highest willingness to pay purchase the good, then total surplus will be

-Refer to Figure 7-25. Suppose the government imposes a price ceiling of $16 in this market. If the buyers with the highest willingness to pay purchase the good, then total surplus will be

(Multiple Choice)

4.9/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)