Exam 7: Consumers, Producers, and the Efficiency of Markets

Exam 1: Ten Principles of Economics439 Questions

Exam 2: Thinking Like an Economist617 Questions

Exam 3: Interdependence and the Gains From Trade527 Questions

Exam 4: The Market Forces of Supply and Demand697 Questions

Exam 5: Elasticity and Its Application594 Questions

Exam 6: Supply, Demand, and Government Policies645 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets549 Questions

Exam 8: Application: the Costs of Taxation513 Questions

Exam 9: Application: International Trade492 Questions

Exam 10: Externalities524 Questions

Exam 11: Public Goods and Common Resources433 Questions

Exam 12: The Design of the Tax System549 Questions

Exam 13: The Costs of Production420 Questions

Exam 14: Firms in Competitive Markets543 Questions

Exam 15: Monopoly637 Questions

Exam 16: Monopolistic Competition580 Questions

Exam 17: Oligopoly488 Questions

Exam 18: The Markets for the Factors of Production564 Questions

Exam 19: Earnings and Discrimination490 Questions

Exam 20: Income Inequality and Poverty455 Questions

Exam 21: The Theory of Consumer Choice431 Questions

Exam 22: Frontiers of Microeconomics440 Questions

Exam 23: Measuring a Nations Income520 Questions

Exam 24: Measuring the Cost of Living529 Questions

Exam 25: Production and Growth505 Questions

Exam 26: Saving, Investment, and the Financial System564 Questions

Exam 27: The Basic Tools of Finance500 Questions

Exam 28: Unemployment678 Questions

Exam 29: The Monetary System515 Questions

Exam 30: Money Growth and Inflation481 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts522 Questions

Exam 32: A Macroeconomic Theory of the Open Economy475 Questions

Exam 33: Aggregate Demand and Aggregate Supply562 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand508 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment491 Questions

Exam 36: Six Debates Over Macroeconomic Policy372 Questions

Select questions type

David tunes pianos in his spare time for extra income. Buyers of his service are willing to pay $135 per tuning. One particular week, David is willing to tune the first piano for $115, the second piano for $125, the third piano for $140, and the fourth piano for $175. Assume David is rational in deciding how many pianos to tune. His producer surplus is

(Multiple Choice)

4.8/5  (44)

(44)

Figure 7-28  -Refer to Figure 7-28. At the quantity Q2, the marginal value to buyers

-Refer to Figure 7-28. At the quantity Q2, the marginal value to buyers

(Multiple Choice)

4.7/5 (33)

Table 7-14

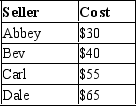

The only four producers in a market have the following costs:  -Refer to Table 7-14. If Abbey, Bev, and Carl sell the good, and the resulting producer surplus is $55 altogether, then the price must have been

-Refer to Table 7-14. If Abbey, Bev, and Carl sell the good, and the resulting producer surplus is $55 altogether, then the price must have been

(Multiple Choice)

4.8/5 (40)

The particular price that results in quantity supplied being equal to quantity demanded is the best price because it

(Multiple Choice)

4.9/5 (40)

Figure 7-27  -Refer to Figure 7-27. If the government mandated a price increase from P1 to a higher price, then

-Refer to Figure 7-27. If the government mandated a price increase from P1 to a higher price, then

(Multiple Choice)

4.7/5 (37)

Figure 7-31  -Refer to Figure 7-31. If the market equilibrium price rises from $25 to $35, how much is the increase in producer surplus to the producers supplying units at the initial $25 price?

-Refer to Figure 7-31. If the market equilibrium price rises from $25 to $35, how much is the increase in producer surplus to the producers supplying units at the initial $25 price?

(Essay)

4.7/5 (41)

Total surplus in a market can be measured as the area below the supply curve plus the area above the demand curve, up to the point of equilibrium.

(True/False)

4.8/5 (42)

Dallas buys strawberries, and he would be willing to pay more than he now pays. Suppose that Dallas has a change in his tastes such that he values strawberries more than before. If the market price is the same as before, then

(Multiple Choice)

4.8/5 (33)

Chuck would be willing to pay $20 to attend a dog show, but he buys a ticket for $15. Chuck values the dog show at

(Multiple Choice)

4.9/5 (38)

The cost of production plus producer surplus is the price a seller is paid.

(True/False)

4.8/5 (43)

When a buyer's willingness to pay for a good is equal to the price of the good, the

(Multiple Choice)

4.7/5 (44)

If the United States legally allowed for a market in transplant organs, it is estimated that one kidney would sell for at least $100,000.

(True/False)

4.8/5 (30)

Which of the following will cause a decrease in consumer surplus?

(Multiple Choice)

4.8/5 (39)

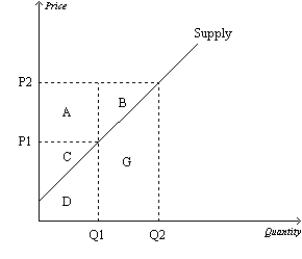

Figure 7-15  -Refer to Figure 7-15. When the price is P1, producer surplus is

-Refer to Figure 7-15. When the price is P1, producer surplus is

(Multiple Choice)

4.8/5 (39)

Figure 7-11  -Refer to Figure 7-11. If the supply curve is S and the demand curve shifts from D to D', what is the increase in producer surplus to existing producers?

-Refer to Figure 7-11. If the supply curve is S and the demand curve shifts from D to D', what is the increase in producer surplus to existing producers?

(Multiple Choice)

4.8/5 (38)

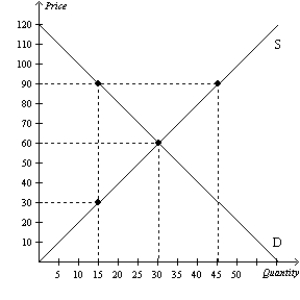

Figure 7-26  -Refer to Figure 7-26. If the government imposes a price floor of $90 in this market, then consumer surplus will be

-Refer to Figure 7-26. If the government imposes a price floor of $90 in this market, then consumer surplus will be

(Multiple Choice)

4.8/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)