Exam 7: Consumers, Producers, and the Efficiency of Markets

Exam 1: Ten Principles of Economics439 Questions

Exam 2: Thinking Like an Economist617 Questions

Exam 3: Interdependence and the Gains From Trade527 Questions

Exam 4: The Market Forces of Supply and Demand697 Questions

Exam 5: Elasticity and Its Application594 Questions

Exam 6: Supply, Demand, and Government Policies645 Questions

Exam 7: Consumers, Producers, and the Efficiency of Markets549 Questions

Exam 8: Application: the Costs of Taxation513 Questions

Exam 9: Application: International Trade492 Questions

Exam 10: Externalities524 Questions

Exam 11: Public Goods and Common Resources433 Questions

Exam 12: The Design of the Tax System549 Questions

Exam 13: The Costs of Production420 Questions

Exam 14: Firms in Competitive Markets543 Questions

Exam 15: Monopoly637 Questions

Exam 16: Monopolistic Competition580 Questions

Exam 17: Oligopoly488 Questions

Exam 18: The Markets for the Factors of Production564 Questions

Exam 19: Earnings and Discrimination490 Questions

Exam 20: Income Inequality and Poverty455 Questions

Exam 21: The Theory of Consumer Choice431 Questions

Exam 22: Frontiers of Microeconomics440 Questions

Exam 23: Measuring a Nations Income520 Questions

Exam 24: Measuring the Cost of Living529 Questions

Exam 25: Production and Growth505 Questions

Exam 26: Saving, Investment, and the Financial System564 Questions

Exam 27: The Basic Tools of Finance500 Questions

Exam 28: Unemployment678 Questions

Exam 29: The Monetary System515 Questions

Exam 30: Money Growth and Inflation481 Questions

Exam 31: Open-Economy Macroeconomics: Basic Concepts522 Questions

Exam 32: A Macroeconomic Theory of the Open Economy475 Questions

Exam 33: Aggregate Demand and Aggregate Supply562 Questions

Exam 34: The Influence of Monetary and Fiscal Policy on Aggregate Demand508 Questions

Exam 35: The Short-Run Trade-Off Between Inflation and Unemployment491 Questions

Exam 36: Six Debates Over Macroeconomic Policy372 Questions

Select questions type

Scenario 7-2

Suppose market demand and market supply are given by the equations:  -Refer to Scenario 7-2. Suppose a reduction in input prices shifts the market supply curve to

-Refer to Scenario 7-2. Suppose a reduction in input prices shifts the market supply curve to  By how much does total producer surplus increase as a result of this supply shift?

By how much does total producer surplus increase as a result of this supply shift?

(Essay)

4.7/5  (35)

(35)

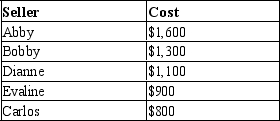

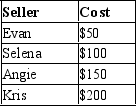

Table 7-11

The following table represents the costs of five possible sellers.  -Refer to Table 7-11. If the price is $1,000,

-Refer to Table 7-11. If the price is $1,000,

(Multiple Choice)

4.9/5 (35)

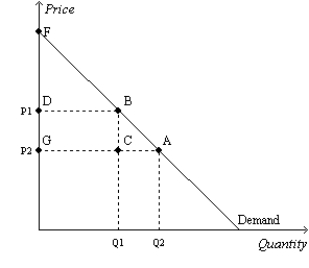

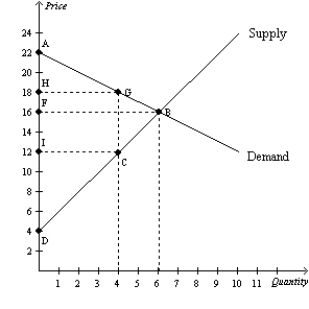

Figure 7-4  -Refer to Figure 7-4. Which area represents the increase in consumer surplus when the price falls from P1 to P2?

-Refer to Figure 7-4. Which area represents the increase in consumer surplus when the price falls from P1 to P2?

(Multiple Choice)

4.7/5 (35)

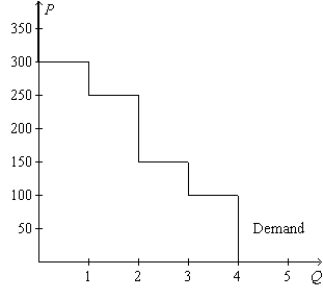

Figure 7-1  -Refer to Figure 7-1. If the price of the good is $150, then consumer surplus amounts to

-Refer to Figure 7-1. If the price of the good is $150, then consumer surplus amounts to

(Multiple Choice)

5.0/5 (37)

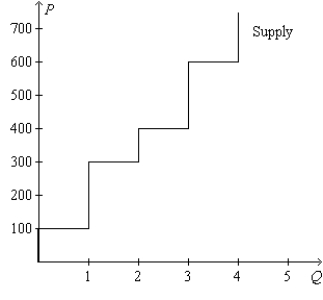

Figure 7-16  -Refer to Figure 7-16. If the price of the good is $600, then producer surplus amounts to

-Refer to Figure 7-16. If the price of the good is $600, then producer surplus amounts to

(Multiple Choice)

4.8/5 (39)

Figure 7-24  -Refer to Figure 7-24. At equilibrium, consumer surplus is measured by the area

-Refer to Figure 7-24. At equilibrium, consumer surplus is measured by the area

(Multiple Choice)

4.8/5 (37)

Table 7-12

The only four producers in a market have the following costs:  -Refer to Table 7-12. If the sellers bid against each other for the right to sell the good to a consumer, then the good will sell for

-Refer to Table 7-12. If the sellers bid against each other for the right to sell the good to a consumer, then the good will sell for

(Multiple Choice)

4.7/5 (30)

A drought in California destroys many red grapes. As a result of the drought, the consumer surplus in the market for red grapes

(Multiple Choice)

4.7/5 (44)

Denise values a stainless steel dishwasher for her new house at $500, but she succeeds in buying one for $350. Denise's consumer surplus is

(Multiple Choice)

4.8/5 (33)

If the United States changed its laws to allow for the legal sale of a kidney, which of the following is likely to occur?

(Multiple Choice)

4.7/5 (39)

If a market is in equilibrium, then it is impossible for a social planner to raise economic welfare by increasing or decreasing the quantity of the good.

(True/False)

4.7/5 (41)

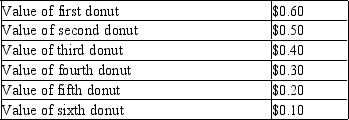

Tammy loves donuts. The table shown reflects the value Tammy places on each donut she eats:  a. Use this information to construct Tammy's demand curve for donuts.

b. If the price of donuts is $0.20, how many donuts will Tammy buy?

c. Show Tammy's consumer surplus on your graph. How much consumer surplus would she have at a price of $0.20?

d. If the price of donuts rose to $0.40, how many donuts would she purchase now? What would happen to Tammy's consumer surplus? Show this change on your graph.

a. Use this information to construct Tammy's demand curve for donuts.

b. If the price of donuts is $0.20, how many donuts will Tammy buy?

c. Show Tammy's consumer surplus on your graph. How much consumer surplus would she have at a price of $0.20?

d. If the price of donuts rose to $0.40, how many donuts would she purchase now? What would happen to Tammy's consumer surplus? Show this change on your graph.

(Essay)

4.8/5 (32)

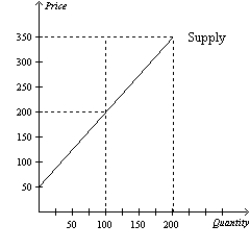

Figure 7-12  -Refer to Figure 7-12. If the equilibrium price is $200, what is the producer surplus?

-Refer to Figure 7-12. If the equilibrium price is $200, what is the producer surplus?

(Multiple Choice)

4.9/5 (45)

If a consumer places a value of $20 on a particular good and if the price of the good is $25, then the

(Multiple Choice)

4.8/5 (43)

Answer each of the following questions about supply and producer surplus.

a. What is producer surplus, and how is it measured?

b. What is the relationship between the cost to sellers and the supply curve?

c. Other things equal, what happens to producer surplus when the price of a good rises?

Illustrate your answer on a supply curve.

(Essay)

4.7/5 (27)

Market power and externalities are examples of market failures.

(True/False)

4.8/5 (39)

Suppose Raymond and Victoria attend a charity benefit and participate in a silent auction. Each has in mind a maximum amount that he or she will bid for an oil painting by a locally famous artist. This maximum is called

(Multiple Choice)

4.7/5 (33)

Suppose that Firms A and B each produce high-resolution computer monitors, but Firm A can do so at a lower cost. Cassie and David each want to purchase a high-resolution computer monitor, but David is willing to pay more than Cassie. If Firm B produces a monitor that David buys, then the market outcome illustrates which of the following principles?

(Multiple Choice)

4.8/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)