Exam 8: Profit Maximization and Competitive Supply

Exam 1: Preliminaries78 Questions

Exam 2: The Basics of Supply and Demand139 Questions

Exam 3: Consumer Behavior134 Questions

Exam 4: Individual and Market Demand131 Questions

Exam 5: Uncertainty and Consumer Behavior150 Questions

Exam 6: Production125 Questions

Exam 7: The Cost of Production178 Questions

Exam 8: Profit Maximization and Competitive Supply164 Questions

Exam 9: The Analysis of Competitive Markets183 Questions

Exam 10: Market Power: Monopoly and Monopsony158 Questions

Exam 11: Pricing With Market Power130 Questions

Exam 12: Monopolistic Competition and Oligopoly120 Questions

Exam 13: Game Theory and Competitive Strategy150 Questions

Exam 14: Markets for Factor Inputs134 Questions

Exam 15: Investment, Time, and Capital Markets153 Questions

Exam 16: General Equilibrium and Economic Efficiency126 Questions

Exam 17: Markets With Asymmetric Information133 Questions

Exam 18: Externalities and Public Goods131 Questions

Exam 19: Behavioral Economics101 Questions

Select questions type

The long-run supply curve in a constant-cost industry is linear and:

(Multiple Choice)

4.8/5  (35)

(35)

Figure 8.7.3

-Refer to Figure 8.7.3 above. As the firm makes its long-run adjustment, which must be true?

Figure 8.7.3

-Refer to Figure 8.7.3 above. As the firm makes its long-run adjustment, which must be true?

(Multiple Choice)

4.8/5 (44)

The long-run cost function for Jeremy's Jetski Rentals is:  The long-run marginal cost function is

The long-run marginal cost function is  If Jeremy can sell as many jetski rentals as he desires at $50, calculate his optimal output in the long run.

If Jeremy can sell as many jetski rentals as he desires at $50, calculate his optimal output in the long run.

(Essay)

4.7/5 (41)

Consider the following statements when answering this question: I. In the long run, if a firm wants to remain in a competitive industry, then it needs to own resources that are in limited supply.

II) In this competitive market our firm's long-run survival depends only on the efficiency of our production process.

(Multiple Choice)

4.9/5 (36)

At the profit-maximizing level of output, what is relationship between the total revenue (TR) and total cost (TC) curves?

(Multiple Choice)

4.8/5 (37)

In the long run, a firm's producer surplus is equal to the:

(Multiple Choice)

4.9/5 (45)

If the market price for a competitive firm's output doubles, then:

(Multiple Choice)

4.9/5 (39)

The shutdown decision can be restated in terms of producer surplus by saying that a firm should produce in the short run as long as:

(Multiple Choice)

4.7/5 (41)

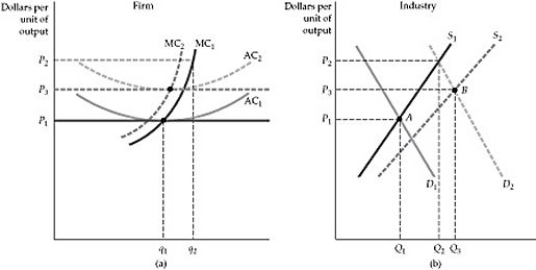

Figure 8.8.2

-Refer to Figure 8.8.2 above. Starting with the increase in demand, the cost and supply curves will shift, indicating that this is:

Figure 8.8.2

-Refer to Figure 8.8.2 above. Starting with the increase in demand, the cost and supply curves will shift, indicating that this is:

(Multiple Choice)

4.7/5 (32)

The authors note that the goal of maximizing the market value of the firm may be more appropriate than maximizing short-run profits because:

(Multiple Choice)

4.9/5 (43)

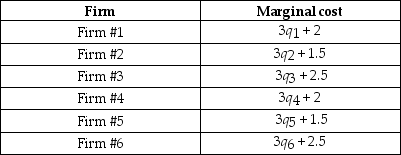

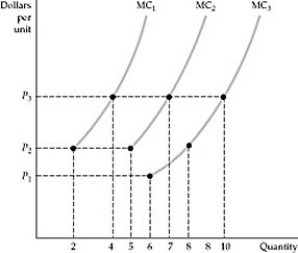

The marginal cost curves of six firms in an industry appear in the table below. If these firms behave competitively, determine the market supply curve. Calculate the elasticity of market supply at $5.

(Essay)

4.8/5 (31)

Consider the following statements when answering this question: I. In the long-run equilibrium of a perfectly competitive market, a firm's producer surplus equals the sum of the economic rents earned on its inputs to production.

II) In the long-run equilibrium of a perfectly competitive market, the amount of economic profit earned can differ across firms, but not the amount of producer surplus.

(Multiple Choice)

4.8/5 (36)

If managers do not choose to maximize profit, but pursue some other goal such as revenue maximization or growth,

(Multiple Choice)

4.9/5 (51)

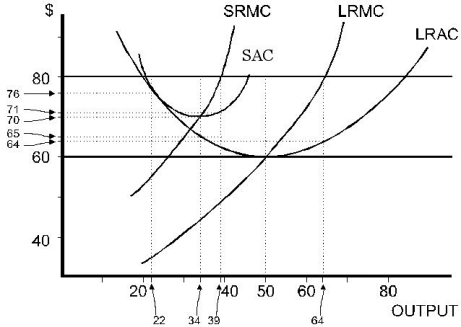

Figure 8.6.1

-Refer to Figure 8.6.1 above. The minimum variable cost of the firms in this competitive market is:

Figure 8.6.1

-Refer to Figure 8.6.1 above. The minimum variable cost of the firms in this competitive market is:

(Multiple Choice)

4.7/5 (35)

The market demand for a type of carpet known as KP-7 has been estimated as:

P = 40 - 0.25Q,

where P is price ($/yard) and Q is rate of sales (hundreds of yards per month). The market supply is expressed as:

P = 5.0 + 0.05Q.

A typical firm in this market has a total cost function given as:

C = 100 - 20.0q + 2.0q2.

a. Determine the equilibrium market output rate and price.

b. Determine the output rate for a typical firm.

c. Determine the rate of profit (or loss) earned by the typical firm.

(Essay)

5.0/5 (29)

Several years ago, Alcoa was effectively the sole seller of aluminum because the firm owned nearly all of the aluminum ore reserves in the world. This market was not perfectly competitive because this situation violated the:

(Multiple Choice)

4.7/5 (41)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)