Exam 8: Profit Maximization and Competitive Supply

Exam 1: Preliminaries78 Questions

Exam 2: The Basics of Supply and Demand139 Questions

Exam 3: Consumer Behavior134 Questions

Exam 4: Individual and Market Demand131 Questions

Exam 5: Uncertainty and Consumer Behavior150 Questions

Exam 6: Production125 Questions

Exam 7: The Cost of Production178 Questions

Exam 8: Profit Maximization and Competitive Supply164 Questions

Exam 9: The Analysis of Competitive Markets183 Questions

Exam 10: Market Power: Monopoly and Monopsony158 Questions

Exam 11: Pricing With Market Power130 Questions

Exam 12: Monopolistic Competition and Oligopoly120 Questions

Exam 13: Game Theory and Competitive Strategy150 Questions

Exam 14: Markets for Factor Inputs134 Questions

Exam 15: Investment, Time, and Capital Markets153 Questions

Exam 16: General Equilibrium and Economic Efficiency126 Questions

Exam 17: Markets With Asymmetric Information133 Questions

Exam 18: Externalities and Public Goods131 Questions

Exam 19: Behavioral Economics101 Questions

Select questions type

A firm's producer surplus equals its economic profit when:

(Multiple Choice)

4.7/5  (46)

(46)

The table below provides cost information for two firms in a competitive industry. Graph the supply curves of the firms individually and jointly. For these two firms, at any positive output level, marginal cost exceeds average variable cost.

(Essay)

4.9/5 (35)

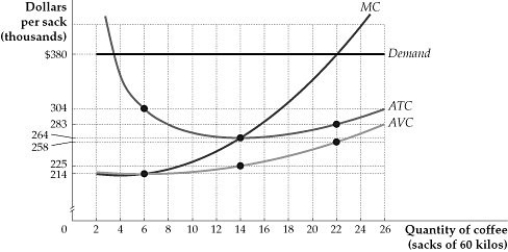

Figure 8.4.2

-Refer to Figure 8.4.2 above. How much is the profit lost when the farmer produces 6 sacks instead of 14 sacks?

Figure 8.4.2

-Refer to Figure 8.4.2 above. How much is the profit lost when the farmer produces 6 sacks instead of 14 sacks?

(Multiple Choice)

4.8/5 (36)

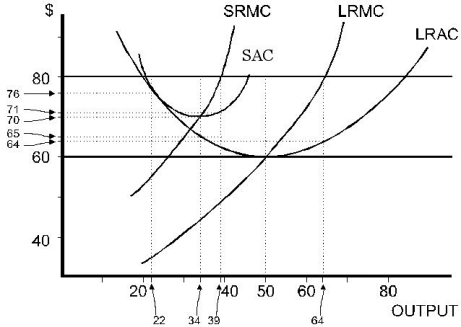

Figure 8.7.3

-Refer to Figure 8.7.3 above. At P = $80, the profit-maximizing output in the short run is:

Figure 8.7.3

-Refer to Figure 8.7.3 above. At P = $80, the profit-maximizing output in the short run is:

(Multiple Choice)

4.7/5 (42)

If a competitive firm's marginal costs always increase with output, then at the profit maximizing output level, producer surplus is:

(Multiple Choice)

4.9/5 (38)

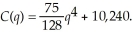

Homer's Boat Manufacturing cost function is:  The marginal cost function is:

The marginal cost function is:  If Homer can sell all the boats he produces for $1,200, what is his optimal output? Calculate Homer's profit or loss.

If Homer can sell all the boats he produces for $1,200, what is his optimal output? Calculate Homer's profit or loss.

(Essay)

4.7/5 (45)

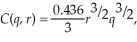

The squishy industry is competitive and the market price is $0.80. Apu's long-run cost function is:  where r is the price Apu pays to lease a squishy machine and q is squishy output. The long-run marginal cost curve is:

where r is the price Apu pays to lease a squishy machine and q is squishy output. The long-run marginal cost curve is:  What is Apu's optimal output if the price Apu pays to lease a squishy machine is $1.10? Suppose the lease price of squishy machines falls by $0.55. What happens to Apu's optimal output if the market price for a squishy remains at $0.80? Did profits increase for Apu when the lease rate of squishy machines fell?

What is Apu's optimal output if the price Apu pays to lease a squishy machine is $1.10? Suppose the lease price of squishy machines falls by $0.55. What happens to Apu's optimal output if the market price for a squishy remains at $0.80? Did profits increase for Apu when the lease rate of squishy machines fell?

(Essay)

4.9/5 (29)

Scenario 8.2:

Yachts are produced by a perfectly competitive industry in Dystopia. Industry output (Q) is currently 30,000 yachts per year. The government, in an attempt to raise revenue, places a $20,000 tax on each yacht. Demand is highly, but not perfectly, elastic.

-Refer to Scenario 8.2. The more elastic is demand for yachts,

(Multiple Choice)

4.9/5 (41)

Three hundred firms supply the market for paint. For fifty of the firms, their short-run average variable costs are minimized at $10 and short-run total costs are minimized at $15. For the remaining firms, the short-run average variable costs and short-run average total costs are minimized at $20 and $25, respectively. If each firm has a U-shaped marginal cost curve then the short-run market supply curve is:

(Multiple Choice)

4.9/5 (43)

Use the following statements to answer this question: I. Markets may be highly (but not perfectly) competitive even if there are a few sellers.

II) There is no simple indicator that tells us when markets are highly competitive.

(Multiple Choice)

4.9/5 (46)

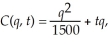

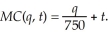

The manufacturing of paper products causes damage to a local river when the manufacturing plant produces more than 1,000 units in a period. To discourage the plant from producing more than 1,000 units, the local community is considering placing a tax on the plant. The long-run cost curve for the paper producing firm is:  where q is the number of units of paper produced and t is the per unit tax on paper production. The relevant marginal cost curve is:

where q is the number of units of paper produced and t is the per unit tax on paper production. The relevant marginal cost curve is:  If the manufacturing plant can sell all of its output for $2, what is the firm's optimal output if the tax is set at zero? What is the minimum tax rate necessary to ensure that the firm produces no more than 1,000 units? How much are the firm's profits reduced by the presence of a tax?

If the manufacturing plant can sell all of its output for $2, what is the firm's optimal output if the tax is set at zero? What is the minimum tax rate necessary to ensure that the firm produces no more than 1,000 units? How much are the firm's profits reduced by the presence of a tax?

(Essay)

4.8/5 (32)

In the short run, a perfectly competitive firm earning negative economic profit is:

(Multiple Choice)

4.7/5 (36)

Suppose we plot the total revenue curve with quantity on the horizontal axis and revenue on the vertical axis (as in Figure 8.1 in the book). Under price-taking behavior, the total revenue curve should be:

(Multiple Choice)

4.7/5 (31)

The textbook for your class was not produced in a perfectly competitive industry because:

(Multiple Choice)

4.9/5 (38)

Consider the following statements when answering this question: I. Increases in the demand for a good, which is produced by a competitive industry, will raise the short-run market price.

II) Increases in the demand for a good, which is produced by a competitive industry, will raise the long-run market price.

(Multiple Choice)

4.8/5 (34)

When the price faced by a competitive firm was $5, the firm produced nothing in the short run. However, when the price rose to $10, the firm produced 100 tons of output. From this we can infer that:

(Multiple Choice)

4.9/5 (37)

Bette's Breakfast, a perfectly competitive eatery, sells its "Breakfast Special" (the only item on the menu) for $5.00. The costs of waiters, cooks, power, food etc. average out to $3.95 per meal; the costs of the lease, insurance and other such expenses average out to $1.25 per meal. Bette should:

(Multiple Choice)

4.7/5 (36)

Short-run supply curves for perfectly competitive firms tend to be upward sloping because:

(Multiple Choice)

4.9/5 (39)

Consider a competitive market in which the market demand for the product is expressed as

P = 75 - 1.5Q,

and the supply of the product is expressed as

P = 25 + 0.50Q.

Price, P, is in dollars per unit sold, and Q represents rate of production and sales in hundreds of units per day. The typical firm in this market has a marginal cost of

MC = 2.5 + 10q.

a. Determine the equilibrium market price and rate of sales.

b. Determine the rate of sales of the typical firm, given your answer to part (a) above.

c. If the market demand were to increase to  what would the new price and rate of sales in the market be? What would the new rate of sales for the typical firm be?

d. If the original supply and demand represented a long-run equilibrium condition in the market, would the new equilibrium (c) represent a new long-run equilibrium for the typical firm? Explain.

what would the new price and rate of sales in the market be? What would the new rate of sales for the typical firm be?

d. If the original supply and demand represented a long-run equilibrium condition in the market, would the new equilibrium (c) represent a new long-run equilibrium for the typical firm? Explain.

(Essay)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)