Exam 8: Profit Maximization and Competitive Supply

Exam 1: Preliminaries78 Questions

Exam 2: The Basics of Supply and Demand139 Questions

Exam 3: Consumer Behavior134 Questions

Exam 4: Individual and Market Demand131 Questions

Exam 5: Uncertainty and Consumer Behavior150 Questions

Exam 6: Production125 Questions

Exam 7: The Cost of Production178 Questions

Exam 8: Profit Maximization and Competitive Supply164 Questions

Exam 9: The Analysis of Competitive Markets183 Questions

Exam 10: Market Power: Monopoly and Monopsony158 Questions

Exam 11: Pricing With Market Power130 Questions

Exam 12: Monopolistic Competition and Oligopoly120 Questions

Exam 13: Game Theory and Competitive Strategy150 Questions

Exam 14: Markets for Factor Inputs134 Questions

Exam 15: Investment, Time, and Capital Markets153 Questions

Exam 16: General Equilibrium and Economic Efficiency126 Questions

Exam 17: Markets With Asymmetric Information133 Questions

Exam 18: Externalities and Public Goods131 Questions

Exam 19: Behavioral Economics101 Questions

Select questions type

Which of the following statements identifies a key difference between condominiums and cooperative housing?

(Multiple Choice)

4.8/5  (40)

(40)

In a supply-and-demand graph, producer surplus can be pictured as the:

(Multiple Choice)

4.9/5 (36)

In the short run, a perfectly competitive profit maximizing firm that has not shut down:

(Multiple Choice)

4.7/5 (34)

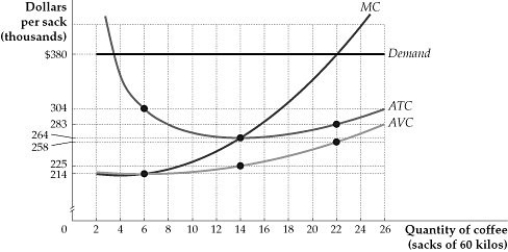

Figure 8.4.2

-Refer to Figure 8.4.2 above. The figure describes the cost and revenue structure of a perfectly competitive coffee farm, on a per-unit basis. What is the profit maximizing number of sacks when the price of coffee in the market is $380 dollars?

Figure 8.4.2

-Refer to Figure 8.4.2 above. The figure describes the cost and revenue structure of a perfectly competitive coffee farm, on a per-unit basis. What is the profit maximizing number of sacks when the price of coffee in the market is $380 dollars?

(Multiple Choice)

4.8/5 (31)

Suppose a plant manager ignores some implicit marginal costs of production so that the perceived MC curve is below the actual MC curve. What is the likely outcome from this error?

(Multiple Choice)

4.9/5 (31)

Suppose your firm has a U-shaped average variable cost curve and operates in a perfectly competitive market. If you produce where the product price (marginal revenue) equals average variable cost (on the upward sloping portion of the AVC curve), then your output will:

(Multiple Choice)

5.0/5 (45)

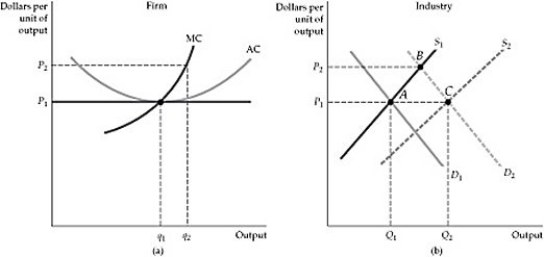

Figure 8.8.1

-Refer to Figure 8.8.1 above. After the increase in demand, from D1 to D2 in panel (b), and being this a constant-cost industry, what is likely to happen in the market?

Figure 8.8.1

-Refer to Figure 8.8.1 above. After the increase in demand, from D1 to D2 in panel (b), and being this a constant-cost industry, what is likely to happen in the market?

(Multiple Choice)

4.9/5 (45)

The market for wheat consists of 500 identical firms, each with the total and marginal cost functions shown:

TC = 90,000 + 0.00001Q2

MC = 0.00002Q,

where Q is measured in bushels per year. The market demand curve for wheat is Q = 90,000,000 20,000,000P, where Q is again measured in bushels and P is the price per bushel.

a. Determine the short-run equilibrium price and quantity that would exist in the market.

b. Calculate the profit maximizing quantity for the individual firm. Calculate the firm's short-run profit (loss) at that quantity.

c. Assume that the short-run profit or loss is representative of the current long-run prospects in this market. You may further assume that there are no barriers to entry or exit in the market. Describe the expected long-run response to the conditions described in part b. (The TC function for the firm may be regarded as an economic cost function that captures all implicit and explicit costs.)

(Essay)

4.7/5 (33)

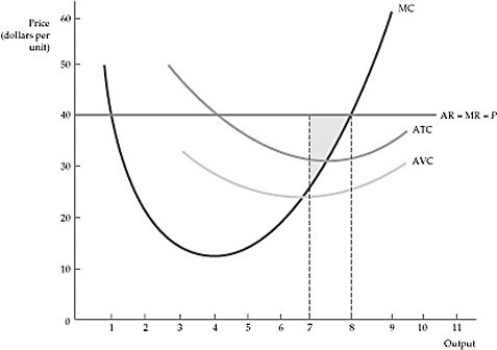

Figure 8.4.1

-Refer to Figure 8.4.1 above. The shaded area in the graph shows:

Figure 8.4.1

-Refer to Figure 8.4.1 above. The shaded area in the graph shows:

(Multiple Choice)

4.8/5 (37)

The market demand for a type of carpet known as KS-12 has been estimated as

P = 75 - 1.5Q,

where P is price ($/yard), and Q is output per time period (thousands of yards per month). The market supply is expressed as P = 25 + 0.50Q. A typical competitive firm that markets this type of carpet has a marginal cost of production of

MC = 2.5 + 10q.

a. Determine the market equilibrium price for this type of carpet. Also determine the production rate in the market.

b. Determine how much the typical firm will produce per week at the equilibrium price.

c. If all firms had the same cost structure, how many firms would compete at the equilibrium price computed in (a) above?

d. Determine the producer surplus the typical firm has under the conditions described above. (Hint: Note that the marginal cost function is linear.)

(Essay)

4.7/5 (35)

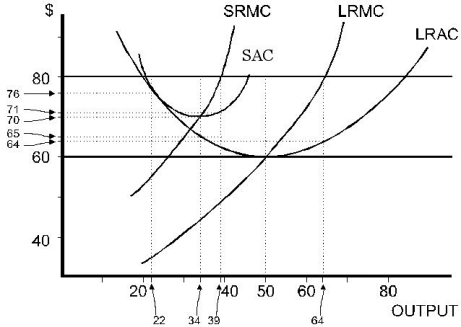

Figure 8.7.3

-Refer to Figure 8.7.3 above. As the competitive industry, not just the firm in question, moves toward long-run equilibrium, the firm will be forced to operate at what level of output?

Figure 8.7.3

-Refer to Figure 8.7.3 above. As the competitive industry, not just the firm in question, moves toward long-run equilibrium, the firm will be forced to operate at what level of output?

(Multiple Choice)

4.8/5 (35)

That Table 8.1 shows a short-run situation is evident from:

(Multiple Choice)

4.7/5 (46)

The demand for pizzas in the local market is given by:  There are 100 pizza firms currently in the market. The long-run cost function for each pizza firm is:

There are 100 pizza firms currently in the market. The long-run cost function for each pizza firm is:  where w is the wage rate pizza firms pay for a labor hour and q is the number of pizzas produced. The marginal cost function for each firm is:

where w is the wage rate pizza firms pay for a labor hour and q is the number of pizzas produced. The marginal cost function for each firm is:  If the current wage rate is $7 and the industry is competitive, calculate the optimal output of each firm given each firm produces the same level of output. Do you anticipate firms entering or exiting the pizza industry? Suppose that the wage rate increases to $8.40. Calculate optimal output for each of the 100 firms. Do you anticipate firms entering or exiting the pizza industry? What happens to the market output of pizzas with the higher wage rate? What happens to the market price for pizza?

If the current wage rate is $7 and the industry is competitive, calculate the optimal output of each firm given each firm produces the same level of output. Do you anticipate firms entering or exiting the pizza industry? Suppose that the wage rate increases to $8.40. Calculate optimal output for each of the 100 firms. Do you anticipate firms entering or exiting the pizza industry? What happens to the market output of pizzas with the higher wage rate? What happens to the market price for pizza?

(Essay)

4.8/5 (40)

The "perfect information" assumption of perfect competition includes all of the following except one. Which one?

(Multiple Choice)

4.9/5 (31)

Use the following statements to answer this question: I. The firm's decision to produce zero output when the price is less than the average variable cost of production is known as the shutdown rule.

II) The firm's supply decision is to generate zero output for all prices below the minimum AVC.

(Multiple Choice)

4.9/5 (43)

Figure 8.4.2

-Refer to Figure 8.4.2 above. When the coffee farmer maximizes profit, how much is his profit?

(Multiple Choice)

4.8/5 (45)

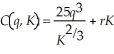

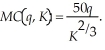

Laura's internet services has the following short-run cost curve:  where q is Laura's output level, K is the number of servers she leases and r is the lease rate of servers. Laura's short-run marginal cost function is:

where q is Laura's output level, K is the number of servers she leases and r is the lease rate of servers. Laura's short-run marginal cost function is:  Currently, Laura leases 8 servers, the lease rate of servers is $15, and Laura can sell all the output she produces for $500. Find Laura's short-run profit maximizing level of output. Calculate Laura's profits. If the lease rate of internet servers rise to $20, how does Laura's optimal output and profits change?

Currently, Laura leases 8 servers, the lease rate of servers is $15, and Laura can sell all the output she produces for $500. Find Laura's short-run profit maximizing level of output. Calculate Laura's profits. If the lease rate of internet servers rise to $20, how does Laura's optimal output and profits change?

(Essay)

4.8/5 (46)

The following table contains information for a price taking competitive firm. Complete the table and determine the profit maximizing level of output (round your answer to the nearest whole number).

Total Marginal Fixed Average Total Average Marginal

Output Cost Cost Cost Cost Revenue Revenue Revenue

0 25

1 35

2 30

3 45

4 185

5 57

6 120 240

(Essay)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)