Exam 16: Time-Series Forecasting

Exam 1: Defining and Collecting Data207 Questions

Exam 2: Organizing and Visualizing Variables213 Questions

Exam 3: Numerical Descriptive Measures167 Questions

Exam 4: Basic Probability171 Questions

Exam 5: Discrete Probability Distributions217 Questions

Exam 6: The Normal Distributions and Other Continuous Distributions189 Questions

Exam 7: Sampling Distributions135 Questions

Exam 8: Confidence Interval Estimation189 Questions

Exam 9: Fundamentals of Hypothesis Testing: One-Sample Tests187 Questions

Exam 10: Two-Sample Tests208 Questions

Exam 11: Analysis of Variance216 Questions

Exam 12: Chi-Square and Nonparametric Tests178 Questions

Exam 13: Simple Linear Regression214 Questions

Exam 14: Introduction to Multiple Regression336 Questions

Exam 15: Multiple Regression Model Building99 Questions

Exam 16: Time-Series Forecasting173 Questions

Exam 17: Business Analytics115 Questions

Exam 18: A Roadmap for Analyzing Data329 Questions

Exam 19: Statistical Applications in Quality Management Online162 Questions

Exam 20: Decision Making Online129 Questions

Exam 21: Understanding Statistics: Descriptive and Inferential Techniques39 Questions

Select questions type

Which of the following statements about moving averages is not true?

(Multiple Choice)

4.8/5  (44)

(44)

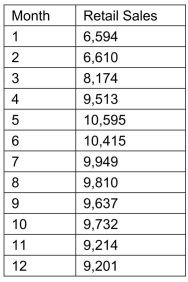

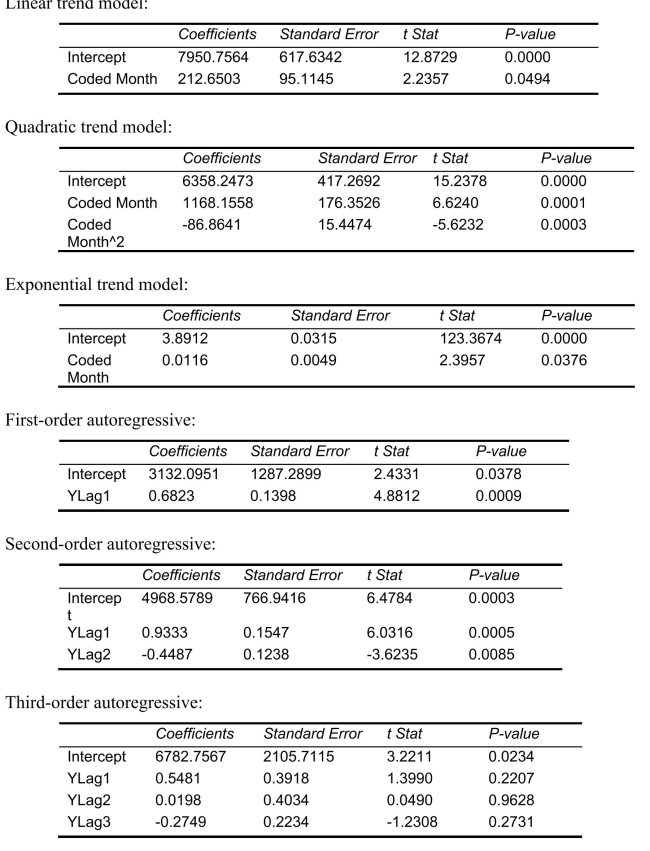

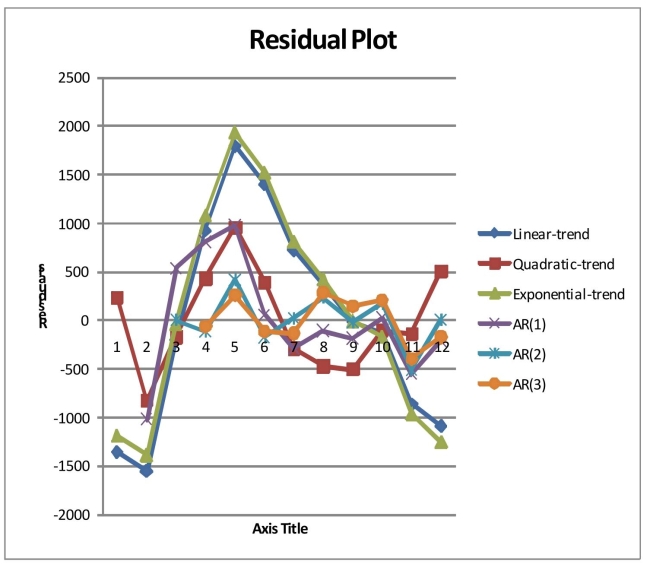

SCENARIO 16-13 Given below is the monthly time series data for U.S.retail sales of building materials over a specific year.  The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the

The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the  month is 0:

month is 0:  Below is the residual plot of the various models:

Below is the residual plot of the various models:  -Referring to Scenario 16-13, what is the value of the t test statistic for testing the appropriateness of the third-order autoregressive model?

-Referring to Scenario 16-13, what is the value of the t test statistic for testing the appropriateness of the third-order autoregressive model?

(Short Answer)

4.8/5 (32)

SCENARIO 16-12 A local store developed a multiplicative time-series model to forecast its revenues in future quarters, using quarterly data on its revenues during the 5-year period from 2009 to 2013.The following is the resulting regression equation:  where

where  is the estimated number of contracts in a quarter. X is the coded quarterly value with X = 0 in the first quarter of 2008.

is the estimated number of contracts in a quarter. X is the coded quarterly value with X = 0 in the first quarter of 2008.  is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise.  is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise.

is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise.  is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise.

-Referring to Scenario 16-12, the best interpretation of the coefficient of

is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise.

-Referring to Scenario 16-12, the best interpretation of the coefficient of  (0.098)in the regression equation is:

(0.098)in the regression equation is:

(Multiple Choice)

4.9/5 (40)

SCENARIO 16-13 Given below is the monthly time series data for U.S.retail sales of building materials over a specific year. The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the month is 0: Below is the residual plot of the various models:

-Referring to Scenario 16-13, what is the exponentially smoothed value for the first month using a smoothing coefficient of W = 0.5?

(Short Answer)

4.9/5 (37)

SCENARIO 16-13 Given below is the monthly time series data for U.S.retail sales of building materials over a specific year. The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the month is 0: Below is the residual plot of the various models:

-Referring to Scenario 16-13, if a five-month moving average is used to smooth this series, how many moving averages can you compute?

(Short Answer)

4.7/5 (36)

SCENARIO 16-12 A local store developed a multiplicative time-series model to forecast its revenues in future quarters, using quarterly data on its revenues during the 5-year period from 2009 to 2013.The following is the resulting regression equation: where is the estimated number of contracts in a quarter. X is the coded quarterly value with X = 0 in the first quarter of 2008. is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise. is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise. is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise.

-Referring to Scenario 16-12, using the regression equation, what is the forecast for the revenues in the fourth quarter of 2015?

(Short Answer)

4.8/5 (39)

Which of the following methods should not be used for short-term forecasts into the future?

(Multiple Choice)

4.8/5 (40)

SCENARIO 16-13 Given below is the monthly time series data for U.S.retail sales of building materials over a specific year. The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the month is 0: Below is the residual plot of the various models:

-Referring to Scenario 16-13, what is the p-value of the t test statistic for testing the appropriateness of the second-order autoregressive model?

(Short Answer)

4.7/5 (43)

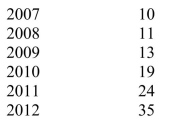

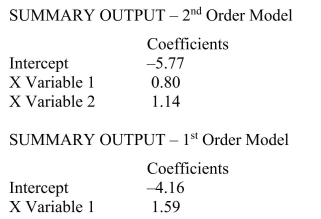

SCENARIO 16-10 Business closures in a city in the western U.S.from 2007 to 2012 were:  Microsoft Excel was used to fit both first-order and second-order autoregressive models, resulting in the following partial outputs:

Microsoft Excel was used to fit both first-order and second-order autoregressive models, resulting in the following partial outputs:  -Referring to Scenario 16-10, the fitted values for the second-order autoregressive model are ________, ________, ________, and ________.

-Referring to Scenario 16-10, the fitted values for the second-order autoregressive model are ________, ________, ________, and ________.

(Short Answer)

4.7/5 (27)

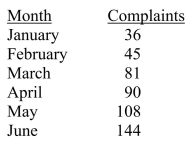

SCENARIO 16-3 The following table contains the number of complaints received in a department store for the first 6 months of last year.  -Referring to Scenario 16-3, suppose the last two smoothed values are 81 and 96 (Note: they are not).What would you forecast as the value of the time series for July?

-Referring to Scenario 16-3, suppose the last two smoothed values are 81 and 96 (Note: they are not).What would you forecast as the value of the time series for July?

(Multiple Choice)

4.9/5 (31)

The annual multiplicative time-series model does not possess _______ component.

(Multiple Choice)

4.9/5 (44)

SCENARIO 16-13 Given below is the monthly time series data for U.S.retail sales of building materials over a specific year. The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the month is 0: Below is the residual plot of the various models:

-Referring to Scenario 16-13, what is the exponentially smoothed forecast for the  month using a smoothing coefficient of W = 0.5 if the exponentially smooth value for the 1

month using a smoothing coefficient of W = 0.5 if the exponentially smooth value for the 1  and 11th month are 9,746.3672 and 9,480.1836, respectively?

and 11th month are 9,746.3672 and 9,480.1836, respectively?

(Short Answer)

4.9/5 (32)

SCENARIO 16-12 A local store developed a multiplicative time-series model to forecast its revenues in future quarters, using quarterly data on its revenues during the 5-year period from 2009 to 2013.The following is the resulting regression equation: where is the estimated number of contracts in a quarter. X is the coded quarterly value with X = 0 in the first quarter of 2008. is a dummy variable equal to 1 in the first quarter of a year and 0 otherwise. is a dummy variable equal to 1 in the second quarter of a year and 0 otherwise. is a dummy variable equal to 1 in the third quarter of a year and 0 otherwise.

-Referring to Scenario 16-12, the best interpretation of the constant 6.102 in the regression equation is:

(Multiple Choice)

4.8/5 (36)

The manager of a company believed that her company's profits were following an exponential trend.She used Microsoft Excel to obtain a prediction equation for the logarithm (base 10)of profits:  (Profits)= 2 + 0.3X The data she used were from 2007 through 2012 coded 0 to 5.The forecast for 2013 profits is __________.

(Profits)= 2 + 0.3X The data she used were from 2007 through 2012 coded 0 to 5.The forecast for 2013 profits is __________.

(Short Answer)

4.8/5 (32)

SCENARIO 16-10 Business closures in a city in the western U.S.from 2007 to 2012 were: Microsoft Excel was used to fit both first-order and second-order autoregressive models, resulting in the following partial outputs:

-Referring to Scenario 16-10, the residuals for the first-order autoregressive model are ________, ________, ________, ________, and ________.

(Short Answer)

4.7/5 (37)

To assess the adequacy of a forecasting model, one measure that is often used is

(Multiple Choice)

4.7/5 (39)

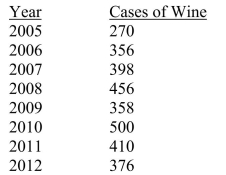

SCENARIO 16-4 The number of cases of merlot wine sold by a Paso Robles winery in an 8-year period follows.  -Referring to Scenario 16-4, a centered 3-year moving average is to be constructed for the wine sales.The result of this process will lead to a total of __________ moving averages.

-Referring to Scenario 16-4, a centered 3-year moving average is to be constructed for the wine sales.The result of this process will lead to a total of __________ moving averages.

(Short Answer)

4.9/5 (33)

SCENARIO 16-13 Given below is the monthly time series data for U.S.retail sales of building materials over a specific year. The results of the linear trend, quadratic trend, exponential trend, first-order autoregressive, second-order autoregressive and third-order autoregressive model are presented below in which the coded month for the month is 0: Below is the residual plot of the various models:

-Referring to Scenario 16-13, the best model based on the residual plots is the linear-trend model.

(True/False)

4.8/5 (38)

With a 15-year time duration and available time series data, how many five-year moving average forecasts can be made?

(Multiple Choice)

4.8/5 (36)

A second-order autoregressive model for average mortgage rate is:  If the average mortgage rate in 2012 was 7.0, and in 2011 was 6.4, the forecast for 2013 is __________.

If the average mortgage rate in 2012 was 7.0, and in 2011 was 6.4, the forecast for 2013 is __________.

(Short Answer)

4.7/5 (29)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)