Exam 5: Consolidation of Non-Wholly Owned Subsidiaries

Exam 1: Setting the Stage40 Questions

Exam 2: Intercorporate Equity Investments: an Introduction43 Questions

Exam 3: Business Combinations43 Questions

Exam 3: Appendix A: AIncome Tax Allocation6 Questions

Exam 4: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions40 Questions

Exam 4: Appendix A: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions4 Questions

Exam 4: Appendix B: Wholly Owned Subsidiaries: Reporting Subsequent Acquisitions6 Questions

Exam 5: Consolidation of Non-Wholly Owned Subsidiaries41 Questions

Exam 5: Appendix A: Step Purchases6 Questions

Exam 5: Appendix B: Decreases in Ownership Interest4 Questions

Exam 6: Subsequent-Year Consolidations: General Approach40 Questions

Exam 6: Appendix A: Preferred and Restricted Shares of Investee Corporation5 Questions

Exam 6: Appendix B: Intercompany Bond Holdings6 Questions

Exam 7: Segment and Interim Reporting41 Questions

Exam 8: Foreign Currency Transactions and Hedges49 Questions

Exam 9: Reporting Foreign Operations44 Questions

Exam 10: Financial Reporting for Not-For-Profit Organizations46 Questions

Exam 10: Appendix A: Fund Accounting5 Questions

Exam 11: Public Sector Financial Reporting44 Questions

Select questions type

Which of the following is not a reason why a parent company would prefer to be involved with an NCI?

(Multiple Choice)

4.9/5  (32)

(32)

On December 31, 20X5, Paper Co. purchased 60% of the outstanding common shares of Book Ltd. for $760,000 in shares and $200,000 in cash. The statements of financial position of Paper and Book immediately before the acquisition and issuance of the notes payable were as follows (in 000s):

Book Fair Book Fair Value Value Value Value Cash \ 360 \ 360 \ 200 \ 200 Accounts receivable 520 500 380 380 Inventory 800 880 400 360 Property, plant, and equipment 2,000 1,640 \ 3,500 \ 2,400

Accounts payable \ 380 \ 380 \ 260 \ 260 Long-term liabilities 1,200 1,200 1000 1000 Common shares 500 600 Retained earnings \ 3,500 \ 2,400

The difference in the carrying value and the fair value of the property, plant, and equipment for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 35% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 35% of selling price. At December 31, 20X6, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

Paper uses the cost method to report its investment in Book.

Required:

Paper has determined that it does not have control but only has significant influence over Book. Calculate the balance in the investment account at December 31, 20X7.

Calculate the investment income from this investee for 20X7 that Paper would show on its statement of comprehensive income.

(Essay)

4.9/5 (34)

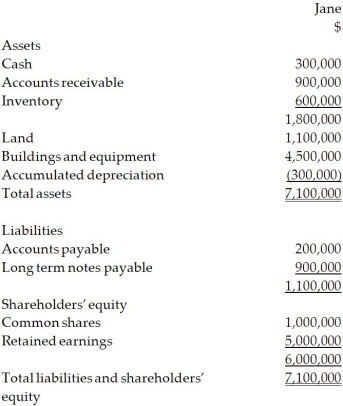

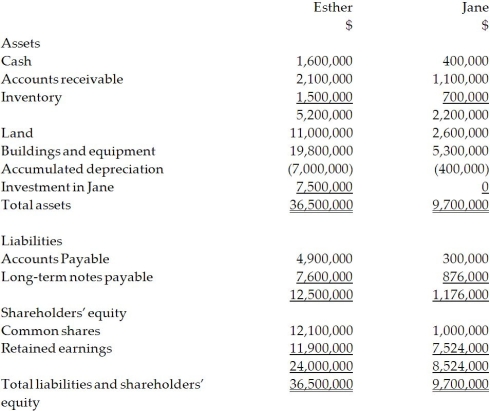

On December 31, 20X2, Esther Company purchased 80% of the outstanding common shares of Jane Company for $7.5 million in cash. On that date, the shareholders' equity of Jane totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization. The statement of financial position for Jane is provided below at December 31, 20X2.  For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: Esther Jane Sales and other revenue Cost of goods sold 8,000,000 4,000,000 Depreciation expense 1,500,000 1,000,000 Other expenses Total expenses Net income At December 31, 20X4, the condensed statement of financial position for the two companies were as follows:

For the year ending December 31, 20X4, the statements of comprehensive income for Esther and Jane were as follows: Esther Jane Sales and other revenue Cost of goods sold 8,000,000 4,000,000 Depreciation expense 1,500,000 1,000,000 Other expenses Total expenses Net income At December 31, 20X4, the condensed statement of financial position for the two companies were as follows:  OTHER INFORMATION:

1. On December 31, 20X2, Jane had a building with a fair value that was $450,000 greater than its carrying value. The building had an estimated remaining useful life of 15 years.

2. On December 31, 20X2, Jane had inventory with a fair value that was $150,000 less than its carrying value. This inventory was sold in 20X3.

3. During 20X3, Jane sold merchandise to Esther for $100,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Esther and the other 60% remained in its December 31, 20X3, inventories. On December 31, 20X4, the inventories of Esther contained merchandise purchased from Jane on which Jane had recognized a gross profit in the amount of $20,000. Total sales from Jane to Esther were $150,000 during 20X4.

4. During 20X4, Esther declared and paid dividends of $300,000, while Jane declared and paid dividends of $100,000.

5. Esther accounts for its investment in Jane using the cost method.

Required:

Calculate goodwill on the consolidated balance sheet at December 31, 20X4, under the entity method and the parent-company extension method. Explain the differences between the two balances.

OTHER INFORMATION:

1. On December 31, 20X2, Jane had a building with a fair value that was $450,000 greater than its carrying value. The building had an estimated remaining useful life of 15 years.

2. On December 31, 20X2, Jane had inventory with a fair value that was $150,000 less than its carrying value. This inventory was sold in 20X3.

3. During 20X3, Jane sold merchandise to Esther for $100,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Esther and the other 60% remained in its December 31, 20X3, inventories. On December 31, 20X4, the inventories of Esther contained merchandise purchased from Jane on which Jane had recognized a gross profit in the amount of $20,000. Total sales from Jane to Esther were $150,000 during 20X4.

4. During 20X4, Esther declared and paid dividends of $300,000, while Jane declared and paid dividends of $100,000.

5. Esther accounts for its investment in Jane using the cost method.

Required:

Calculate goodwill on the consolidated balance sheet at December 31, 20X4, under the entity method and the parent-company extension method. Explain the differences between the two balances.

(Essay)

4.8/5 (36)

On December 31, 20X5, Paper Co. purchased 60% of the outstanding common shares of Book Ltd. for $760,000 in shares and $200,000 in cash. The statements of financial position of Paper and Book immediately before the acquisition were as follows (in 000s):

Book Fair Book Fair Value Value Value Value Cash \ 360 \ 360 \ 200 \ 200 Accounts receivable 520 500 380 380 Inventory 800 880 400 360 Property, plant, and equipment 2,000 1,640 \ 3,500 \ 2,400 Accounts payable \ 380 \ 380 \ 260 \ 260 Long-term liabilities 1,200 1,200 1000 1000 Common shares 500 600 Retained earnings \ 3,500 \ 2,400

The difference in the carrying value and the fair value of the property, plant, and equipment for Book relates to its office building. This building has an estimated 20 years remaining of useful life.

During 20X6, the year following the acquisition, the following occurred:

1. Throughout the year, Book purchased merchandise of $800,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X6, Book still owed Paper $250,000 on this merchandise; 75% of this merchandise was resold by Book prior to December 31, 20X6.

2. Throughout the year, Book sold merchandise to Paper totalling $500,000. The gross margin on these products is 25%. At the end of 20X6, Paper had not yet resold 60% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X6 and Paper paid dividends of $500,000.

During 20X7, the following occurred:

1. Throughout the year, Book purchased merchandise of $1,000,000 from Paper. Paper's gross margin is 30% of selling price. At December 31, 20X7, Book still owed Paper $150,000 on this merchandise; 85% of this merchandise was resold by Book prior to December 31, 20X7.

2. Throughout the year, Book sold merchandise to Paper totalling $650,000. The gross margin in these products is 25%. At the end of 20X7, Paper had not yet resold 40% of this merchandise.

3. Management fees were paid to Paper from Book totalling $250,000.

4. Book paid dividends of $250,000 at the end of 20X7 and Paper paid dividends of $500,000.

5. Goodwill was tested and found to be impaired, resulting in $100 impairment loss.

6. Paper uses the cost method to report its investment in Book.

Required:

Calculate the following items as they would appear on the Paper Co.'s consolidated statement of financial position at December 31, 20X7, under the entity method:

a. Goodwill

b. Non-controlling interest

c. Property, plant, and equipment, net

(Essay)

4.8/5 (32)

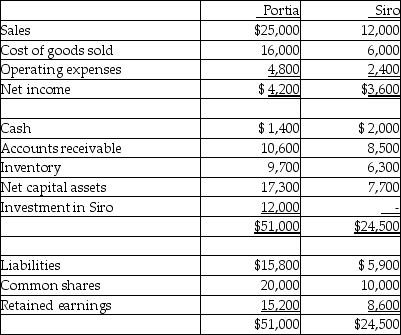

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:  - During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What amount should be shown on the consolidated statement of financial position for the non-controlling interest at December 31, 20X1?

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What amount should be shown on the consolidated statement of financial position for the non-controlling interest at December 31, 20X1?

(Multiple Choice)

4.7/5 (38)

Olthius Ltd. purchased 60% of Fredo Ltd. for $1,500,000. At the date of acquisition, the carrying value of Fredo's net identifiable assets was $1,800,000 and the fair value was $2,200,000. What is the amount of the goodwill under the entity method?

(Multiple Choice)

4.9/5 (41)

On December 31, 20X6, the balance sheets of Power Company and Pro Company are as follows (amounts in thousands):

Pawer Pra Pra (FV) Cash \ 500 \ 800 Accounts receivable 1,500 1,700 Inventorips 2,000 1,500 Plant and Equipment (net) \ 4,300 Total Assets \ 6,500 \ 8,000 Current liabilities \ 700 \ 400 Long-term liabilities 800 500 \4 00 Common shares 2,500 1,000 Contributed surplus 800 1,500 Retained earnings Total equities \ 6,500 \ 8,000

Power Company has 100,000 shares of common stock outstanding; Pro Company has 45,000 shares outstanding. All assets and liabilities have book values equal to fair values, except as noted.

The plant and equipment has an estimated remaining useful life of nine years from the date of acquisition. The long-term liabilities mature on December 31, 2020. The company estimates that straight-line amortization will approximate the effective interest rate method.

Required:

Assume that 80% of the outstanding shares of Pro were acquired for cash of $5.8 million. Calculate goodwill and the non-controlling interest on the consolidated statement of financial position at December 31, 20X6, under the entity method and the parent-company extension method.

At December 31, 20X9, the balance in the long term liabilities of Pro is still $500,000 and the balance of long term liabilities for Power is $900,000. Calculate the balance in the consolidated long-term liabilities at December 21, 20X9.

(Essay)

4.7/5 (34)

On December 31, 20X2, Bates Ltd. purchased 75% of the outstanding common shares of Ted Ltd. for $1,050,000 in cash. The balance sheets of Bates and Ted immediately before the acquisition were as follows (in 000s): Bates Ted Cash Vook Value Fair Value Book Value Fair Value Accounts receivable \ 160 \ 160 \ 100 \ 100 Inventory 420 400 280 280 Capital assets 600 680 300 350 2,000 1,620 Current liabilities \ 280 \ 280 \ 160 \ 180 Long-term liabilities 1,100 1,100 900 900 Common shares 500 500 Retained earnings At the time of acquisition, Ted's capital assets still had a remaining useful life of 10 years. Under the entity method, what amount should be allocated to goodwill?

(Multiple Choice)

5.0/5 (33)

Bates Ltd. owns 60% of the outstanding common shares of Sam Ltd. During 20X6, sales from Sam to Bates were $200,000. Merchandise was priced to provide Sam with a gross margin of 20%. Bates's inventories contained $40,000 at December 31, 20X5, and $15,000 at December 31, 20X6, of merchandise purchased from Sam. Cost of goods sold for Bates and Sam for 20X6 on their separate-entity income statements were as follows: Bates Sam Beginning inventory \ 100,000 \ 50,000 Purchases 700,000 200,000 Ending inventory Cost of goods sold \ \ What is the balance of the inventory account on Bates's consolidated statement of financial position at December 31, 20X6?

(Multiple Choice)

4.9/5 (42)

Portia Ltd. acquired 80% of Siro Ltd. on December 31, 20X0. At the acquisition date, Siro's net assets totalled $15,000. Portia uses the cost method to record the acquisition and consolidates using the entity method. At December 31, 20X1, the separate-entity financial statements showed the following:

- During 20X1, Siro sold $7,000 of goods, with a gross margin of 40%, to Portia. At the end of 20X1, $3,000 of the goods were still in Portia's inventory. What portion of consolidated net income for 20X1 is attributable to Portia?

(Multiple Choice)

4.9/5 (33)

On December 31, 20X6, the statements of financial position of Power Company and Pro Company are as follows (amounts in thousands):

Power Pra Pro (FV) Cash \ 500 \ 800 Accounts receivable 1,500 1,700 Inventories 2,000 1,500 Plant and equipment (net) \ 4,300 Total Assets \6 ,500 \8 ,000 Current liabilities \ 700 \ 400 Long-term liabilities 800 500 \ 400 Common shares 2,500 1,000 Contributed suplus 800 1,500 Retained earnings Total Equities \ \ \ ,500 \ \ ,000 Power Company has 100,000 shares of common stock outstanding. Pro Company has 45,000 shares outstanding. All assets and liabilities have book values equal to fair values, except as noted above.

The plant and equipment has an estimated remaining useful life of nine years from the date of acquisition. The long-term liabilities mature on December 31, 2020. Market value of the new shares issued was $90 per share at issuance.

Required:

Assume that 90% of the outstanding shares of Pro were acquired for cash of $8.1 million. Calculate goodwill and the non-controlling interest on the consolidated balance sheet at December 31, 20X6, under the entity method and the parent-company extension method. Explain the differences between the two balances for goodwill.

Which method is preferred under IFRS? Why are the two methods allowed? Which methods are allowed under ASPE?

(Essay)

4.9/5 (38)

A parent company chooses to acquire only a 65% interest in its subsidiary. Which of the following is not a reason why the parent would choose to acquire less than a 100% interest in a subsidiary?

(Multiple Choice)

4.8/5 (42)

Taguchi Ltd. owns 80% of Shag Co. Shag declared and paid $100,000 in dividends. Taguchi uses the cost method to record its investment in Shag. In preparing Taguchi's consolidated financial statements, what elimination entry must be made with respect to the dividends?

(Multiple Choice)

4.7/5 (46)

Under IAS 27, where does the non-controlling interest (NCI)appear on the statement of financial position?

(Multiple Choice)

4.8/5 (36)

Arnez Ltd. acquired 70% of Bedard Ltd. At the acquisition date, Bedard's net identifiable assets had a carrying value of $825,000 and a fair value of $1,000,000. Arnez paid $910,000 for the acquisition. Under the parent-company extension method, what amount should be reported for goodwill on Arnez's consolidated statement of financial position?

(Multiple Choice)

4.9/5 (37)

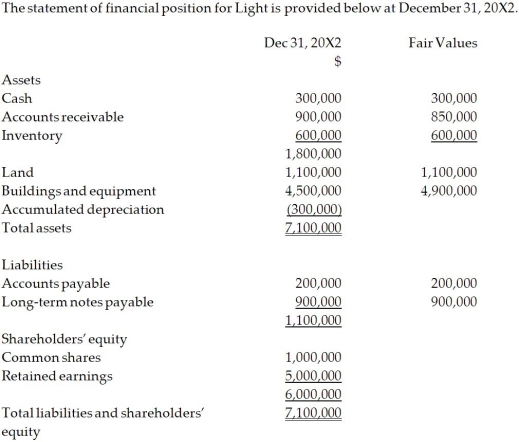

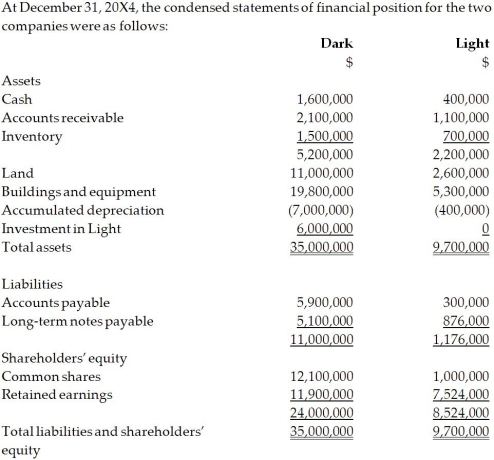

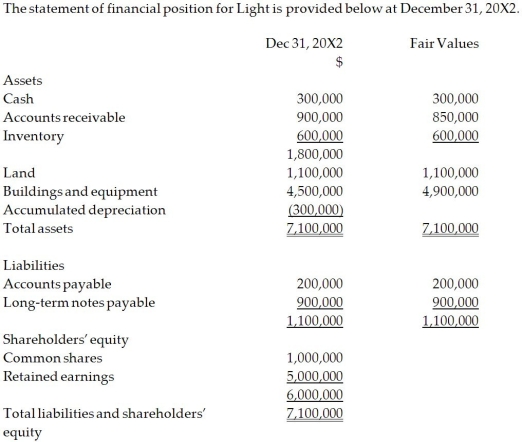

On December 31, 20X2, Dark Company purchased 75% of the outstanding common shares of Light Company for $6.0 million in cash. On that date, the shareholders' equity of Light totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization.  For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

Dark Light Sales and other revenue \ 12,500,000 \ 6,804,000 Cost of goods sold 8,000,000 4,000,000 Depreciation expense 1,500,000 1,000,000 Other expenses 1,800,000 1,200,000 Total expenses 6,200,000 Net income

For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

Dark Light Sales and other revenue \ 12,500,000 \ 6,804,000 Cost of goods sold 8,000,000 4,000,000 Depreciation expense 1,500,000 1,000,000 Other expenses 1,800,000 1,200,000 Total expenses 6,200,000 Net income  OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000 while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the non-controlling interest on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Calculate the NCI's share of earnings for 20X4.

OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000 while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the non-controlling interest on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Calculate the NCI's share of earnings for 20X4.

(Essay)

4.8/5 (38)

Amber Ltd. purchased 80% of Patel Ltd. for $1,000,000. At the time of acquisition, the carrying value of Patel's net identifiable assets was $1,000,000 and the fair value was $1,350,000. What is the amount of the goodwill under the entity method?

(Multiple Choice)

4.8/5 (38)

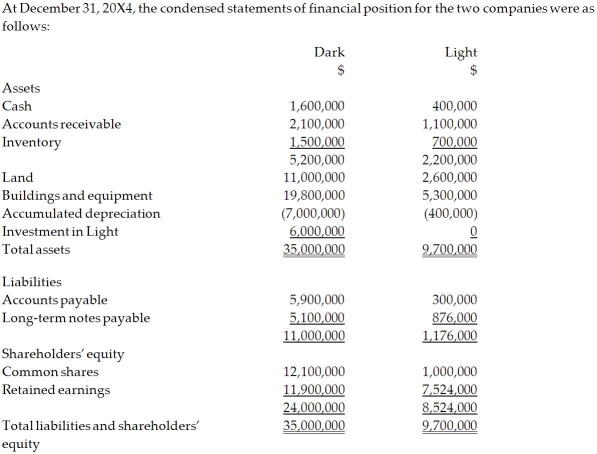

On December 31, 20X2, Dark Company purchased 75% of the outstanding common shares of Light Company for $6.0 million in cash. On that date, the shareholders' equity of Light totalled $6 million and consisted of $1 million in no par common shares and $5 million in retained earnings. Both companies use the straight-line method to calculate depreciation and amortization.  For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

Dark Light Sales and other revenue \ 12,500,000 \ 6,804,000 Cost of goods sold 8,000,000 4,000,000 Depreciation expense 1,500,000 1,000,000 Other expenses 1,800,000 1,200,000 Total expenses 6,200,000 Net income

For the year ending December , the statements of comprehensive income for Dark and Light were as follows:

Dark Light Sales and other revenue \ 12,500,000 \ 6,804,000 Cost of goods sold 8,000,000 4,000,000 Depreciation expense 1,500,000 1,000,000 Other expenses 1,800,000 1,200,000 Total expenses 6,200,000 Net income  OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000, while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the retained earnings balance on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Prepare the consolidated statement of financial position at December 31, 20X4.

OTHER INFORMATION:

1. On December 31, 20X2, Light had a building with a fair value that was $4,900,000 and an estimated remaining useful life of 20 years.

2. On December 31, 20X2, Light had a trademark that had a fair value of $60,000. The trademark has an expected useful life of five years.

3. During 20X3, Light sold merchandise to Dark for $150,000, a price that included a gross profit of $50,000. During 20X3, 40% of this merchandise was resold by Dark and the other 60% remained in its December 31, 20X3, inventories.

4. On December 31, 20X4, the inventories of Dark contained merchandise purchased from Light on which Light had recognized a gross profit in the amount of $20,000. Total sales from Light to Dark were $150,000 during 20X4.

5. During 20X4, Dark declared and paid dividends of $300,000, while Light declared and paid dividends of $100,000.

6. Dark accounts for its investment in Light using the cost method.

Required:

Calculate the retained earnings balance on the consolidated statement of financial position at December 31, 20X4, under the entity method.

Prepare the consolidated statement of financial position at December 31, 20X4.

(Essay)

4.8/5 (40)

Under ASPE reporting requirements for investments in subsidiaries, how should the NCI at the time of acquisition be valued?

(Multiple Choice)

4.8/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)