Exam 13: Additional Topics in Regression Analysis

Exam 1: Describing Data: Graphical247 Questions

Exam 2: Describing Data: Numerical326 Questions

Exam 3: Probability345 Questions

Exam 4: Discrete Random Variables and Probability Distributions257 Questions

Exam 5: Continuous Random Variables and Probability Distributions239 Questions

Exam 6: Sampling and Sampling Distributions147 Questions

Exam 7: Estimation: Single Population151 Questions

Exam 8: Estimation: Additional Topics109 Questions

Exam 9: Hypothesis Testing: Single Population164 Questions

Exam 10: Hypothesis Testing: Additional Topics103 Questions

Exam 11: Simple Regression217 Questions

Exam 12: Multiple Regression252 Questions

Exam 13: Additional Topics in Regression Analysis168 Questions

Exam 14: Analysis of Categorical Data241 Questions

Exam 15: Analysis of Variance192 Questions

Exam 16: Time-Series Analysis and Forecasting138 Questions

Exam 17: Additional Topics in Sampling110 Questions

Select questions type

If εt is the error in time t,εt-1 is the error in the previous time period,ρ is the correlation coefficient,and μt a random variable with autocorrelation,which of the following is the first-order autoregressive model of autocorrelated behavior?

(Multiple Choice)

4.7/5  (43)

(43)

If dummy variables are used to represent distinct subsets or regions,then a linear relationship between predictor variables will result,and estimation of coefficients will be impossible.

(True/False)

4.7/5 (31)

A regression model with three independent variables was constructed to analyze certain data: y = β0 + β1X1 + β3X3 + β2X2 + ε.But while estimating the coefficient,the following regression model was mistakenly used: y = α0 + α1x1 + μ.From the second formula,which of the following can be deduced to be affecting the regression model?

(Multiple Choice)

4.8/5 (31)

THE NEXT QUESTIONS ARE BASED ON THE FOLLOWING INFORMATION:

You are interested in examining the factors that determine the average length of stay in a hospital across states.You collect data on the following variables:

Y = statewide average hospital stay

X1 = median state income

X2 = 1 if the state is in the Northeast,0 otherwise

X3 = 1 if the state is in the South,0 otherwise

X4 = 1 if the state is in the Midwest,0 otherwise

X5 = 1 if the state is in the West,0 otherwise

-You run the following regression: Y = β0 + β1X1 + β2X2 + β3X3 + β4X4.What effect does being a state in the West have on the average length of hospital stay?

(Multiple Choice)

4.8/5 (30)

When does multicollinearity occur in a multiple regression model?

(Multiple Choice)

4.9/5 (41)

If the Durbin-Watson statistic d has values greater than 4 - dL,this indicates:

(Multiple Choice)

4.9/5 (34)

Dummy variables cannot be used to estimate the seasonal effects on a regression model applied to time-series data.

(True/False)

4.7/5 (32)

THE NEXT QUESTIONS ARE BASED ON THE FOLLOWING INFORMATION:

Suppose that a regression was run with two independent variables and 25 observations.The Durbin-Watson statistic was 2.28.

-Consider a regression model that uses 50 observations.Let ei denote the residuals from the fitted regression and  i the in-sample predicted values of the dependent variables.The least squares regression of

i the in-sample predicted values of the dependent variables.The least squares regression of  on

on  i has coefficient of determination 0.028.What can you conclude from this finding?

i has coefficient of determination 0.028.What can you conclude from this finding?

(Essay)

4.7/5 (41)

You are interested in examining the factors that influence the amount of stock a person owns.As explanatory variables,you include both the person's income and also the amount of equity they have in their house.Which of the following problems would most likely affect your model?

(Multiple Choice)

4.9/5 (39)

If an analyst is regressing individual independent variables on all other independent variables of a regression model,he or she is testing for:

(Multiple Choice)

4.7/5 (42)

THE NEXT QUESTIONS ARE BASED ON THE FOLLOWING INFORMATION:

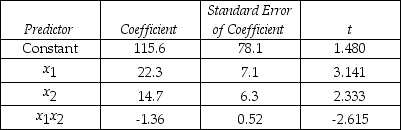

An economist is in the process of developing a model to predict the price of gold.She believes that the two most important variables are the price of a barrel of oil (x1)and the interest rate (x2).She proposes the model y = β0 + β1x1 + β2x2 + β3x1x3 + ε.A random sample of 20 daily observations was taken.The computer output is shown below.

THE REGRESSION EQUATION IS

y = 115.6 + 22.3x1 + 14.7x2 - 1.36x1x2

S = 20.9 R-Sq = 55.4%

ANALYSIS OF VARIANCE

S = 20.9 R-Sq = 55.4%

ANALYSIS OF VARIANCE

-Suppose that a regression relationship is given by Y = β0 + β1X1 + β2X2 + ε.If the simple linear regression of Y on X1 is estimated from a sample of n observations,the resulting slope estimate will generally be biased for β1.But if the sample correlation between X1 and X2 is 0,the slope will not be biased for β1.

How does X2 affect β1 if the sample correlation between X1 and X2 is zero?

-Suppose that a regression relationship is given by Y = β0 + β1X1 + β2X2 + ε.If the simple linear regression of Y on X1 is estimated from a sample of n observations,the resulting slope estimate will generally be biased for β1.But if the sample correlation between X1 and X2 is 0,the slope will not be biased for β1.

How does X2 affect β1 if the sample correlation between X1 and X2 is zero?

(Essay)

4.8/5 (29)

Consider the first-order model  = 50 - 10x1 + 8x2 - 2x1x2.A 1-unit increase in x1,while holding x2 constant at a value of 4,decreases the value of y,on average,by:

= 50 - 10x1 + 8x2 - 2x1x2.A 1-unit increase in x1,while holding x2 constant at a value of 4,decreases the value of y,on average,by:

(Multiple Choice)

4.7/5 (33)

Suppose you are interested in modeling the amount of money a household spends for a house.We would expect income to be a determining factor.In addition,the income tax rate for a household might be important since there are tax advantages to home ownership.If you were to run a regression of home purchase price on income and marginal tax rate,your results might be subject to:

(Multiple Choice)

4.8/5 (35)

Explain what is meant by multicollinearity.What effects does multicollinearity have on the results of regression coefficients?

(Essay)

4.7/5 (30)

THE NEXT QUESTIONS ARE BASED ON THE FOLLOWING INFORMATION:

Consider the following model: Y = β0 + β1X1t + β2X2t + γ3Yt-1.Using a sample of 36 months,we estimate this model and obtain the following results: yt = 1.33 + 17.6x1t + 0.94x2t + 0.39Yt-1

-If X1 were to increase by 1-unit in time t,by how much would we expect Y to change in period t?

(Multiple Choice)

4.8/5 (35)

When is a dummy variable used as an independent variable in a regression model?

(Multiple Choice)

4.7/5 (40)

Suppose we estimate the regression Yt = β0 + β1X1t + β2X2t + β3X3t + β4X4t + εt using 36 months of data.Using the residuals from this regression,we run another regression of  on the predicted values

on the predicted values  t.From this regression we get a coefficient of determination R2 of 0.09.Let H0 be that there is no heteroscedasticity.What can you conclude?

t.From this regression we get a coefficient of determination R2 of 0.09.Let H0 be that there is no heteroscedasticity.What can you conclude?

(Multiple Choice)

4.9/5 (38)

Why is it so important to understand and test the assumptions of the multiple regression model?

(Essay)

4.8/5 (32)

If the independent variables in a regression model are perfectly correlated,it will be impossible to estimate the regression coefficients.

(True/False)

4.8/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)