Exam 17: Time Series Forecasting and Index Numbers

Exam 1: An Introduction to Business Statistics and Analytics98 Questions

Exam 2: Descriptive Statistics and Analytics: Tabular and Graphical Methods120 Questions

Exam 3: Descriptive Statistics and Analytics: Numerical Methods145 Questions

Exam 4: Probability and Probability Models150 Questions

Exam 5: Predictive Analytics I: Trees, K-Nearest Neighbors, Naive Bayes,101 Questions

Exam 6: Discrete Random Variables150 Questions

Exam 7: Continuous Random Variables150 Questions

Exam 8: Sampling Distributions111 Questions

Exam 9: Confidence Intervals149 Questions

Exam 10: Hypothesis Testing150 Questions

Exam 11: Statistical Inferences Based on Two Samples140 Questions

Exam 12: Experimental Design and Analysis of Variance132 Questions

Exam 13: Chi-Square Tests120 Questions

Exam 14: Simple Linear Regression Analysis147 Questions

Exam 15: Multiple Regression and Model Building85 Questions

Exam 16: Predictive Analytics Ii: Logistic Regression, Discriminate Analysis,101 Questions

Exam 17: Time Series Forecasting and Index Numbers161 Questions

Exam 18: Nonparametric Methods103 Questions

Exam 19: Decision Theory90 Questions

Select questions type

Forecasters using a multiplicative decomposition model or time series regression model, assume that the time series components are changing over time.

(True/False)

4.9/5  (39)

(39)

The following data on prices and quantities for the years 1995 and 2000 are given for three products.

Calculate the 2000 Paasche index.

Calculate the 2000 Paasche index.

(Short Answer)

5.0/5 (33)

Consider a time series with 15 quarterly sales observations. Using the quadratic trend model, the following partial computer output was obtained.

Test the significance of the t2 term at α =.05. State the critical T value (rejection point) and the p-value. Make your decision using a two-sided null hypothesis.

Test the significance of the t2 term at α =.05. State the critical T value (rejection point) and the p-value. Make your decision using a two-sided null hypothesis.

(Short Answer)

4.8/5 (39)

Those fluctuations that are associated with climate, holidays, and related activities are referred to as ________ variations.

(Multiple Choice)

4.8/5 (29)

When deseasonalizing a time series observation, we divide the actual time series observation by its ________.

(Multiple Choice)

4.7/5 (32)

Exponential smoothing is designed to forecast time series described by regular and seasonal components that are always changing over time.

(True/False)

4.8/5 (33)

When preparing a price index based on multiple products, if the price of each product is weighted by the quantity of the product purchased in a given period of time, the resulting index is called a ________ price index.

(Multiple Choice)

4.8/5 (41)

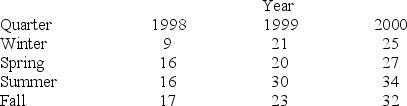

Consider the quarterly production data (in thousands of units) for the XYZ manufacturing company below. The normalized (adjusted) seasonal factors are winter = .9982, spring = .9263, summer = 1.139, and fall = .9365.

Based on the following deseasonalized observations (dt), a trend line was estimated.

1998

Based on the following deseasonalized observations (dt), a trend line was estimated.

1998

1999

1999

2000

2000

The following Minitab output gives the straight-line trend equation fitted to the deseasonalized observations. Based on the trend equation given below, calculate the trend value for each period in the time series.

The regression equation is Deseasonalized = 10.1 + 1.91 × Time

The following Minitab output gives the straight-line trend equation fitted to the deseasonalized observations. Based on the trend equation given below, calculate the trend value for each period in the time series.

The regression equation is Deseasonalized = 10.1 + 1.91 × Time

(Short Answer)

4.9/5 (33)

Simple exponential smoothing is a forecasting method that applies equal weights to the time series observations.

(True/False)

4.8/5 (36)

A forecasting method that weights recent observations more heavily is called ________.

(Multiple Choice)

5.0/5 (40)

When there is ________ seasonal variation, the magnitude of the seasonal swing does not depend on the level of the time series.

(Multiple Choice)

4.8/5 (28)

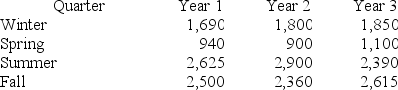

Consider the following set of quarterly sales data, given in thousands of dollars.

The following dummy variable model that incorporates a linear trend and constant seasonal variation was used: y(t) = β0 + β1t + βQ1(Q1) + βQ2(Q2) + βQ3(Q3) + Et. In this model, there are three binary seasonal variables (Q1, Q2, and Q3), where Qi is a binary (0,1) variable defined as:

Qi = 1, if the time series data is associated with quarter i;

Qi = 0, if the time series data is not associated with quarter i.

The results associated with this data and model are given in the following Minitab computer output.

The regression equation is

Sales = 2442 + 6.2 Time − 693 Q1 − 1499 Q2 + 153 Q3

The following dummy variable model that incorporates a linear trend and constant seasonal variation was used: y(t) = β0 + β1t + βQ1(Q1) + βQ2(Q2) + βQ3(Q3) + Et. In this model, there are three binary seasonal variables (Q1, Q2, and Q3), where Qi is a binary (0,1) variable defined as:

Qi = 1, if the time series data is associated with quarter i;

Qi = 0, if the time series data is not associated with quarter i.

The results associated with this data and model are given in the following Minitab computer output.

The regression equation is

Sales = 2442 + 6.2 Time − 693 Q1 − 1499 Q2 + 153 Q3

Analysis of Variance

Analysis of Variance

Provide a managerial interpretation of the regression coefficient for the variable "time."

Provide a managerial interpretation of the regression coefficient for the variable "time."

(Short Answer)

5.0/5 (33)

The Box-Jenkins methodology can be used to identify what is called an autoregressive-moving average model.

(True/False)

4.8/5 (28)

XYZ Company, Annual Data  Based on the information given in the table above, we can conclude that, in general,

Based on the information given in the table above, we can conclude that, in general,

(Multiple Choice)

4.9/5 (41)

A positive autocorrelation implies that negative error terms will be followed by ________ error terms.

(Multiple Choice)

4.8/5 (31)

The multiplicative Winters method is used to forecast time series when there are no seasonal factors that are part of the model.

(True/False)

4.9/5 (36)

The following data on prices and quantities for the years 1995 and 2000 are given for three products.

Calculate the 2000 Laspeyres index.

Calculate the 2000 Laspeyres index.

(Short Answer)

4.9/5 (29)

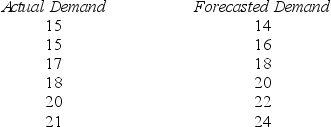

Given the following data, compute the total error (sum of the error terms).

(Short Answer)

4.7/5 (36)

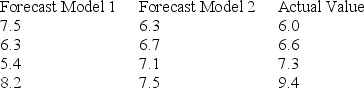

Two forecasting models were used to predict the future values of a time series. The forecasts are shown below with the actual values.

Calculate the mean absolute deviation (MAD) for Model 1.

Calculate the mean absolute deviation (MAD) for Model 1.

(Short Answer)

4.8/5 (47)

Dummy variables are used to model increasing seasonal variation.

(True/False)

4.8/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)