Exam 14: Introduction to Time Series Regression and Forecasting

Exam 1: Economic Questions and Data17 Questions

Exam 2: Review of Probability71 Questions

Exam 3: Review of Statistics63 Questions

Exam 4: Linear Regression With One Regressor65 Questions

Exam 5: Regression With a Single Regressor: Hypothesis Tests and Confidence Intervals59 Questions

Exam 6: Linear Regression With Multiple Regressors65 Questions

Exam 7: Hypothesis Tests and Confidence Intervals in Multiple Regression65 Questions

Exam 8: Nonlinear Regression Functions62 Questions

Exam 9: Assessing Studies Based on Multiple Regression65 Questions

Exam 10: Regression With Panel Data50 Questions

Exam 11: Regression With a Binary Dependent Variable50 Questions

Exam 12: Instrumental Variables Regression50 Questions

Exam 13: Experiments and Quasi-Experiments50 Questions

Exam 14: Introduction to Time Series Regression and Forecasting50 Questions

Exam 15: Estimation of Dynamic Causal Effects50 Questions

Exam 16: Additional Topics in Time Series Regression50 Questions

Exam 17: The Theory of Linear Regression With One Regressor49 Questions

Exam 18: The Theory of Multiple Regression50 Questions

Select questions type

In order to make reliable forecasts with time series data,all of the following conditions are needed with the exception of

(Multiple Choice)

4.8/5  (41)

(41)

(Requires Appendix material): Show that the AR(1)process Yt = a1Yt-1 + et;  < 1,can be converted to a MA(∞)process.

< 1,can be converted to a MA(∞)process.

(Essay)

4.8/5 (33)

(Requires Internet access for the test question)

The following question requires you to download data from the internet and to load it into a statistical package such as STATA or EViews.

a.Your textbook suggests using two test statistics to test for stationarity: DF and ADF.Test the null hypothesis that inflation has a stochastic trend against the alternative that it is stationary by performing the DF and ADF test for a unit autoregressive root.That is,use the equation (14.34)in your textbook with four lags and without a lag of the change in the inflation rate as a regressor for sample period 1962:I - 2004:IV.Go to the Stock and Watson companion website for the textbook and download the data "Macroeconomic Data Used in Chapters 14 and 16." Enter the data for consumer price index,calculate the inflation rate and the acceleration of the inflation rate,and replicate the result on page 526 of your textbook.Make sure not to use the heteroskedasticity-robust standard error option for the estimation.

b.Next find a website with more recent data,such as the Federal Reserve Economic Data (FRED)site at the Federal Reserve Bank of St.Louis.Locate the data for the CPI,which will be monthly,and convert the data in quarterly averages.Then,using a sample from 1962:I - 2009:IV,re-estimate the above specification and comment on the changes that have occurred.

c.For the new sample period,find the DF statistic.

d.Finally,calculate the ADF statistic,allowing for the lag length of the inflation acceleration term to be determined by either the AIC or the BIC.

(Essay)

4.9/5 (41)

You should use the QLR test for breaks in the regression coefficients,when

(Multiple Choice)

4.9/5 (31)

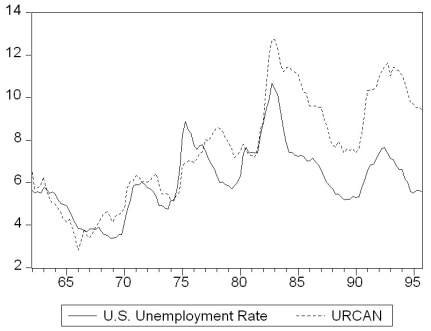

There is some evidence that the Phillips curve has been unstable during the 1962 to 1999 period for the United States,and in particular during the 1990s.You set out to investigate whether or not this instability also occurred in other places.Canada is a particularly interesting case,due to its proximity to the United States and the fact that many features of its economy are similar to that of the U.S.

(a)Reading up on some of the comparative economic performance literature,you find that Canadian unemployment rates were roughly the same as U.S.unemployment rates from the 1920s to the early 1980s.The accompanying figure shows that a gap opened between the unemployment rates of the two countries in 1982,which has persisted to this date.  Inspection of the graph and data suggest that the break occurred during the second quarter of 1982.To investigate whether the Canadian Phillips curve shows a break at that point,you estimate an ADL(4,4)model for the sample period 1962:I-1999:IV and perform a Chow test.Specifically you postulate that the constant and coefficients of the unemployment rates changed at that point.The F-statistic is 1.96.Find the critical value from the F-table and test the null hypothesis that a break occurred at that time.Is there any reason why you should be skeptical about the result regarding the break and using the Chow-test to detect it?

(b)You consider alternative ways to test for a break in the relationship.The accompanying figure shows the F-statistics testing for a break in the ADL(4,4)equation at different dates.

Inspection of the graph and data suggest that the break occurred during the second quarter of 1982.To investigate whether the Canadian Phillips curve shows a break at that point,you estimate an ADL(4,4)model for the sample period 1962:I-1999:IV and perform a Chow test.Specifically you postulate that the constant and coefficients of the unemployment rates changed at that point.The F-statistic is 1.96.Find the critical value from the F-table and test the null hypothesis that a break occurred at that time.Is there any reason why you should be skeptical about the result regarding the break and using the Chow-test to detect it?

(b)You consider alternative ways to test for a break in the relationship.The accompanying figure shows the F-statistics testing for a break in the ADL(4,4)equation at different dates.  The QLR-statistic with 15% trimming is 3.11.Comment on the figure and test for the hypothesis of a break in the ADL(4,4)regression.

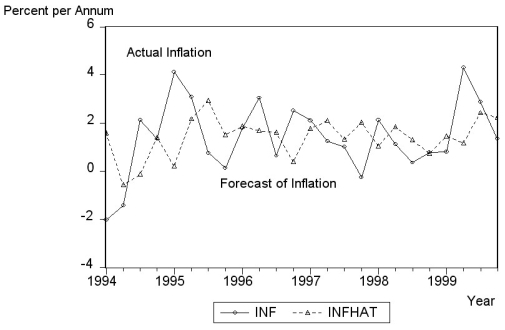

(c)To test for the stability of the Canadian Phillips curve in the 1990s,you decide to perform a pseudo out-of-sample forecasting.For the 24 quarters from 1994:I-1999:IV you use the ADL(4,4)model to calculate the forecasted change in the inflation rate,the resulting forecasted inflation rate,and the forecast error.The standard error of the ADL(4,4)for the estimation sample period 1962:1-1993:4 is 1.91 and the sample RMSFE is 1.70.The average forecast error for the 24 inflation rates is 0.003 and the sample standard deviation of the forecast errors is 0.82.Calculate the t-statistic and test the hypothesis that the mean out-of-sample forecast error is zero.Comment on the result and the accompanying figure of the actual and forecasted inflation rate.

The QLR-statistic with 15% trimming is 3.11.Comment on the figure and test for the hypothesis of a break in the ADL(4,4)regression.

(c)To test for the stability of the Canadian Phillips curve in the 1990s,you decide to perform a pseudo out-of-sample forecasting.For the 24 quarters from 1994:I-1999:IV you use the ADL(4,4)model to calculate the forecasted change in the inflation rate,the resulting forecasted inflation rate,and the forecast error.The standard error of the ADL(4,4)for the estimation sample period 1962:1-1993:4 is 1.91 and the sample RMSFE is 1.70.The average forecast error for the 24 inflation rates is 0.003 and the sample standard deviation of the forecast errors is 0.82.Calculate the t-statistic and test the hypothesis that the mean out-of-sample forecast error is zero.Comment on the result and the accompanying figure of the actual and forecasted inflation rate.

(Essay)

4.8/5 (43)

(Requires Appendix material)The long-run,stationary state solution of an AD(p,q)model,which can be written as A(L)Yt = β0 + c(L)Xt-1 + ut,where  = 1,and

= 1,and  = -βj,cj = δj,can be found by setting L=1 in the two lag polynomials.Explain.Derive the long-run solution for the estimated ADL(4,4)of the change in the inflation rate on unemployment:

= -βj,cj = δj,can be found by setting L=1 in the two lag polynomials.Explain.Derive the long-run solution for the estimated ADL(4,4)of the change in the inflation rate on unemployment:  t = 1.32 - .36 ΔInft-1 - 0.34vInft-2 + 0.7ΔInft-3 - 0.3ΔInft-4

-2.68Unempt-1 + 3.43Unempt-2 - 1.04Unempt-3 + .07Unempt-4

Assume that the inflation rate is constant in the long-run and calculate the resulting unemployment rate.What does the solution represent? Is it reasonable to assume that this long-run solution is constant over the estimation period 1962-1999? If not,how could you detect the instability?

t = 1.32 - .36 ΔInft-1 - 0.34vInft-2 + 0.7ΔInft-3 - 0.3ΔInft-4

-2.68Unempt-1 + 3.43Unempt-2 - 1.04Unempt-3 + .07Unempt-4

Assume that the inflation rate is constant in the long-run and calculate the resulting unemployment rate.What does the solution represent? Is it reasonable to assume that this long-run solution is constant over the estimation period 1962-1999? If not,how could you detect the instability?

(Essay)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)